drives these stories

The global economic recovery is facing a crossroads moment. The growth engine of the last eighteen months, China, is facing considerable headwinds, with growth and industrial production data disappointing in recent weeks. While the Chinese economic expansion was widely expected to moderate as the initial recovery phase faded out, the rapid deceleration has taken many pundits by surprise. Despite the slowdown, the country is on course of beating the official full-year growth target of six per cent. However, some analysts, most notably Citigroup and Bank of America, now expects the soft patch to extend into next year, with growth below five per cent. The current situation has been in the making for some months. The domestic economy has been lagging behind the export-driven industry and problems in the property sector. In addition, policies aiming at controlling surging commodity prices and pollution levels have contributed. The unravelling energy crisis has since, in combination with resurgent Covid-19 outbreaks, super-charged the challenges the Chinese economy is facing.

As the importance of China is fading somewhat, much of the focus of the growth narrative has shifted to other parts of the world. After a few difficult months, India is firmly on track to regain the designation as the world’s fastest-growing major economy. The International Monetary Fund expects it to expand by 9.5 per cent during the year ending in March. Many of the world’s developed economies have also joined the recovery path fuelled by extensive stimulus programmes. However, the route has become increasingly rocky as the supply chain disruptions have limited the upside for the industrial production recovery.

Energy Crisis – Oil Prices

While the global economic recovery faces a fair share of headwinds, the unfolding energy crisis has been the real headline grabber during the last month. Several factors have aligned to cause an extensive energy supply crunch, with prices rising rapidly. In China, low inventories following last winter’s cold weather and reduced domestic coal production forced many buyers to seek additional supplies from overseas. Due to limited supplies and soaring natural gas prices, the global coal demand has also been pushed higher as many countries and utilities switch from natural gas to cheaper coal.

Crude oil prices have ventured ever higher, perhaps somewhat in the shadows of developments in thermal coal and LNG markets. West Texas Intermediate hit a seven-year high in late October at 84.65 dollars while gaining eleven percent during the month. Brent recorded a somewhat more modest seven per cent gain in October and traded near a three-year high as the month came to an end. Growing signs that the global economic recovery is fuelling a growth in demand that is outpacing the limited output increase and draining stockpiles have contributed to the price surge.

In addition, the ongoing natural gas and coal shortages across Asia and Europe have supported the month’s oil price advance. The demand outlook for refined products such as diesel, kerosene and propane has improved ahead of the winter, buyers seeking substitutes for the other energy commodities in short supply. As a result, profit margins for the refineries have returned to healthy levels following last year’s challenges. The trading in Nymex gasoline crack, often used as an approximation for refiners’ margins, ended the month at sixteen dollars a barrel, the highest for the season since 2017. Profit margins are also rising across Asia and Europe, suggesting many refiners will continue to process more to meet demand, and global oil stockpiles will continue to shrink in the coming months.

In China, the supply issues surrounding coal and natural gas have led to a shortage of diesel, prompting the fuel to become rationed. Chinese authorities have met with the nation’s refiners in a bid to stave off further disruptions and surging prices. According to reports, officials questioned the refiners if they could raise processing rates to produce more fuel and import more diesel and gasoline. In addition, the ability to source additional crude oil at reasonable prices to avoid adding to the nation’s inflationary pressures remains a concern. In a well-published attempt to control the rising prices, China also released seven million barrels of crude from its strategic reserves. While being a historic first, the quantities account for less than a day’s consumption in the country.

OPEC+ Production

The oil-producing countries are unlikely to come to the rescue anytime soon with increased output, with OPEC+ intent on remaining the custodian of price support. The organisation remains fully committed to the production deal reached in July, which sees the group adding 400,000 barrels a day to supply each month. The pact will see all production cuts removed in September next year, assuming that demand is recovering as projected and there is no significant resurgence of the coronavirus affecting the economic growth materially. Despite increasing diplomatic pressures, notably from the US, there are no indications of the organisation relenting, with the agreement reaffirmed multiple times. The cartel’s Joint Technical Committee has also softened its expectations for how tight global oil markets will be this quarter, ahead of the next ministerial meeting in early November. Its original forecast of 1.1 million barrel daily deficit during the fourth quarter was downgraded to an average of 300,000 barrels per day. However, the committee expects the shortage to turn to a surplus of 1.6 million barrels a day next year as non-OPEC production recovers.

Assuming OPEC+ maintains its planned course of action, traders increasingly believe that 100 dollars a barrel is rapidly approaching. Analysts at Bank of America are even more bullish and anticipate that crude oil will reach 120 dollars by the middle of next year.

The strength of the crude markets is, to a great extent, a testament to the newfound ability of OPEC+ to manage much of the global output of crude oil. Perhaps the most surprising aspect of the OPEC+ agreement is that it still holds, as production quotas in the past often had only limited success. It also highlights the extensive drop in demand that the oil-producing countries perceive that they are facing. Previously, compliance among the cartel members concerning output quotas tended to be somewhat limited under normal market conditions. However, with the extensive production cuts in the wake of the pandemic, there is enough spare capacity to ensure mutually assured destruction in the crude oil market should extensive cheating take place. A widespread failure to adhere to the agreement would see crude oil prices dropping to very low levels, which is unlikely to suit any producer at this stage. Hence, in the current environment, the traditional outcome of game theory experiments in Economics that cheating is the most rational approach, assuming that everybody else is not, is no longer valid. The newfound conformity is obviously good news for the credibility of the OPEC+ arrangement and the wider organisation. Still, tanker owners are likely to wish for a bit less compliance with higher output and lower prices.

