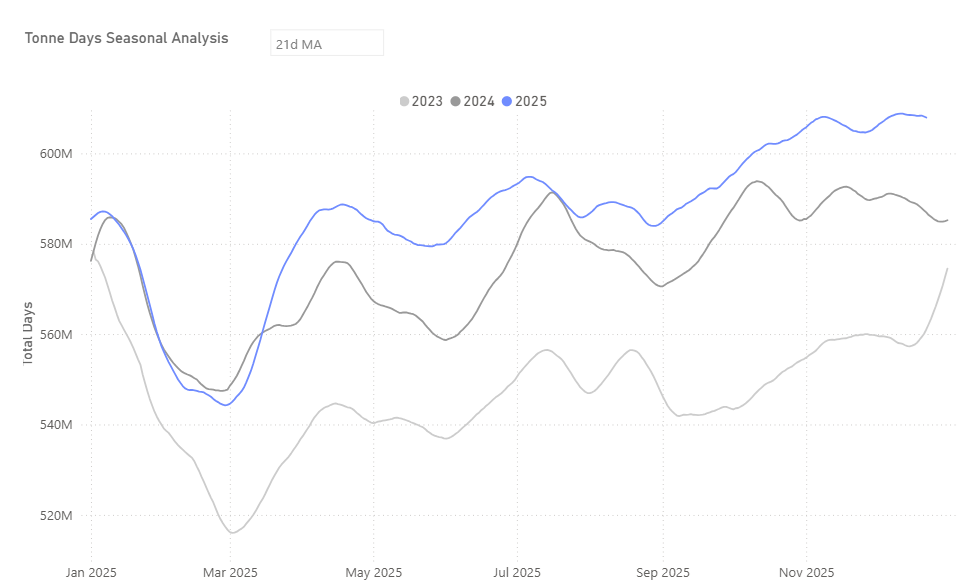

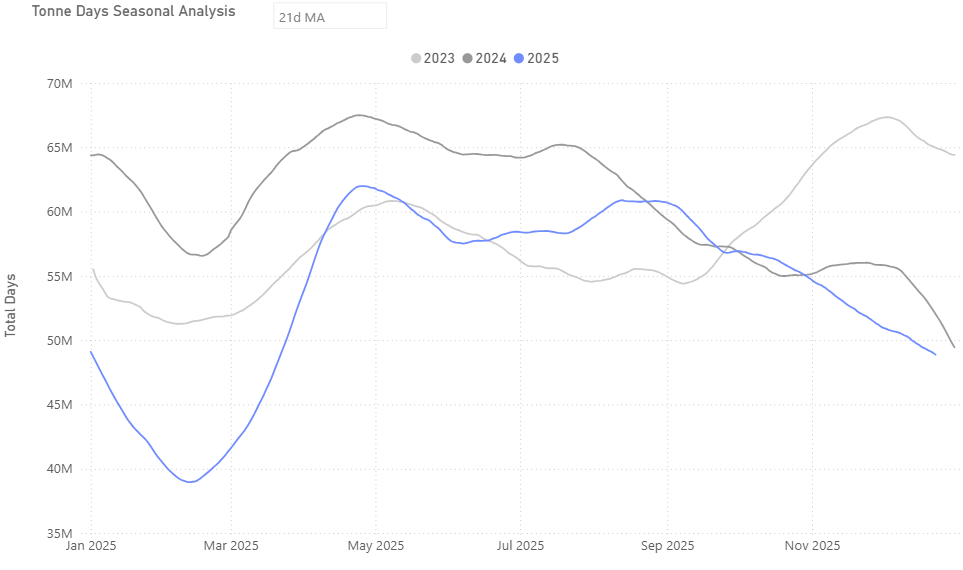

Dry bulk tonne-days reached record highs in 2025, exceeding previous historical peaks, up around 4% year on year and close to 9% compared with 2023, highlighting the role of distance-driven demand in supporting vessel utilisation.

The increase in tonne-days has been driven primarily by iron ore trade, reflecting the impact of long-haul Atlantic basin exports on Capesize demand.

