Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

COMMODITY RADAR | Spotlight: BAUXITE

Bauxite helps to hold the capesize market

A 22% increase YTD in bauxite exports from Guinea has helped to stabilise the capesize market as coal has waned.

Bauxite flows in 2025 sit above 2024 by 18%.

China has driven all the increased demand, with imports rising by 22%.

Elsewhere, imports have remained flat y/y in 2025.

Overall, bauxite export tonnage will face challenges in 2026, as China aims to keep aluminium production capped at 45mt, a figure it is likely to hit in 2025.

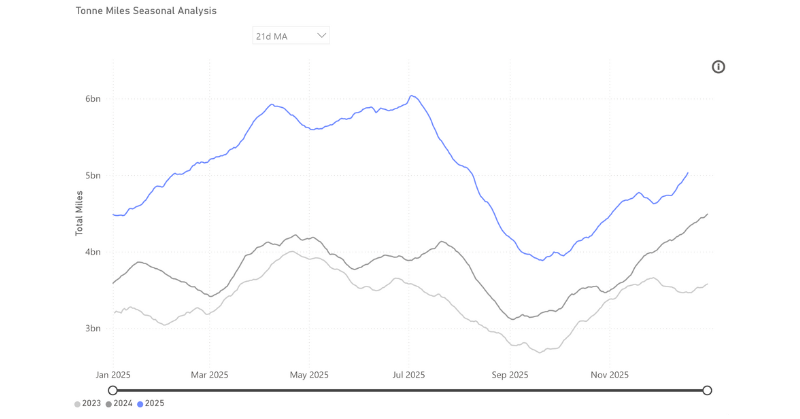

Source: Bauxite carrying Capesize tonne-miles to China from Signal Ocean

Bauxite exports from Guinea have experienced uninterrupted y/y growth every month so far in 2025, with the final month of December likely to be no different. As a result, bauxite exports from Guinea are likely to reach 175mt, 22% higher than in 2024. This has led to bauxite being the best-performing capesize commodity behind iron ore on a tonne-mile basis.

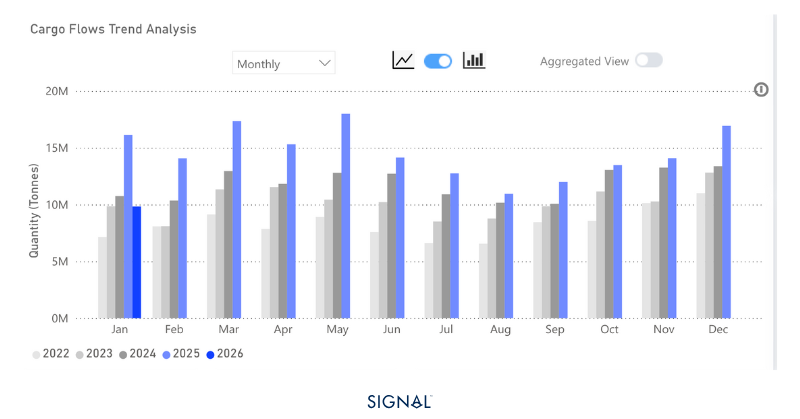

Guinea is the largest bauxite exporter, accounting for 69% of all bauxite exports in 2025. This is way ahead of second-placed Australia, which accounts for 18%. The countries are much closer in terms of bauxite production, 130mt vs 100mt, but Australia processes bauxite domestically into alumina, whereas Guinea does not have the capacity to do so. Guinea, therefore, needs to export bauxite.