News that international talks with Iran over its nuclear programme initially saw oil prices falling, as traders expected it to end the sanctions on Iranian oil exports. However, the early excitement wore off as the extent of the challenge ahead sank in. The newly-elected hardline Iranian president and a demand that future US administrations can not withdraw from any agreement, like the previous one, are likely to complicate matters. According to official statements, the first meeting will take place before the end of November. If the meeting comes to a successful conclusion, it will benefit the freight rates in the tanker sector, as a cash-strapped Iran is likely to try to maximise its exports. Additionally, the vintage tonnage used for sanctions-busting shipments of Iranian crude oil should become surplus to requirements and candidates for scrapping.

Freight Market

While other shipping sectors, most notably container and dry bulk, are seeing some of the best markets in recent history, there is minimal upside for the crude tanker market at this stage, and freight rates look likely to remain near the historical lows. The factors that benefit those sectors are also the reasons for the travails of the crude and product sectors. The pandemic has brought about a focus on consumption and investments in infrastructure, as large parts of the global population are either banned from travelling or simply reluctant to venture too far from home, which has harmed the demand for petroleum products. In addition, pandemic related disruptions in and around many important ports have driven congestion to historically high levels and contributed to a shortage of tonnage in those sectors.

The relative outperformance of the eastbound trade from the Arabian Gulf highlights the importance of the rapid Chinese economic recovery to the global demand growth. The unfolding energy squeeze also contributes, as refiners have come under pressure to increase output to make up for coal and natural gas shortages. In addition, the Chinese habit of opportunistic purchases for its strategic reserves has also supported freight rates to the Far East.

VLCC Freight Market Performance - AG to Far East / AG to USG

MR2 Clean Freight Market Performance - Cont to US Atlantic, US to Continent - MEG to East Africa

With winter approaching in the Northern Hemisphere, it traditionally heralds the peak demand season for the tanker markets. However, any lingering optimism among tanker owners for the months ahead is likely to be relatively short-lived. While a seasonal pickup in demand for oil should be on the cards, the extent ought to be modest compared to previous years. The strict output management by OPEC+ could also add insult to injury for the tanker owners, as the anticipated rise in crude prices will push bunker prices higher and offset much of any potential gains in freight rates.

While the rising crude oil production should be welcome news for tanker owners, the limited scope of the monthly increases means that it will take quite some time before any critical mass is achieved, and freight rates can rise above breakeven. VLCC tanker rates have been trending higher in recent months, but as the market remains oversupplied, the upside has been limited.

Tonnage supply

A continued arrival of new tonnage and an absence of extensive scrapping are adding to the sector's woes, which is likely to increase the interest in transporting clean products onboard vessels typically used for dirty cargoes. This spillover could put product tanker rates under some pressure, which so far has remained in relatively better shape than dirty cargoes. While the supply situation in the product tanker segment has remained relatively stable in recent months, a sudden influx of tankers from the dirty trade would be unwelcome news by the owners in the segment, which still is facing surplus tonnage.

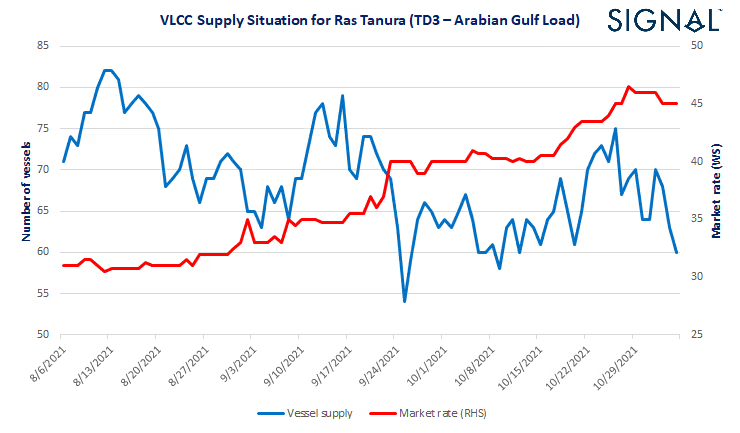

VLCC Supply & Market Rates (WS)

MR2 Clean Supply & Market Rates (WS)

Market Prospects

The dirty tanker markets may be facing their winter of discontent, as OPEC+ keeps supply growth under control to preserve high prices. With the bruising effects of last year's oil price war between Saudi Arabia and Russia still in fresh memory, the group has the incentives to maintain compliance with the production cuts. In their base case, OPEC's analysts expect global consumption to almost return to pre-pandemic levels during the following year. Under such a scenario, the analysts expect the oil supply-demand balance to revert to a surplus if the group increases output as scheduled. The inventories would build even more in their alternative, more pessimistic scenario, which sees demand at around two per cent below the pre-pandemic levels. The build-up in oil inventories from a market in surplus would be beneficial for tanker rates, with demand for seaborne transportation and storage increasing. However, oil prices would come under pressure, and OPEC+ may see itself forced to re-impose production cuts to keep prices high, resulting in a drop in demand for tanker tonnage. Hence, killing any notion of higher oil prices supporting healthy freight rates. It could be argued that demand-driven higher prices would encourage higher charter rates. Still, if higher demand is driving prices substantially higher, it would suggest the supply situation is tight and seaborne volumes may suffer as a result.

At the same time as the dirty tanker market looks set for a protracted recovery, the seaborne transportation of refined products is likely to continue to fare somewhat better. The global rebound in economic activities, notably in land-based transports and air travel, is expected to fuel continued growth in demand for petroleum products. As OPEC+ looks unlikely to lend a hand, a continued drawdown of global stockpiles of crude and products is the likely outcome, which will lay the foundation for broader recovery during 2022.

To generate the same insights for your business and learn more about The Signal Ocean platform, contact us here.

-Republishing is allowed with active link to source

Ready to get started and outrun your competition?

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)