Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

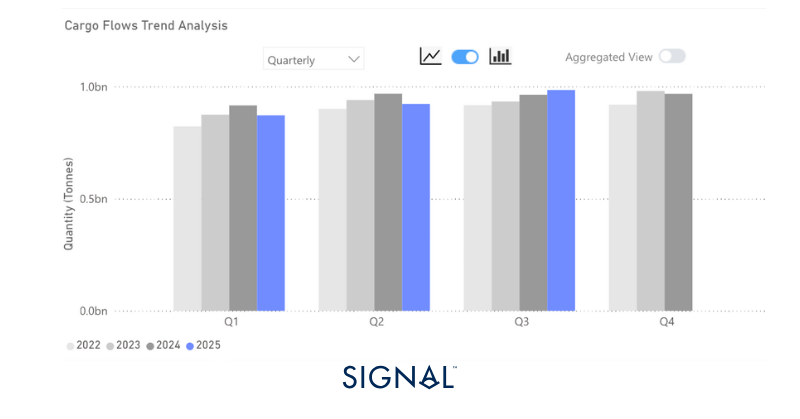

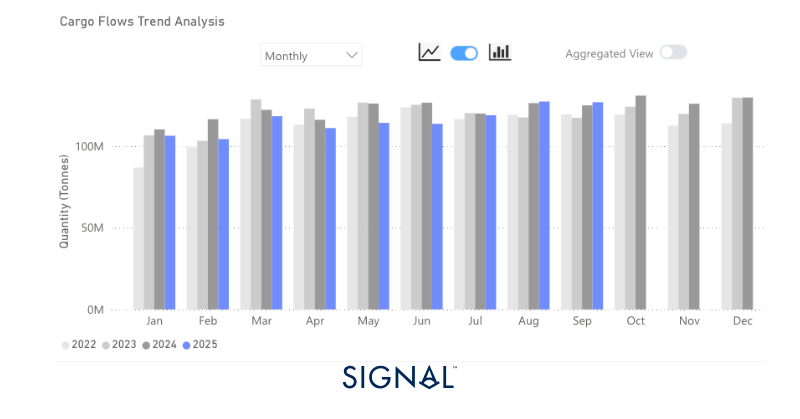

Major bulk, made up of iron ore, coal, and grains, exports ended 2025 Q3 above the previous year and sit as the quarter with the highest volume of major bulk exported on the Signal Ocean Platform. Demand from China across all these major bulks helped to drive this, with September being particularly notable for coal and grain demand.

Source: Total major bulk* export performance from Signal Ocean.*Major bulk is made up of iron ore, coal, and grains.

Economic Environment

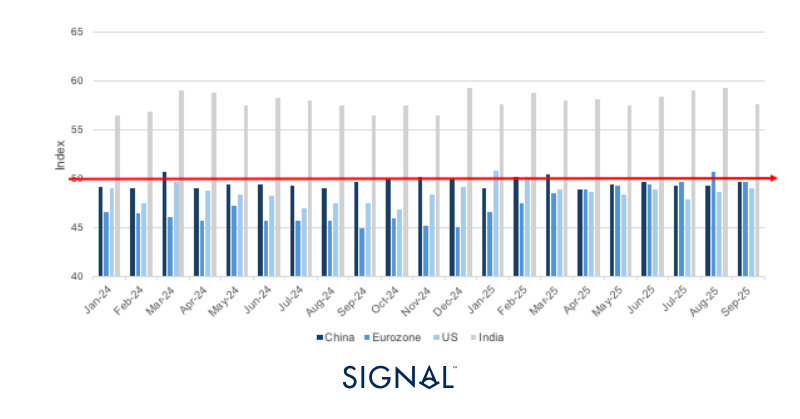

Manufacturing PMI’s

Source: National Bureau of Statistics of China, Institute for Supply Management, HCOB, HBSC India Manufacturing PMI