Source: Guinea bauxite exports from Signal Ocean

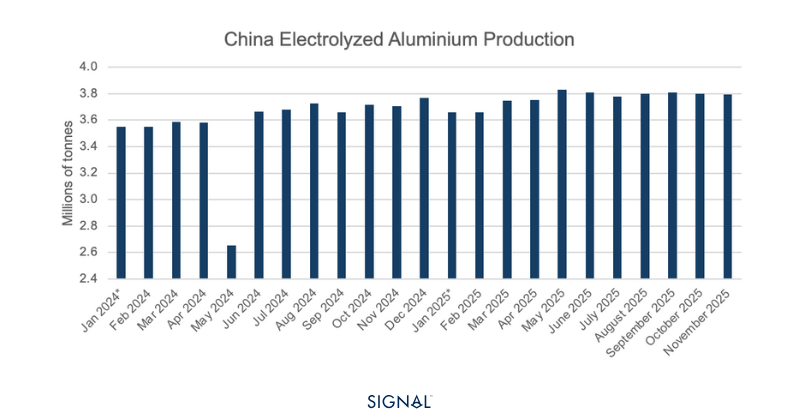

China consumed 86% of all bauxite exports in 2025 to feed its aluminium industry. In China, aluminium production has a self-imposed cap of 45mt tonnes per annum, introduced in 2017 to curb emissions and help prevent oversupply. According to China’s National Bureau of Statistics, Chinese aluminium production for the first 11 months of 2025 sits at 41.4mt, meaning December production can be no more than 3.6mt to be within the cap. This figure is much lower than the 3.8mt monthly average 2025 has produced.

Given the cap restarts in January, the outlook for bauxite demand in China remains strong in the short term. Adding to this, the strong performance of copper prices has helped to increase demand for aluminium as a substitute. The outlook for copper prices is that they will soften somewhat from the current levels in 2026 but remain relatively high. This will be positive for aluminium demand and pull all the way through to bauxite demand. China could look to import greater volumes of bauxite, process them into alumina, and then export that to places like Indonesia, where aluminium smelting capacity is growing.

Source: China aluminium production from the National Bureau of Statistics

Looking further ahead to 2030, bauxite exports raise more intriguing questions. Guinea plans to achieve roughly 7mtof alumina production annually by that year, which would require about 14mt of bauxite. Based on 2025 export levels, this could reduce global bauxite exports by around 5%. While this initial decline is modest, additional alumina capacity could be brought online rapidly if government revenues increase as expected from higher-value alumina exports. Over time, this may drive a steady and prolonged contraction in Guinea’s bauxite exports.

Weaker bauxite exports would compound the expectations of weaker coal exports and weigh heavily on capesize freight markets.

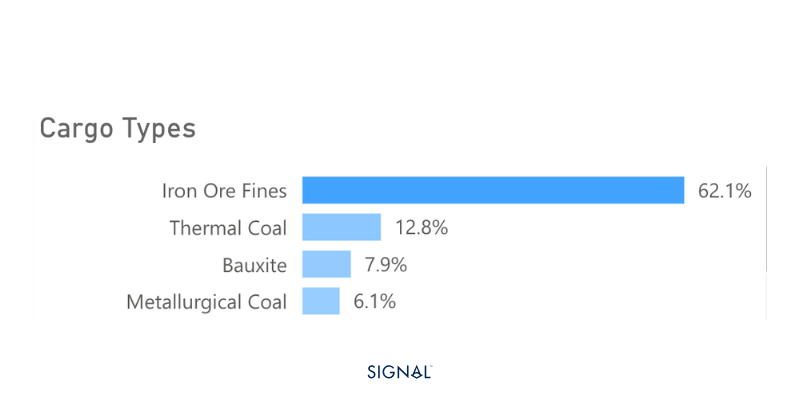

Source: Capesize demand by commodity.

Bauxite will continue to drive capesize …

Chinese aluminium production will continue to drive demand for bauxite, with the domestic production cap providing a soft ceiling. The supply of bauxite will remain consistent from the largest producer, Guinea, but the longer-term risks of more being processed domestically will be something the market needs to be ready for in the next few years.

As a result, we do expect bauxite to persist as a strong driver for capesize demand. The first quarter of the year is often weaker for bauxite exports, but given the trends, 2026 Q1 is expected to be above the same period in 2025, before ramping up in Q2, which tends to be the better-performing quarter.

Luke has over 8-years of experience analysing and forecasting commodity markets, with particular expertise in stainless steel raw materials and the wider metals markets.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)