Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Special Focus of the Week

Rising U.S. pressure on Russian oil buyers is prompting China and India to reduce imports and diversify supply.

The U.S. has publicly floated the possibility of implementing secondary tariffs on nations like China and India that continue buying Russian crude, but no such measures have been formally enacted. In Q2 2025, crude shipments from Russia to China were down about 20% year-over-year, mirroring a similar decline in Q2 2024 compared to Q2 2023.

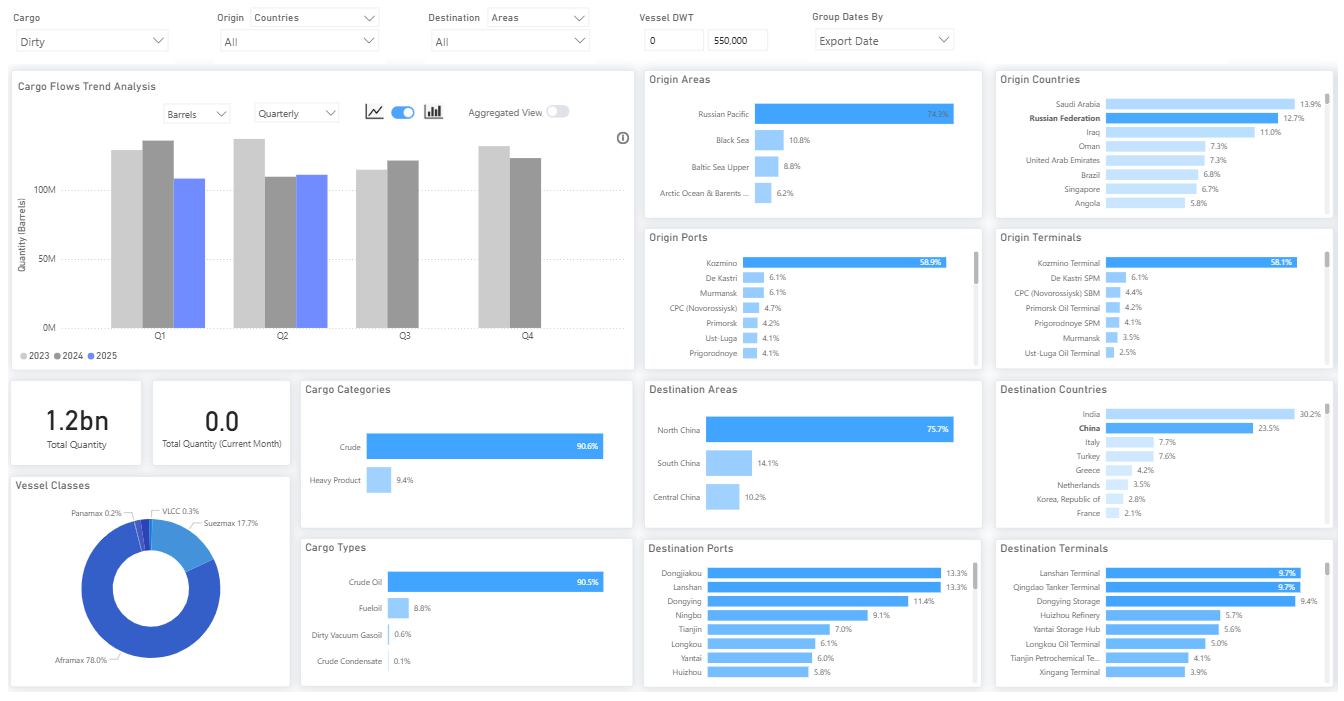

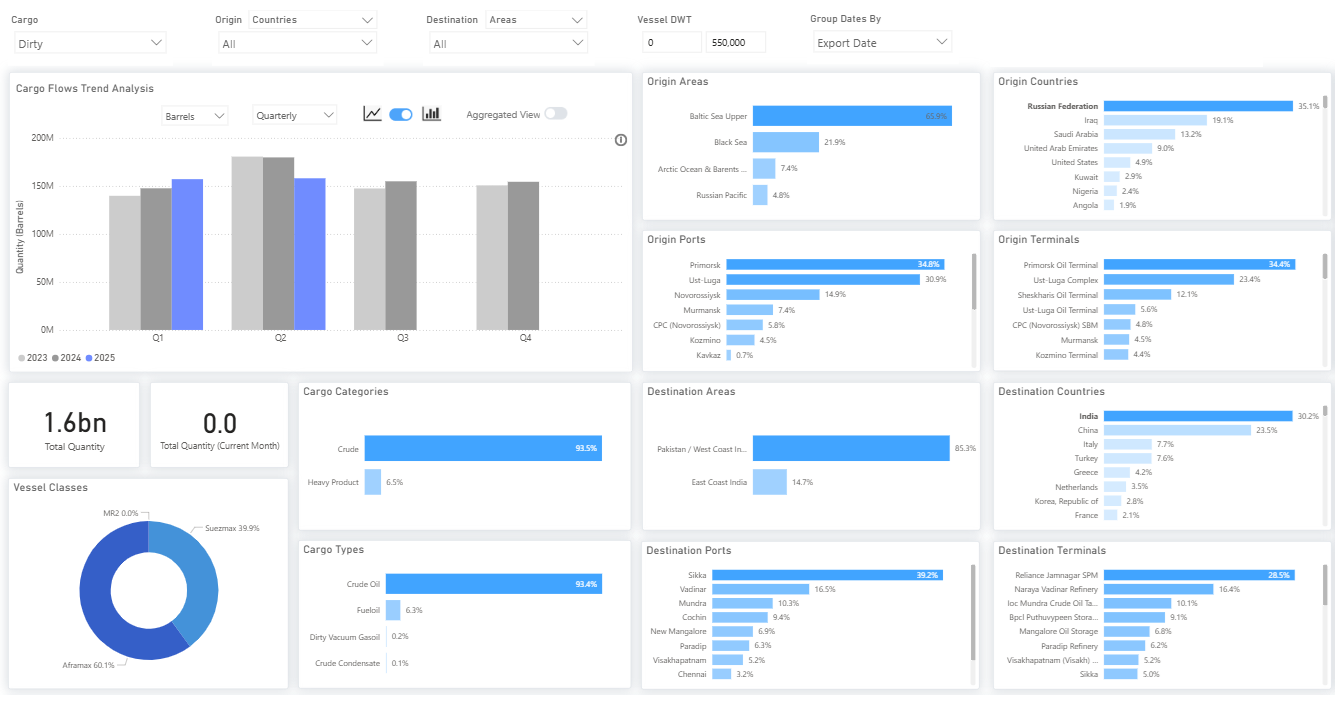

Indian import volumes show a more modest decline: quarterly volumes were nearly flat versus Q1 2025 and down roughly 12% year-over-year, though monthly data reveals a steady drop since March, with June shipments falling over 10 million barrels.

Russian Dirty Oil Flows to India (Quarterly)

Russian Dirty Oil Flows to India (Monthly)

It’s important to understand that Russia’s crude oil remains legally accessible in Asia. While the European Union and United Kingdom have unilaterally reduced the G7 price cap to $47.60/bbl, the United States has resisted endorsing the change, limiting the global enforcement power of the revised cap, especially given oil’s dollar-based trade and U.S.-controlled payment systems. Neither the U.S. nor the EU has banned crude exports to India or China. This suggests that the recent reductions in Russian crude imports by these two countries are more likely driven by market pricing than by sanctions avoidance.

As of July 18, 2025, Brent crude traded near $70/bbl, while Urals crude was priced around $58/bbl FOB, yielding a discount of approximately $12/bbl. While still meaningful, the current spread marks a widening from previous months when reduced Asian spot buying had temporarily narrowed the differential.

Several commercial and logistical factors are contributing to the reduced appeal of Russian spot crude. A larger share of Russian exports is now sold under term contracts, limiting spot availability. At the same time, higher domestic refinery runs in Russia are tightening export supply. These dynamics have gradually pushed Urals prices higher and reduced the arbitrage advantage for Asian refiners. As a result, price-sensitive buyers in India and China are likely scaling back opportunistic purchases, rather than executing any coordinated strategic shift.

This interpretation is further supported by tanker movements. In June, there was a marked return of Greek-owned tankers to Russia-linked trades, suggesting that logistical and compliance confidence has increased and that sanctions risk is being carefully managed, not avoided entirely.