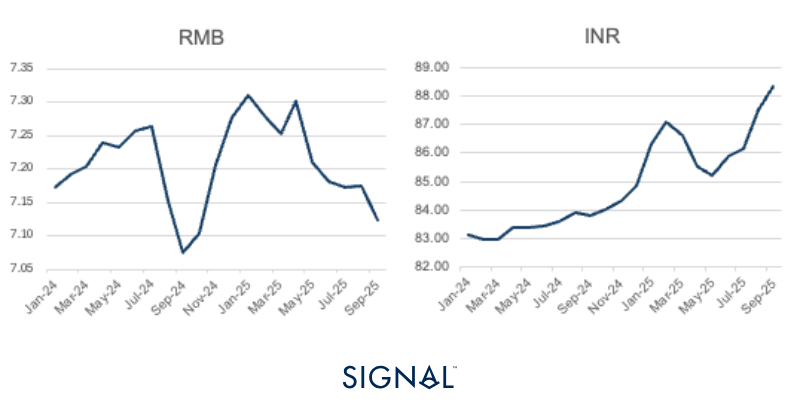

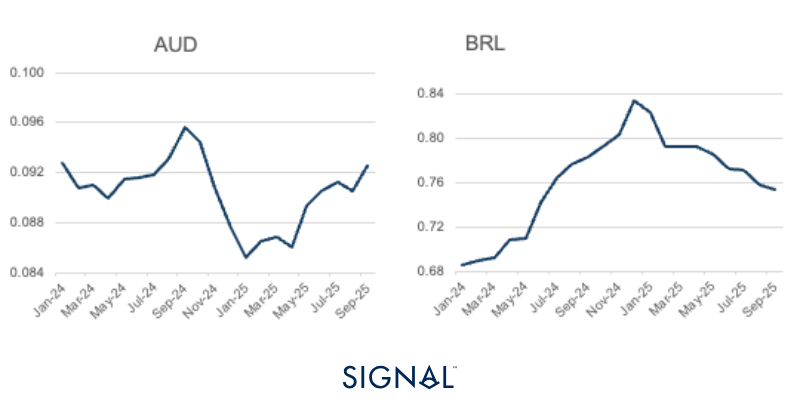

Exchange Rates

USD vs:

RMB vs:

