Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

TANKER MARKET MONITOR |Tracking VLCC freight momentum and the latest Russian flow shifts

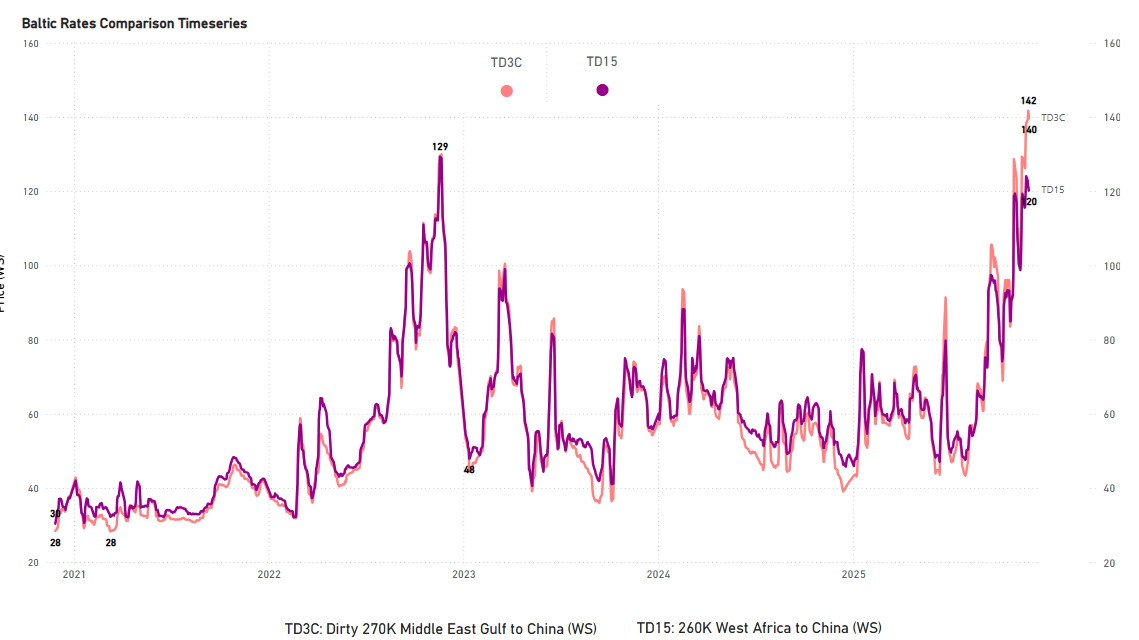

TD3C and TD15 stay at multi-year seasonal highs as the rally continues to push on

AG/WAFR net supply remains tight, with early signs of a renewed upward push

Nov 21-sanctioned Russian flows remain a critical market watchpoint

TD3C: 52-Week High142 | TD15: 52-Week High 124

This week’s analysis focuses on VLCC performance and the evolving Russian crude flows. Building on our October and November Special Editions, we have already outlined the main drivers behind the recent market surge. In the November edition, we emphasised how structural inefficiencies are increasingly shaping market behaviour, reflected in elevated tonne-days despite relatively softer tonne-mile growth.

