Minor bulk exports opened Q4 with steady growth, carried by stronger Chinese demand, firm rice flows, and shifting dynamics in bauxite and scrap steel.

Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

China’s renewed appetite and shifting trade patterns lift volumes across key minor bulk commodities

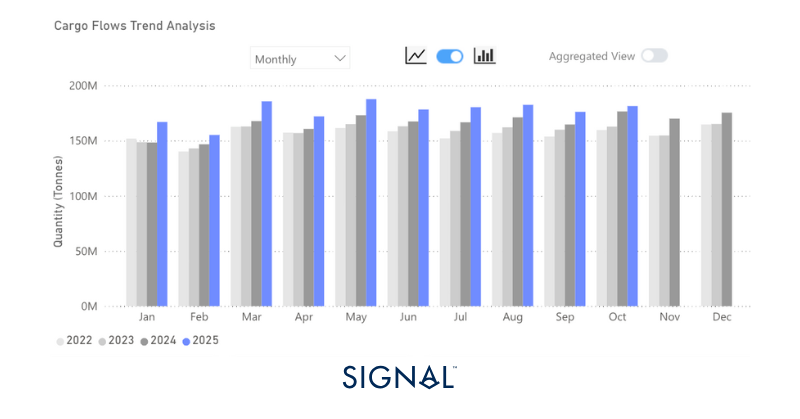

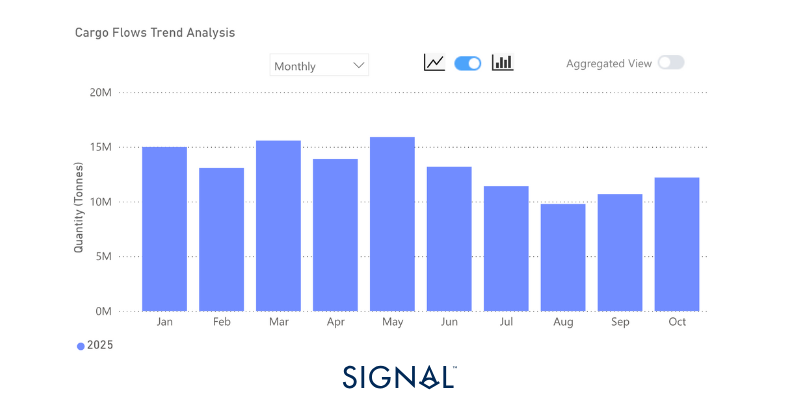

Minor bulk, made up of all cargo types except iron ore, coal, and grains, started the first month of 2025 Q4 with positive momentum, with total export volumes up 3% y/y. This has been driven by China, which has seen imports of minor bulk increase by 14% y/y in October 2025.

Source: Total minor bulk* plus rice export performance from Signal Ocean.*Minor bulk is made up of dry bulk that is not categorised as iron ore, coal, or grains. It includes bauxite, cement, steel, and fertilizers, among others.

Economic Environment

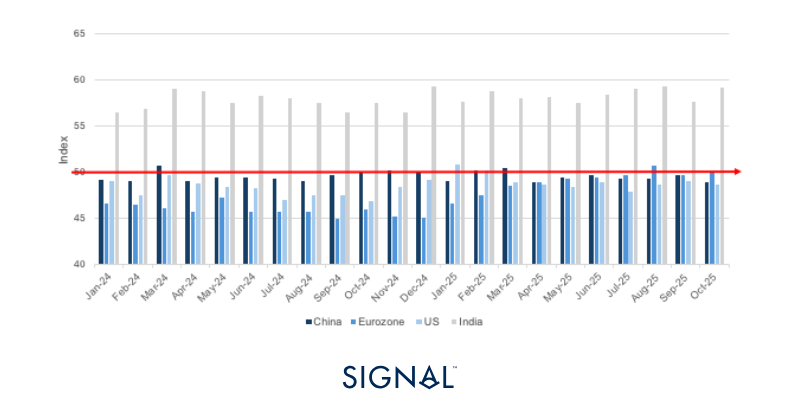

Manufacturing PMI’s

Source: National Bureau of Statistics of China, Institute for Supply Management, HCOB, HBSC India Manufacturing PMI