Source: IMF

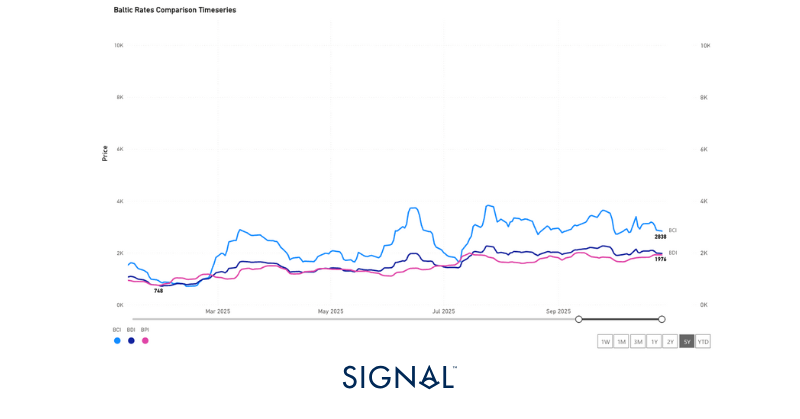

Baltic Indexes

Source: The Baltic Exchange

Major bulk

Iron ore

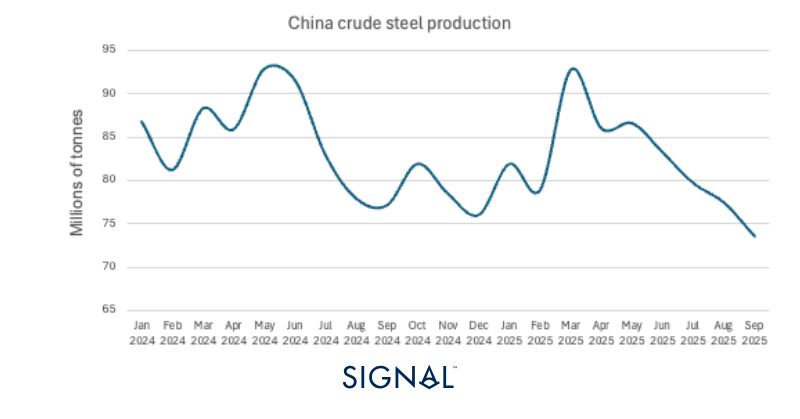

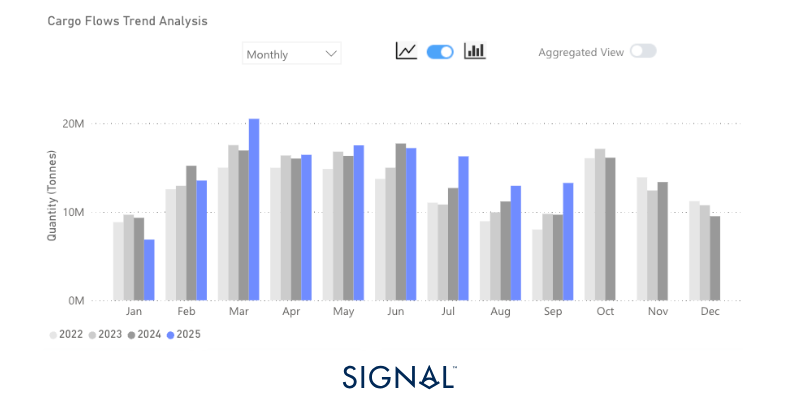

The Signal Ocean platform recorded global iron ore exports at 154.1mt in September, up 2% y/y but down flat m/m. This has been driven by record imports of iron ore into China, which reached 118mt in September. The record import of iron ore into China runs counterintuitively to the current performance of the Chinese steel industry.

So far in 2025, China has produced 746mt of crude steel, down 3% on the same period from last year, with the last four months to September showing consecutive monthly decreases. As a result of both the increased exports and lower steel production, iron ore port stocks in China have reached multi-month highs by mid-October. This may weigh on iron demand in the coming months, and could see a contraction in iron ore imports in October and November, which is common in recent years.

Furthermore, BHP announced at the start of October that the state-run iron ore buyer (CMRG) had placed a halt on buying any of its products due to pricing disputes, and put pressure on others in the country to follow suit. The dispute focuses on the CMRG wanting a discount on the lower-grade iron ore it has been purchasing, with BHP holding firm on its price offering. CMRG also wants more of the purchasing to be conducted in RMB rather than USD. There have been unconfirmed reports that 30% of CMRG spot dealings with BHP will be conducted in RMB starting from Q4 2025. Read more here.

More recently, stories have broken out detailing that BHP has managed to sell some tonnage to Chinese traders, outlining that some in the market are willing to take deliveries of iron ore. Still, with the negotiations between BHP and CMRG still at a standstill, and Chinese iron ore stocks at a multi-month high, it would be logical to expect imports of iron ore into China to soften before the end of 2025.

Source: Global monthly iron ore exports from Signal Ocean

Source: China crude steel production from the National Bureau of Statistics of China

Source: Australia to China iron ore exports from Signal Ocean

Coal

The Signal Ocean Platform data indicated that global coal exports reached 127mt in September, effectively flat month-on-month but 2% higher y/y. The modest annual increase was supported by a 4% rise in thermal coal shipments, underscoring steady demand despite broader volatility in the energy market.

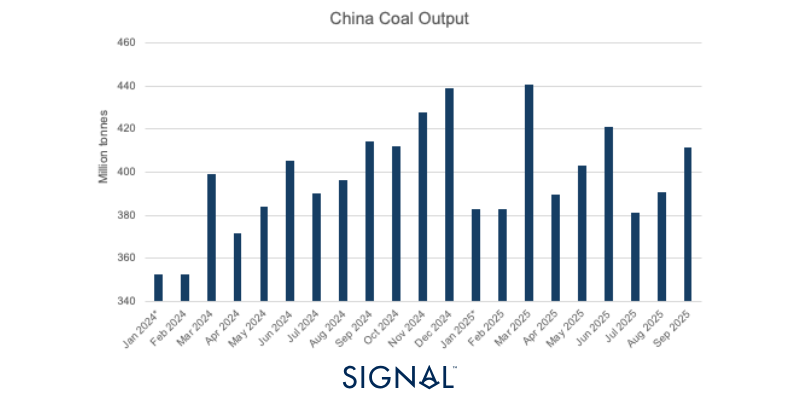

The strength in thermal coal flows was concentrated in East Asia, where demand has remained firm since surging in August. In China, restrictions on domestic coal production have tightened supply, keeping it lower than last year's production, and pushed domestic prices higher, enhancing the relative competitiveness of imported coal. At the same time, robust manufacturing and power generation activity across other East Asian economies, notably South Korea and Japan, has sustained regional import demand. South Korea saw imports of thermal coal up 47% y/y in September, and Japan's imports were up 5% y/y.