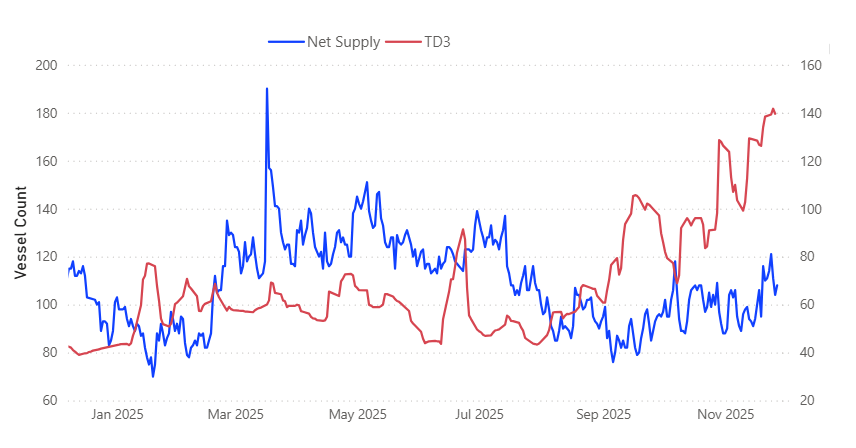

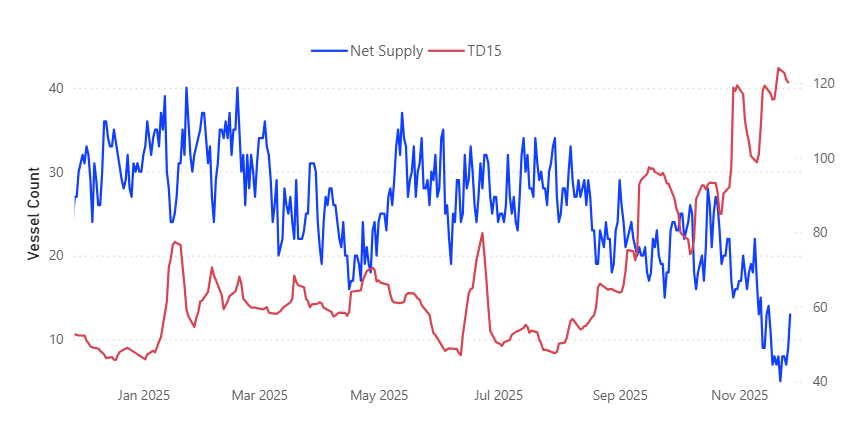

In this follow-up, we examine how freight prices and vessel supply interact to influence short-term market direction, with a particular focus on net supply dynamics from the Arabian Gulf (AG) and West Africa.

Trend Reversal: Late November shows a noticeable easing, with the 21-day MA around 30% below end-October.

India has not completely halted purchases of Russian crude. November arrivals are on track to reach a multi-month high as refiners front-loaded purchases ahead of the U.S. sanctions deadline. However, the TSOP 21-day moving average of Russian flows has already declined from its late-October peak and is now trending lower following the U.S. measures on Rosneft and Lukoil, announced in late October and effective from 21 November. Together with the sanctions wind-down, this points to a sharp drop in arrivals from December onward. Although Indian refiners can still buy Russian crude from non-sanctioned intermediaries, several developments indicate that inflows are likely to continue falling, rather than stabilising or rebounding:

Following the U.S. sanctions announcement, Reliance Industries accelerated its exit from Russian crude at its export-oriented SEZ refinery at Jamnagar. The last Russian cargo was loaded on 12 November, and any barrels arriving after 20 November are being diverted to the Domestic Tariff Area rather than entering the export stream. This effectively ends the use of Russian feedstock in the SEZ ahead of the 21 November wind-down deadline.

Russian-linked shipments face a higher compliance burden in insurance and banking. This raises the operational risk profile for all importers, not just Reliance, and contributes to expectations that Russian inflows will ease from December onward.

Indian Oil Corporation (IOC) has successfully procured approximately five December-arrival Russian crude cargoes from suppliers not subject to sanctions. While this confirms that Russian crude flows continue, the secured volume, around 3.5 million barrels of ESPO-grade, is small compared to IOC's previous intake before sanctions. IOC's policy is to buy Russian crude only if the associated sellers and shipping lines are not sanctioned. This emphasizes that the continuity of future inflows is wholly dependent on finding compliant, non-designated counterparties, rather than being driven solely by underlying demand or pricing.

In the AG, even as supply increased from ~76 in early September to over 100, rates remained elevated. TD3 was already near WS 98 in mid-September and continues to display firmness into late November.

WAFR | Last 12M Avg: 13 Vessels

In WAF, TD15 has surged as net supply dropped to multi-month lows, with rates holding firm around WS 120 even as availability began to pick up in late November.

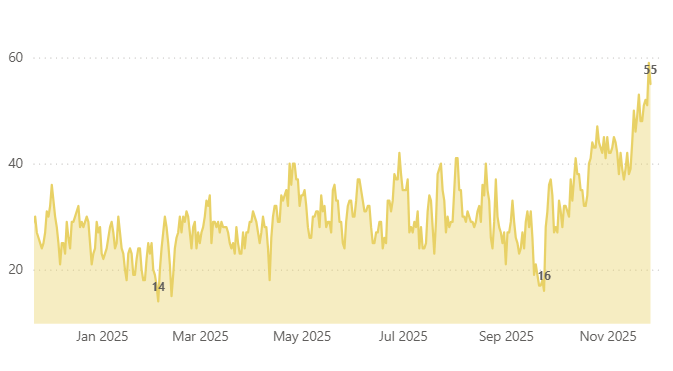

Discharge congestion in China has climbed sharply from early-autumn lows to the highest levels of the year, tightening effective tonnage supply and adding to the firmer sentiment on long-haul crude routes.

Macro Elements

Oil price projections | JPMorgan recently warned that a structural oversupply in the oil market could cause prices to fall sharply by 2027. In their base-case scenario, Brent crude is projected to be around $57 per barrel in 2027. However, under their downside scenario, if oversupply persists and producers fail to cut output, Brent prices could fall into the $30s per barrel by the end of 2027.

Some Indian banks are cautiously exploring financing of Russian-origin oil trades, provided the Russian counterparties and shipping/insurance lines are not under U.S. or EU sanctions. This reflects a narrow path to re-enter Russian crude supply without violating sanction regimes.The proposed mechanism involves complex compliance: payments routed through alternative currencies (e.g., UAE dirham, Chinese yuan) and rigorous vetting of counterparties to ensure no sanctioned entity is involved.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)