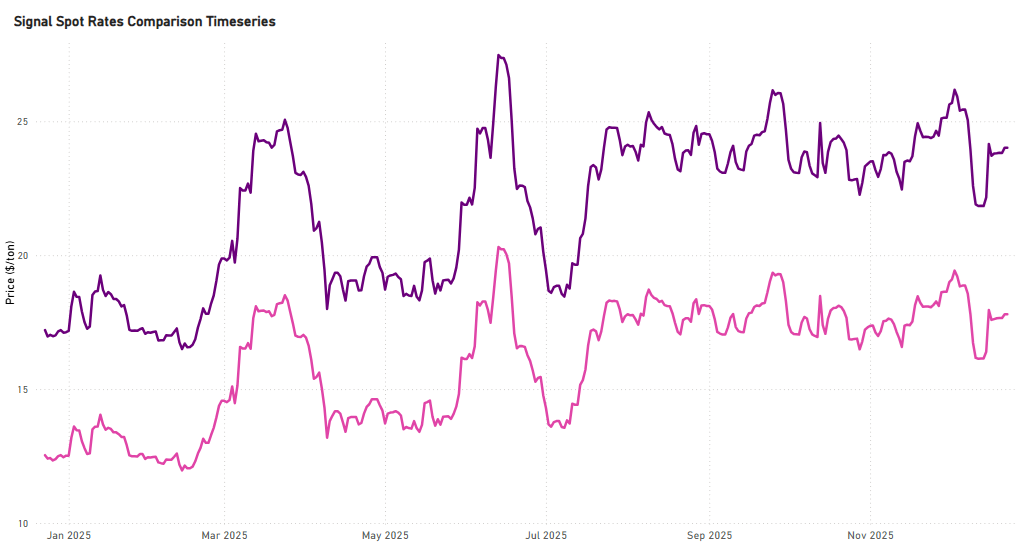

Freight market trends ahead of the Christmas period indicate strengthening momentum on Brazil–China and South Africa–China Capesize routes, pointing to a firmer tone into year-end. Although Brazil–China Capesize rates peaked on 3 December at nearly $26/ton, the subsequent pullback has been contained, with current levels holding at about $24/ton rather than signaling a broader deterioration, supported by ongoing long-haul cargo demand.

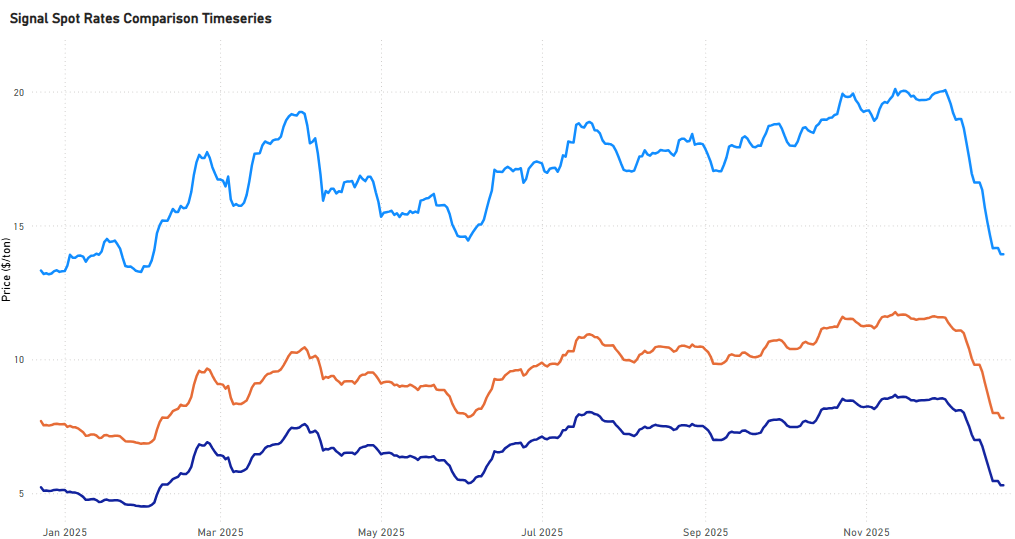

FREIGHT | Capesize | Atlantic Firmer

Iron Ore: Core Contributor to Tonne-Day Growth

Iron ore has remained the dominant driver of the recent recovery in dry bulk tonne-days, with Chinese import demand continuing to underpin Capesize utilisation despite weak macroeconomic signals and subdued downstream steel sentiment. Growth in iron ore–related tonne-days is estimated at approximately 199 million, accounting for a significant share of the overall expansion and underscoring the continued importance of long-haul iron ore trades relative to other dry bulk commodities.

