Australia, Brazil, and West Africa Lead the Charge

In the Pilbara, BHP is doubling down on growth, pledging A$1.4 billion to enhance Port Hedland infrastructure and sustain export capacity near 305 million tonnes per annum (Mtpa). The investment signals confidence in steady, high-volume output from Western Australian miners through 2026.

Brazil’s Vale posted 94.4 Mt in Q3 2025, its strongest quarterly output since 2018, keeping it on track for the top end of its 325–335 Mt guidance. Stronger performance from the Northern System and better weather lifted loadings from Ponta da Madeira and Tubarao, cementing Brazil’s role in the Atlantic-to-Asia trade.

Simandou Nears Launch, Redefining Atlantic–Pacific Iron Ore Trade Routes

In West Africa, momentum is finally building. Simandou in Guinea is moving from construction to early stockpiling, with first shipments expected in late 2025. The long-awaited, high-grade project could redefine trade patterns, positioning West Africa as a new long-haul supplier to China.

Tonne-Mile Growth Fuels Capesize Rally as Long-Haul Flows Expand

For the freight market, the implications are clear. The recent increase in iron ore supply from major export hubs such as Australia, Brazil, and emerging West African origins is already visible through a sharp rise in tonne-days, up by roughly 25–30% since early 2025. This surge reflects stronger long-haul activity and greater tonnage absorption, supporting improved Capesize rate performance and a sustained recovery in the BCI. Continued expansion of these export flows, particularly from projects like Simandou, is expected to further boost tonne-mile demand and gradually rebalance Atlantic–Pacific trade dynamics.

Chinese Steel Slowdown Offsets Supply Gains - Port Stocks on the Rise

However, the recent renewed supply optimism contrasts sharply with China’s weakening macroeconomic outlook. The world’s largest iron ore importer continues to struggle with a sluggish property sector and compressed steel margins, both of which are limiting restocking appetite.

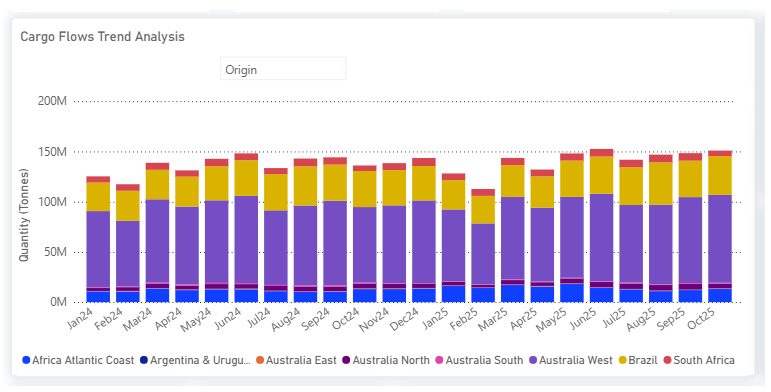

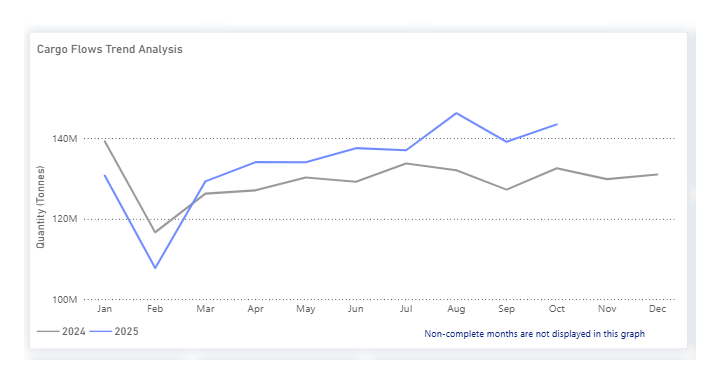

As illustrated in the chart, iron ore shipments to China have grown markedly in 2025, with monthly arrivals consistently exceeding 2024 levels since March. Volumes climbed from around 115 million tonnes in February to more than 140 million tonnes by October, reflecting stronger export flows from Australia and Brazil.

Yet this growth in seaborne supply is occurring at a time of soft domestic steel demand and seasonal production slowdowns. Rising port inventories, together with a lack of meaningful policy stimulus from Beijing, have therefore kept spot prices under downward pressure. As winter maintenance cuts steel output, the continued inflow of cargoes risks widening the imbalance between supply and consumption, reinforcing the bearish tone in the iron ore market.

China Eyes Yuan-Based Iron Ore Pricing

Adding another layer of complexity, discussions are resurfacing about pricing iron ore in yuan rather than U.S. dollars. Such a shift, if it gains traction, would mark a significant geopolitical move, aligning with China’s broader strategy to internationalize its currency and reduce exposure to dollar-denominated commodities. While symbolic for now, yuan-based pricing could eventually alter how iron ore trade and financing are conducted, with potential implications for hedging and contract benchmarks.

In short, the iron ore market is preparing for an influx of supply just as China’s demand signals weaken and currency politics enter the pricing equation. For Capesize owners, this combination could mean greater volatility, but also new opportunities as trade routes diversify and tonne-miles expand.

To read more articles like these subscribe here or email us at research@thesignalgroup.com. For demo inquiries, reach out to us and visit the Signal Ocean Newsroom for the latest updates on market trends and platform developments. To check out our previous newsroom article click here.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)