Exchange Rates

USD vs:

RMB vs:

Source: IMF

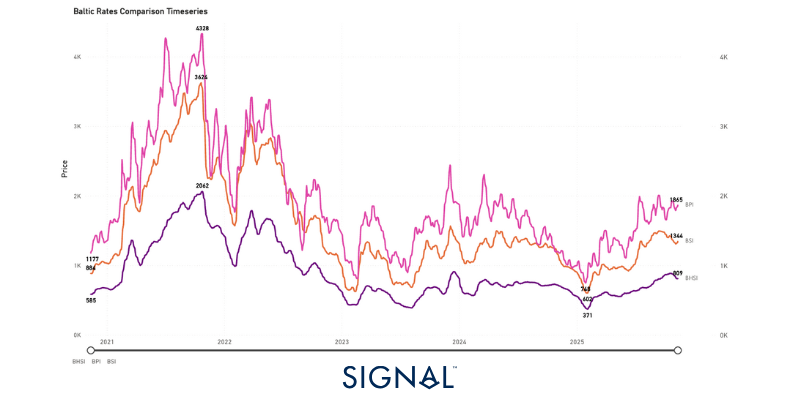

Baltic Indexes

Source: The Baltic Exchange

Minor bulk

Bauxite

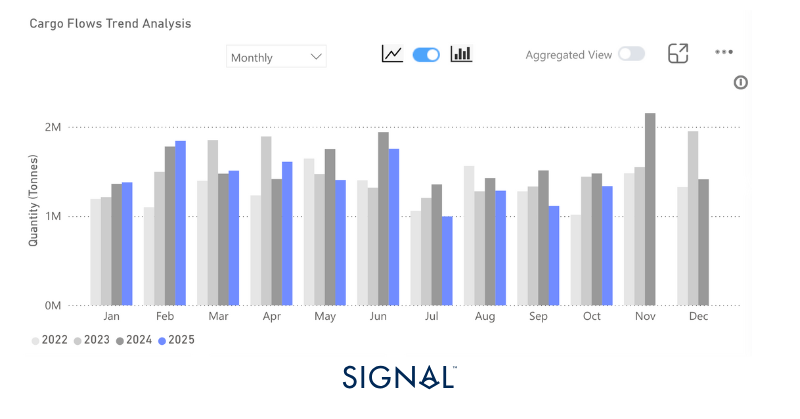

The Signal Ocean platform recorded global bauxite exports in October at 19.6mt, flat m/m. The figure for October marks the first time in 2025 that a monthly export figure of bauxite has not been up y/y, remaining flat on the October 2024 figure.

The bauxite market typically shows seasonality, with the final quarter stronger than the preceding three. The third quarter tends to see the lowest volume of exports. The final quarter of 2025, though, has started weaker than in previous years. From 2022 to 2024, October exports grew by 7% to 17% m/m, but in October 2025, exports remained flat.

A more bullish outlook was provided with the signing of a 1.5mt sales agreement by Guinea state-owned miner Nimba Mining Company (NMC), which took over operations of the Tinguilinta mine from the Emirati-owned Guinea Alumina Corporation, and buyers in China. NMC has already shipped the first 200kt of this contract.

