Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

OPEC Eases Production Cuts Amid Signs of Growing Oil Demand

OPEC has bowed to the inevitable. Last week the oil producers group decided to ease self-imposed production cuts it implemented last year due to the Coronavirus pandemic. Faced with rapid demand growth the cartel - together with Russia and other countries - will add over 2 million barrels per day (mln bpd) to supplies by July.

But the move feels nervous and somewhat reluctant. OPEC remains uncertain of just how robust and resilient the recovery in oil demand will be. Worried that opening the taps too soon may undermine oil prices and trigger unnecessary discord amongst its members. It remains a jumpy and occasionally fractious group.

After the meeting Saudi Energy Minister Prince Abdulaziz Bin Salman said the move was “a very conservative measure”. He was careful to add that the group - known as “OPEC plus” - will have the chance to trim the increases - when it next meets on April 28th - if demand growth is less than expected. Last month he warned “at the risk of sounding like a stuck record, I would once again urge caution and vigilance”.

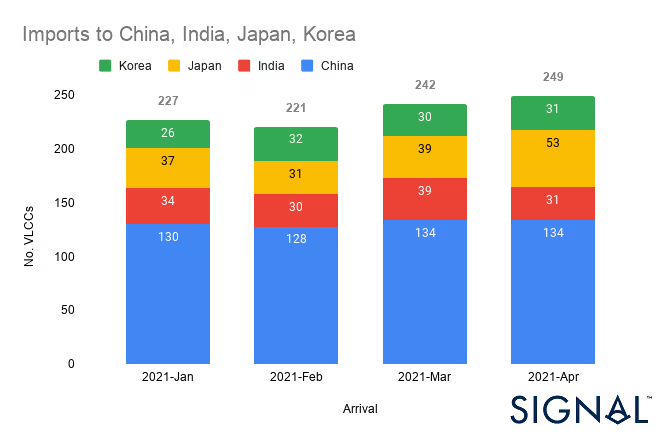

The anxiety feels a little unnecessary but perhaps understandable. OPEC can take some hope from four of the world’s biggest oil importers who are already showing unambiguous signs of growing demand. Together - China, India, Japan and Korea - are expecting 249 Very Large Crude Carriers (VLCC’s) to arrive this month, according to the Signal Oceanplatform. This compares to 242 in March, 221 in February and 227 in January.

The VLCC figures for this month are provisional and likely to change due to ships changing course, speed and destinations. But there is supporting evidence from OPEC’s own research department of demand growth. OPEC itself expects world oil demand to rise by 2.57 mln bpd in the second quarter compared to the first. March MOMR. And to see further rises of 1.82 mln bpd and 1.48 mln bpd in the third and fourth quarters respectively.

These wider projections of demand growth as the world economy recovers from the pandemic should be reassuring to OPEC. As should historical precedence, which shows oil demand recovering quickly after global economic trauma and regional recessions. Governments around the world are eager to stimulate economic recovery but need cheap and plentiful energy to do it.

Keen to keep oil taps flowing both the United States and India applied diplomatic pressure to Saudi Arabia ahead of the OPEC-plus meeting last week. They too are wary and anxious. Fragile economic growth could be thrown off course if OPEC underestimates oil demand and keeps production cuts in place for too long.

Forecasting oil demand is becoming more difficult for the sometimes fractious cartel. Not least because of the broadly chaotic and latent shift towards a less carbon intensive global economy. Still, forecasts by the group’s research department point to a strong recovery in oil demand this year based on economic expectations. Yet on-the-ground individual OPEC countries may see a more disguised picture.

According to data from the Signal Ocean platform Chinese demand growth this year has been partly met by oil from the Atlantic Basin which can be a blind spot for the mostly Arabian Gulf (AG) focused oil producing cartel. Having not experienced the full impact of that demand growth they may feel understandably less confident. For OPEC there was an unnerving drop in oil supplied to China from the AG in February (61 VLCCs) compared to January (84 VLCCs). Over the same period there was a commensurate rise from the Atlantic Basin.

The global oil market is a self-organising and self-describing network with a flexible architecture. Oil tankers (and pipeline networks) continuously optimise the network of buyers and sellers based on price mismatches. A key challenge for OPEC is that this network is beginning to change shape more rapidly. And it will continue to do so as the world shifts towards less carbon intensive energy sources.

For the moment it remains focused on fastidiously navigating a short-term policy as the world emerges from the worst impacts of the Coronavirus pandemic. But this feels like an unsustainable approach in the longer term. Perhaps this is the moment for OPEC to begin considering wider change? Maybe to broaden, modernise and to reflect and recognise the challenges of the coming energy transition.\

Meanwhile, the cartel’s attention will focus on the short term again when it meets on 28th of this month to review last week’s decisions. The empirical evidence of tanker data will provide further clues about the robustness of Chinese demand. And where supplies are coming from. The Atlantic Basin will probably remain the biggest challenger to MidEast producers.

Last week Baker Hughes reported the biggest weekly gain in oil rigs in the United States since January 2020. This is a lead indicator and crude oil production remains roughly 2 mln bpd below peaks of last year. But production has been nudging higher over the past couple of weeks, according to the US Energy Information Administration. Having previously faced down the US fracking industry the cartel is uniquely sensitive to signs of resurgent drilling activity.

Despite this, and the prospect of additional Norwegian oil later in the year, OPEC can relax. The world remains hooked on oil. For the moment at least. And there is a global determination to revive economic growth, manufacturing and trade. The cartel itself expects Chinese oil demand to grow by 8.49% this year and India by 13.60%. March MOMR. Sometimes it is difficult to believe your own view.

Sam Arnold-Forster is an independent analyst. The views expressed are his own and do not necessarily represent those of the Signal Group.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)