Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Chart of the Week: Iron ore Freight Market Trends

This week’s analysis examines iron ore freight market trends with a special focus on the emerging iron ore supply powerplay: Simandou’s Rise, Vale’s Moves, and BHP’s Growing Risk

The Simandou project is advancing through key development milestones and is set to introduce a significant new stream of high-grade iron ore into the global market.

Vale S.A. is intensifying its strategic engagement with India as it seeks long-term growth opportunities beyond its traditional customer base.

BHP Group remains heavily exposed to China’s iron-ore demand; with new supply entering the market and trade dynamics shifting, its strategic risk is increasing.

China’s steel demand has entered a near-plateau phase — growth has largely stalled and may now be moving into gentle decline, as structural headwinds accumulate.

Spotlight of the Week: Market Pulse | Capesize Freight Market Overview

Atlantic Capesize sentiment has strengthened despite high ballast supply, while the Pacific C5 route has softened as November shipments from West Australia decline. At the same time, Brazil’s iron-ore share in China faces its first serious competitive threat in years with the long-anticipated emergence of Simandou. These market shifts are occurring alongside important changes in China’s procurement strategy. The state-backed China Mineral Resources Group has expanded its ban on select BHP iron-ore products as contract negotiations stall, signaling that Beijing is asserting greater procurement leverage.

Capesize Ballasters Vs Baltic Rates

Over the past month, Atlantic Capesize sentiment has firmed as the ballaster supply picture has tightened. The decline in available ballasters, after the late-summer peak, has helped stabilize freight levels despite ongoing volatility. At the same time, Brazilian iron ore’s position in the Chinese market is facing growing competitive pressure from Simandou’s gradual ramp-up, adding a new layer of uncertainty to C3 flows and rate performance.

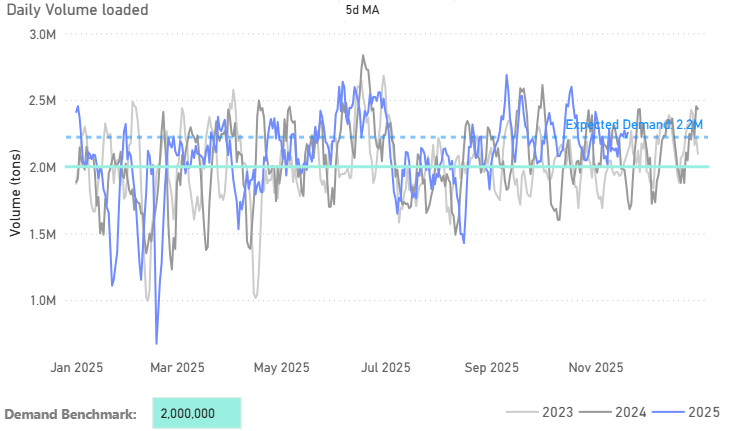

In the Pacific, C5 sentiment has softened as November’s West Australian daily volumes dipped below the 2.1–2.2 Mt demand range, putting renewed downward pressure on rates.

The key question is no longer whether Simandou will matter, but how quickly new supply corridors will alter medium and long-term capesize freight demand and vessel utilisation.

Simandou & Vale’s India Pivot

Two developments are reshaping iron-ore trade patterns: the launch of commercial operations at Simandou in Guinea and Vale’s growing focus on supplying high-grade ore to India. Taken together, these shifts point to a scenario in which 2025–26 could see the first meaningful expansion of long-haul iron-ore routes beyond the dominant Australia–China and Brazil–China corridors. In such a scenario, tonne-mile demand would likely increase, though this would not necessarily alter the central role of today’s major high-volume routes.

Simandou’s Breakout Moment

Simandou has entered its export phase: the first ore shipment departed on 18 November 2025. The development, which includes a 650 km railway and deep-sea port, is designed for full capacity of up to ~120 million tonnes per year of ~65 % Fe ore. The southern block JV (Rio Tinto/Chalco) has a ~30-month ramp-up plan, and the West Africa-China haul is significantly longer than the Australia-China route, enhancing tonne-mile demand.

Vale’s India Pivot

Vale is increasingly positioning India as a crucial, long-term growth market for its high-grade Brazilian iron ore, viewing the Brazil–India route as a potentially significant second structural tonne-mile driver for the seaborne trade. This new pillar is expected to supplement, rather than replace, the established Australia–China (C3) and Brazil–China (C5) trade lanes.

This strategic pivot is driven by India's rapid expansion of steelmaking capacity and its aggressive infrastructure agenda. Vale highlights that its premium ore is an excellent complement to India's lower-grade domestic supply, enabling Indian mills to boost productivity and lower emissions.

While China remains the primary destination for Vale's shipments, India presents a distinctly upward trajectory. Vale projects that Indian steelmakers will lift their capacity toward the 300 Mt level over the next five to seven years, thereby opening a new, durable demand channel for long-haul Brazilian ore.

But Substitution Remains Premature

Australia’s Pilbara region maintains a clear advantage in export scale, unit costs, and supply reliability. With annual exports consistently in the 750–800 million-tonne range, Pilbara capacity remains far larger than any emerging supply source.

Australia’s South Flank: The Quiet Counterweight

BHP’s South Flank continues to reinforce Pilbara’s structural edge: scale, reliability, and highly integrated mine-rail-port infrastructure. This remains the benchmark system against which all new entrants must compete. Even with pressure from Simandou, Australia’s cost-efficient export platform remains deeply entrenched.

Risks from the New Iron Ore Supply

The Simandou high-grade iron-ore deposit requires the construction of a heavy-haul railway of roughly 600–650 km from the mine site to the Atlantic coast of Guinea, together with a newly built export port. The combination of long distance, challenging terrain, and substantial up-front infrastructure is expected to create significant operational constraints for the project. This logistics chain has not yet been tested at full export capacity. Major West African mining developments, including Simandou, have historically faced delays and cost increases, indicating that the risk of a slower-than-planned ramp-up remains substantial.

What’s Next: Shifting the Balance, Not the Center of Gravity

Simandou brings diversification, not displacement. Vale’s India push adds route expansion, not substitution. Together, they redraw trade lanes, boost tonne-miles and strengthen Capesize utilisation, all while the Pilbara stays at the core of global iron-ore flows.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)