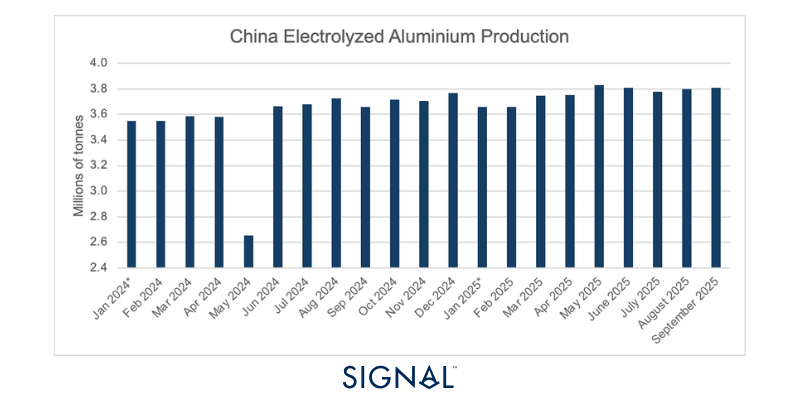

We could see bauxite exports from Guinea come under pressure from 2027. We previously mentioned that the Guinean government has been looking to revoke mining licenses for bauxite operations that do not invest in domestic processing facilities to convert Guinea's abundant bauxite into the higher-value product, alumina. Now, Guinea has signed its first alumina refinery deal with China’s state-owned SPIC, with construction of the facility due in 2027.

In the time from now until then, exports of bauxite from Guinea could increase as buyers look to front-load purchases of material before any interruptions that may come from government policies of domestic alumina production. This will be beneficial for capesize demand, with the Simandou project also helping to boost capesize demand from Guinea through 2026 and beyond.

Source: Global monthly bauxite exports from Signal Ocean

Source: China aluminium production from the National Bureau of Statistics

Source: Exports of bauxite from Guinea in 2025 from Signal Ocean

Scrap steel

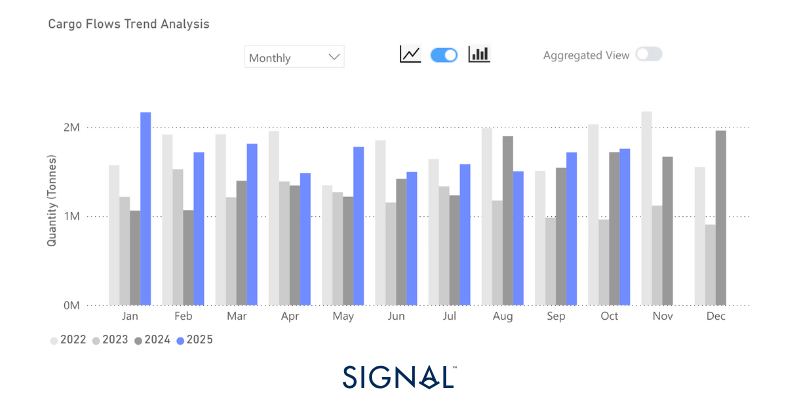

The Signal Ocean Platform recorded scrap metal exports at 1.3mt in October 2025, down 10% y/y but up 20% m/m. Given the uses of scrap steel, the demand drivers are intrinsically aligned with the performance of steel mills.

Turkey is the key destination for scrap metal, accounting for over 62% of all imports since 2022, according to TSOP. This is due to Turkey’s large steel-making capacity, currently sitting 7th in the global steel producers table. It is the way Turkey produces steel that drives its need for scrap metal, though.

Turkey produces a significant portion of its steel through electric arc furnaces (EAFs) rather than blast furnaces (BFs). An EAF uses scrap steel as its primary feedstock, unlike a BF, which cannot melt scrap steel, so it needs primary raw materials, such as iron ore, coal, etc, to produce steel. Turkey does not have enough domestic scrap steel due to some key drivers. Turkey is not a large enough producer of appliances or cars to generate enough scrap through those manufacturing processes, and the industrial base within Turkey does not produce enough prime scrap. Adding to this is the lack of suitable quantities of obsolete scrap, which comes from demolitions or appliances at the end of their life cycle. Therefore, to feed Turkey’s growing EAF capacity, the nation relies heavily on imported scrap.

Currently, Turkey has seen scrap steel imports down 15% YTD. The World Steel Association states Turkey’s crude steel production in 2025 from January to September was 28.1mt, up less than 1% from the same period last year. Yet, exports of Turkish steel products are performing well, up 15% YTD, and are particularly strong to Europe. Steel production in the EU is down around 4% YTD, so Turkish products can find buyers.