The short-term demand picture for thermal coal is positive. China will continue to restrict output from its domestic coal mines, limiting supply at a time when the East Asian region heads into winter and there is typically higher power demand. Australia is the most likely to step in and supply the coal, as we have already seen thermal coal exports surge by 21% in September, heading mostly to East Asia.

The longer-term outlook, however, is not as positive for coal demand. China, the world's largest consumer of coal for electricity generation, has invested heavily in renewable energy infrastructure to provide adequate base load for power in the coming years. There has been a high rate of new coal power stations being commissioned, with 2025 H1 seeing the largest amount of coal-fired capacity being added since 2015, but this was to be expected given the 2030 peak carbon deadline set by the Chinese government. From 2030, coal demand in China will consistently soften.

Source: Total coal export volumes from Signal Ocean

Source: China domestic coal production from the National Bureau of Statistics of China

Source: South Korea vs Japan coal import statistics for September 2025 from Signal Ocean

Grains- Soybeans

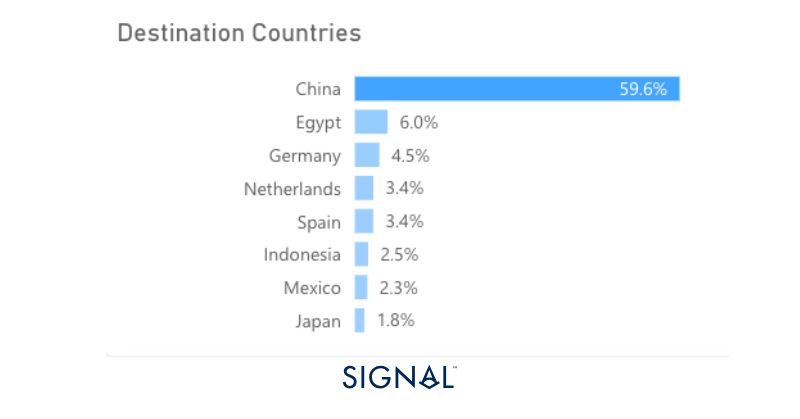

Signal Ocean measured global soybean exports reached 13.3mt, up 37% y/y. China, the largest consumer of soybeans globally, saw imports of soybeans surge 66% in September, driving the global increase in exports. From 2022 to now, China has received 21% of all its soybean imports from the U.S. However, in September 2025, no U.S.-origin soybeans were discharged in China for the first time since 2018. We explored the new sources in a previous article here.

The tariffs imposed by China on U.S. soybeans have been what the market has pointed to as the reason for this drop off. Those soybeans arriving in China from the U.S. before September are from previously harvested supplies. The absence of any U.S.-origin soybeans arriving in China from September 2025 shows that none of the latest harvest of U.S. soybeans has been purchased by Chinese buyers.

Without a positive resolution to the trade talks between the U.S. and China, U.S. farmers will come under pressure, as buyers in other countries are unlikely to require the volumes that China typically purchases. The move could also impact China at the start of next year, when Brazil enters its harvest season, as there is no indication of how much old crop Brazil, the largest supplier of soybeans to China, has left. This could see Chinese buyers look to U.S. soybeans over this period to keep the flows incoming.

Source: Global soybean exports from Signal Ocean

Source: Origins of China soybean imports in September 2025 from Signal Ocean

Source: Destination for U.S.-origin soybeans since 2022 from Signal Ocean

Luke has over 8-years of experience analysing and forecasting commodity markets, with particular expertise in stainless steel raw materials and the wider metals markets.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)