Structural Market Shifts, Not Just Barrels, Powering the Dirty Rally

Structural friction, not soaring demand, is fuelling today’s crude freight rally.

drives these stories

Structural Market Shifts, Not Just Barrels, Powering the Dirty Rally

Crude freight markets are experiencing a surge, which available data suggests is not solely attributable to extended voyages or an oversupply of crude. Elevated tonne-days versus lower tonne-miles reveal a market constrained by structural inefficiencies, including vessel rerouting, compliance delays, and sanction-related reshuffling, which have tightened fleet availability across the dirty segment.

In This Article

- Freight Rates Surge as Inefficiencies Mount

- The Hidden Driver: Tonne-Days Remain Elevated

- The Oil Glut Narrative

- Recent Individual Vessel Behaviour Further Illustrates Market Distortion

- Load Trends Reflect Timing Slips, Not a Major Supply Surge

- Speed as a Signal of Market Inefficiency

- Frequently Asked Questions

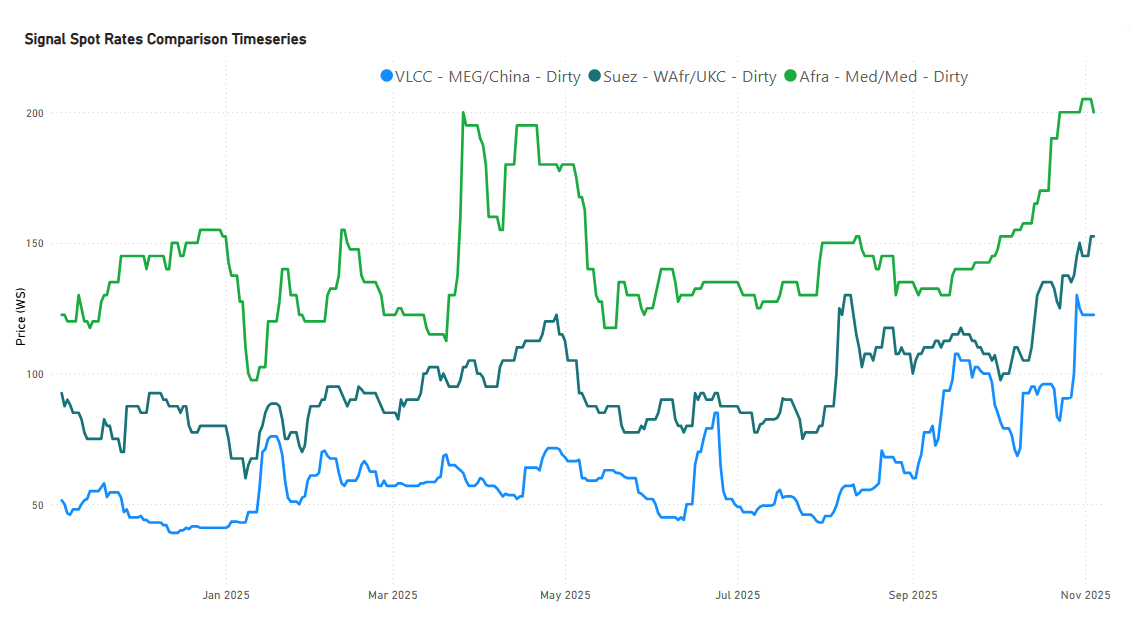

Freight Rates Surge as Inefficiencies Mount

https://app.signalocean.com/tanker/dynamic/market-prices-tankers

https://app.signalocean.com/tanker/dynamic/market-prices-tankers

Crude freight markets are experiencing another surge, with spot rates for VLCC AG–China, Suezmax WAFR–Continent, andAframax Mediterranean routes all climbing to multi-month highs. As of 6 November 2025, VLCC AG–China stands around WS107 (up +114% y/y), Suezmax WAFR–Continent near WS160 (up +76% y/y), and Aframax Med at roughly WS198 (up +66% y/y), while the Baltic Dirty Tanker Index (BDTI) has reached 1,403, marking a +49% y/y gain. While this might initially suggest a surge in tonne-mile demand from longer-haul trades, Signal Ocean data tells a more complex story.