At the same time, bauxite has emerged as an increasingly important contributor to tonne-day growth, particularly within the Capesize segment. Longer-haul sourcing patterns and rising Chinese alumina demand have elevated bauxite’s role in fleet utilisation, a dynamic examined in greater detail in our latest Commodity Radar, with a dedicated focus on bauxite’s growing contribution to current demand growth. Looking ahead, iron ore tonne-day fundamentals remain supported into the remainder of the quarter, although early Q1 is expected to see a temporary moderation around the Chinese New Year period. However, such slowdowns have historically been short-lived, with a post-holiday rebound as supply chains normalise and deferred cargoes re-enter the system.

By contrast, tonne-day growth in coal and agricultural trades has been revised lower toward year-end compared with the previous two years, underscoring the growing reliance on iron ore and bauxite for demand support.

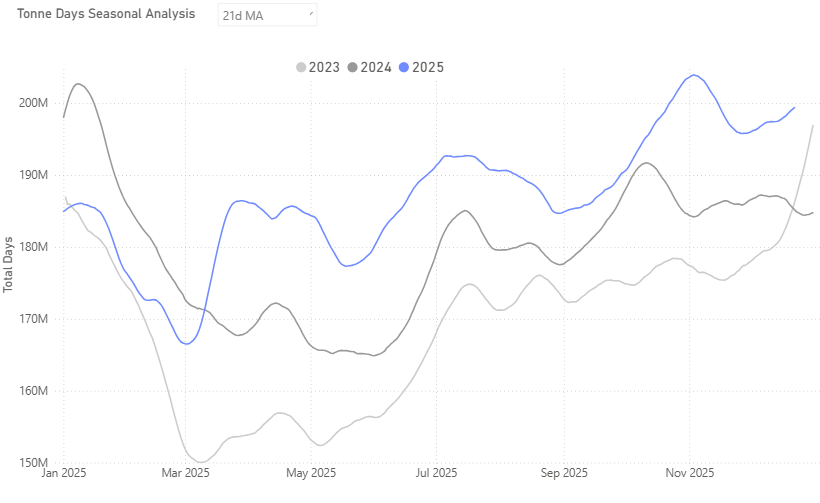

Coal: Seasonal Rebound, Revised Annual Growth

By year-end, downward revisions were observed in full-year tonne-day growth for coal to the Far East, reflecting weaker performance earlier in the year.

However, a clear rebound emerged in the fourth quarter, with coal tonne-days reaching around 90 million following a pronounced decline at the end of the summer season. This recovery aligns with the typical winter seasonal upturn, although the magnitude remains lower compared with previous years, suggesting a more moderate seasonal effect on freight demand rather than a significant shift.

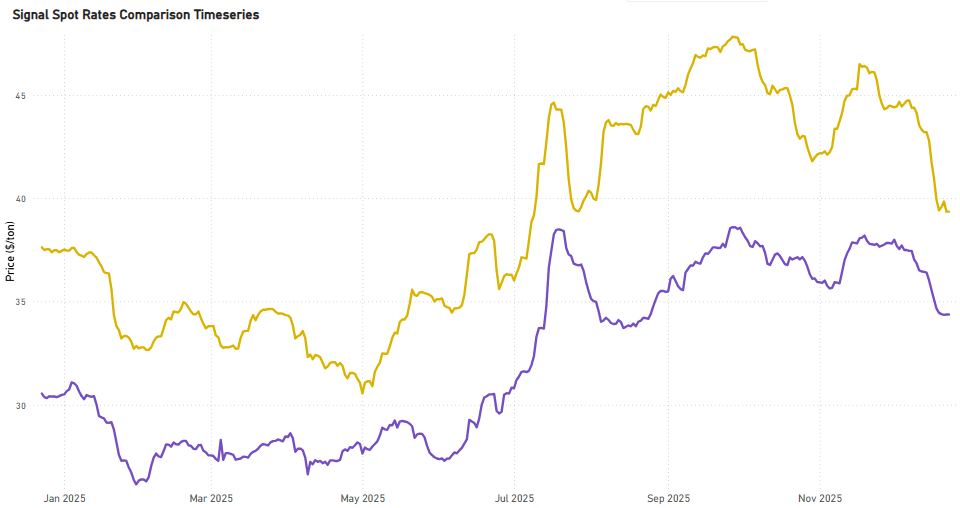

FREIGHT | Panamax | Pacific Weaker

Freight markets are set to close the final quarter of the year with a pronounced downward momentum across key Panamax routes. On a quarter-on-quarter basis, Indonesia–China rates have fallen by 37.5%, Indonesia–India by 32.1%, East Australia–China by 29.3%, and US Gulf–China by 15.8%. These steep QoQ declines confirm that the monthly correction observed earlier in the year has evolved into a deeper momentum downturn. As a result, the market is likely to enter the start of the new year from a weaker base, increasing the risk that Q1 freight levels remain under pressure in the absence of a meaningful supply-side tightening.