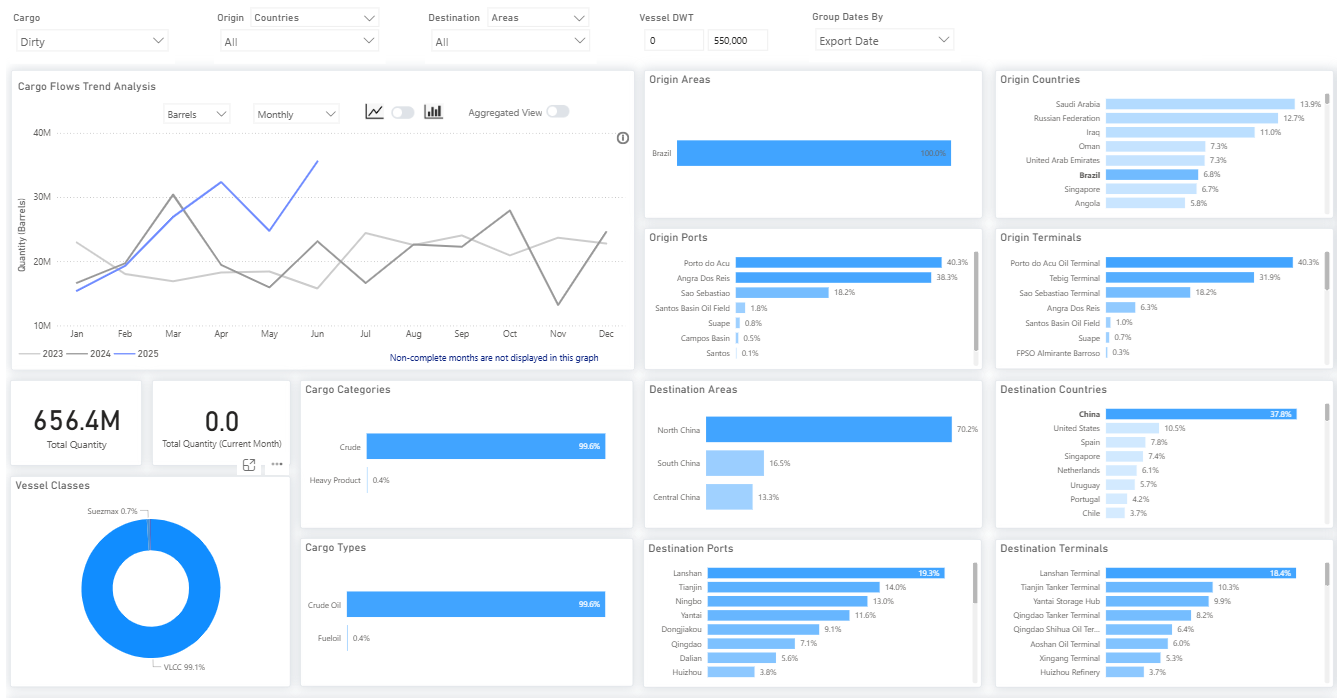

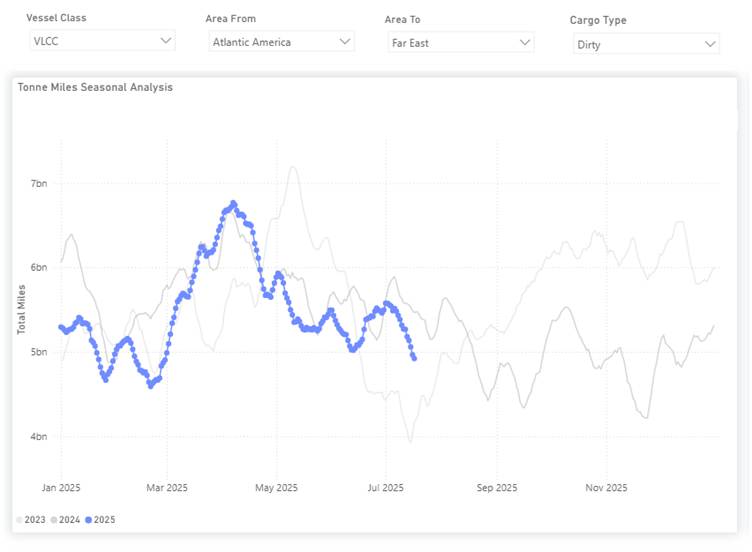

Meanwhile, Brazilian crude exports to China surged above 30 million barrels in June, nearly doubling from 16 million barrels in June 2023. These volumes largely consist of heavy-sweet grades, offering similar yields to Russian Urals and complementing China's diversification strategy. While the increase does not yet indicate a dramatic rise in tonne-miles, it suggests a more diversified supply map for China, driven primarily by seasonal demand and relative value.

This evolving pattern of longer-haul Atlantic Basin crude flows into Asia may push Europe to rely more heavily on Middle Eastern and U.S. supply. That rebalancing could impact U.S. refiners, particularly those optimized for light sweet grades, by altering feedstock availability, margins, and output strategies. At the same time, these shifts may support transatlantic clean product flows from the U.S. Gulf Coast to Europe, particularly for ULSD and, to a lesser extent, naphtha. This could increase demand for clean product tankers, especially MRs and LR1s. Meanwhile, gasoline exports are likely to remain concentrated in the Europe-to-U.S. Atlantic Coast trade.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)