Source: Total scrap steel export volumes from Signal Ocean

Source: Destination of scrap steel exports from Signal ocean

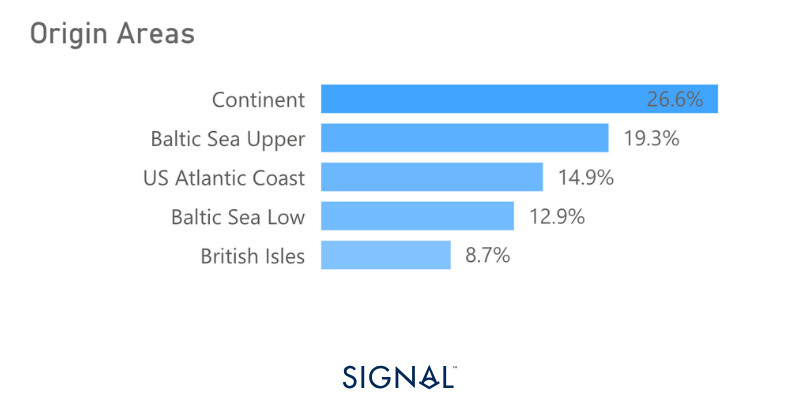

Source: Origin areas of scrap steel exports from Signal Ocean

Rice

Signal Ocean recorded global rice exports at 1.8mt in October 2025. This figure represents a 6% increase in m/m and y/y. India and Thailand dominate the export market, accounting for over 50% of all rice exports recorded by Signal Ocean since 2022.

Indian exports have been boosted in recent months following the scrapping of a minimum price of non-basmati rice in October 2024. This has led to rice exports from India reaching a 55% increase YTD. The majority of these exports have been sent to West Africa, with Senegal and Benin dominating. The reason for West African dominance is a result of rapid population growth, which has outpaced domestic capacity. Rice also benefits from its ease of preparation compared to more traditional West African staples like yams or millet. This will continue to help drive demand as these West African nations continue to urbanize.

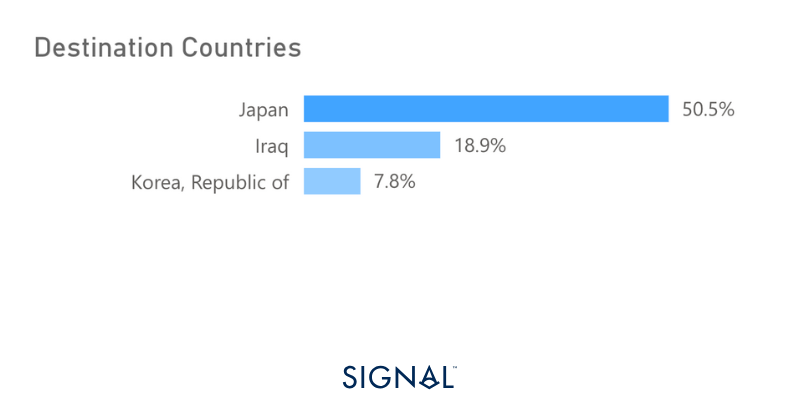

Across the Atlantic, the U.S. is expected to see a surge in rice exports to Japan. Over the summer of 2025, Japan agreed to purchase $8 billion worth of agricultural goods from the U.S. and increase rice imports by 75%. Japan is the largest importer of U.S. rice, accounting for over 51% of all U.S. rice exports since 2022. Japan has faced domestic rice shortages over the past year, leading to prices spiking for the staple. This agreement gives Japan control over the quantity and quality of rice imports, while helping to alleviate domestic food insecurity.

Looking ahead, an increase in the magnitude agreed to by Japan would drive Handysize demand out of the West Coast of the U.S., given that Sacramento is the dominant origin port for U.S. rice exports.

Source: Global rice exports from Signal Ocean

Source: Origins of rice exports from Signal Ocean

Source: Destination for U.S.-origin rice exports from Signal Ocean

Luke has over 8-years of experience analysing and forecasting commodity markets, with particular expertise in stainless steel raw materials and the wider metals markets.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)