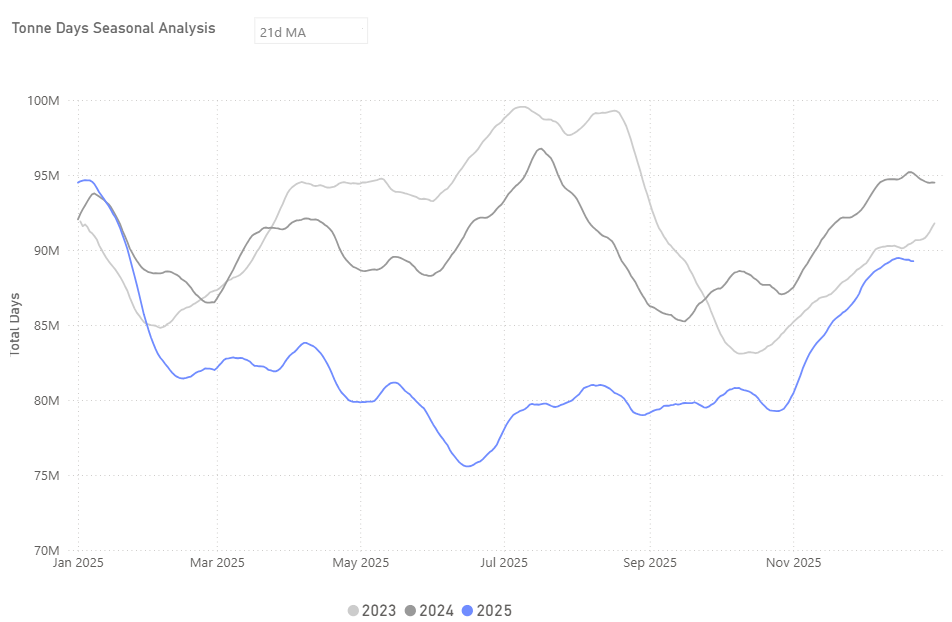

Agricultural Trades: Continued Downward Trend

Agricultural tonne-days continued to trend lower, contributing to the overall downward revisions observed toward year-end.

From a freight standpoint, long-haul demand is moderating as China’s agri self-sufficiency strategy caps incremental import growth and vessel-day generation, with prevailing industry estimates suggesting approximately 1 million tonnes year-on-year reduction in soybean imports for the 2025–26 crop year, despite stable meal feed demand.

Supramax Atlantic routes are closing the final quarter under sustained downward pressure. On a quarter-on-quarter basis, US Gulf–Far East rates are down 14.6%, while US Gulf–Skaw/Pass has declined by 14.9%. ECSA–Far East has also weakened, posting an 8.9% QoQ contraction, though the magnitude of the decline remains smaller relative to US Gulf–origin routes. As a result, the Supramax market enters the start of the new year from a weaker Atlantic-driven base, limiting upside at the beginning of Q1.

FREIGHT | Supramax | Atlantic Weaker

Takeaways and Upcoming Trends

Overall, the year concludes with tonne-day demand driven primarily by iron ore flows into the Far East, while coal and agricultural trades make a more moderate contribution.

In the coal segment, the most notable recent development has been a shift in South African export destinations, with a clear increase in shipments to Israel observed toward year-end. At the same time, China’s coal import dynamics continue to be shaped by supplier economics, logistical considerations, and policy settings, alongside domestic production levels and power-sector requirements.

In agricultural markets, China’s ongoing emphasis on domestic self-sufficiency, together with geopolitical tensions between Russia and Ukraine, remains an important contextual factor for freight markets. Black Sea exports have continued, but under sustained operational and commercial uncertainty, including elevated risk perceptions and higher insurance and compliance costs.

Looking ahead, freight market performance in the coming year is expected to remain strongly influenced by geopolitical risks, Chinese policy direction, and broader macroeconomic developments. These factors will shape both cargo demand and vessel supply dynamics, with current signals pointing toward continued momentum in the Capesize freight market.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)