Tonne-miles in 2025 have averaged around 40–41 billion, staying consistently below early-2024 levels of roughly 42–43 billion. The 2025 trend curves lower throughout most of the year, only narrowing the gap in late Q3.

https://app.signalocean.com/tanker/dynamic/timeseries_tanker

https://app.signalocean.com/tanker/dynamic/timeseries_tanker

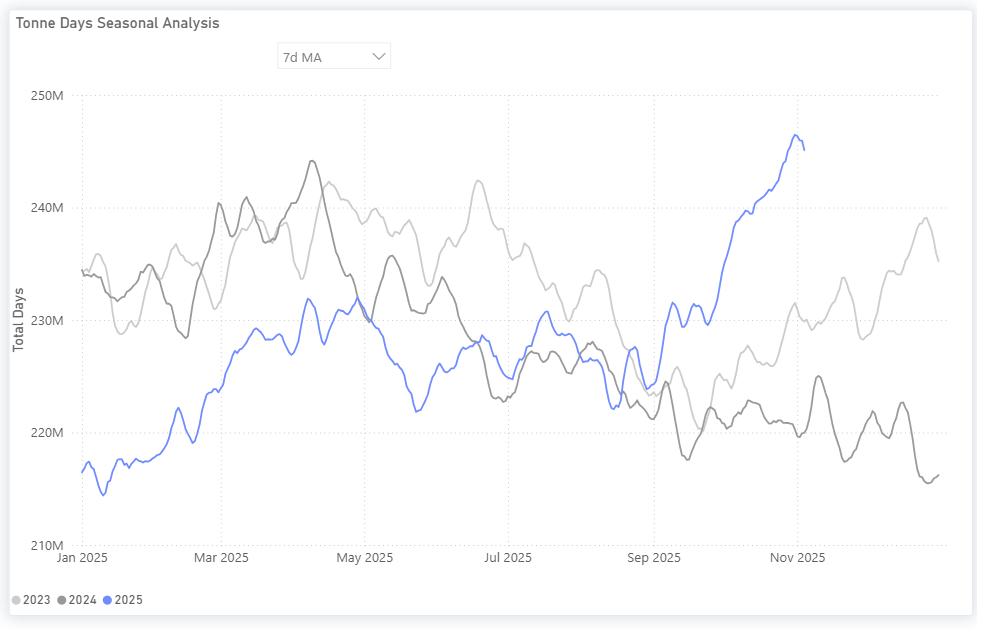

The Hidden Driver: Tonne-Days Remain Elevated

Tonne-days have risen to about 250 million by Q4, hitting multi-year peaks from the lows of below 220 million in early 2025. This indicates not shorter trade distances, but slower fleet circulation and increasing inefficiencies. Oil still reaches its destination; it just takes longer to arrive.

Operational hurdles are causing a slowdown due to sanctions, port fees, and compliance issues that have disrupted voyage routes and vessel deployment. Ships are experiencing longer clearance times, not necessarily from physical port delays, but from strategic repositioning to avoid expensive terminals and reassign vessels for ship-to-ship operations.

Each voyage now faces a greater administrative load, including sanction checks, insurance verifications, and document compliance, all of which add extra days at sea. Overall, this results in inflated tonne-days and an artificially tight freight market — a dynamic Signal Ocean tracks in real time across the full dirty fleet.

https://app.signalocean.com/tanker/dynamic/timeseries_tanker

https://app.signalocean.com/tanker/dynamic/timeseries_tanker

The Oil Glut Narrative

At first glance, the market appears to be facing an emerging oil surplus. Floating storage among non-sanctioned dirty tankers has risen to just over 70 million barrels as of late October, surpassing recent seasonal norms and inviting comparisons with earlier periods of oversupply. Yet, the current buildup may indicate more of a logistical pause than a genuine excess of crude.

https://app.signalocean.com/tanker/dynamic/floating_storage

https://app.signalocean.com/tanker/dynamic/floating_storage

Part of the recent increase seems linked to longer discharge intervals and uneven cargo scheduling, as trade flows adjust to shifting freight economics and evolving compliance frameworks. Some vessels are remaining on the water longer than usual, not necessarily because of weak demand but as a by-product of operational reshuffling across routes and terminals. These barrels are perceived as "stored" by the market, yet they are, in fact, merely awaiting clearance or redirection.

Compared with past supply-driven gluts, today’s conditions appear more transitional than structural. The rise in floating storage seems to reflect temporary friction in seaborne logistics rather than a breakdown in underlying balances. Even with the recent uptick, volumes remain well below the 150 million barrels recorded in late June and far beneath the pandemic highs of 2020.

Should thesanctioned fleet be included, the picture becomes more complex. Floating storage among sanctioned vessels has recently climbed above 30 million barrels, marking one of the highest levels since mid-2022. This rise may reflect growing challenges in clearing sanctioned oil, either because cargoes face delays in obtaining discharge approvals, vessels become sanctioned mid-voyage and are subsequently rejected, or buyers quietly adjust their procurement policies to mitigate compliance risk. Collectively, these dynamics suggest that geopolitical segmentation and shifting regulatory behavior now appear to play a larger role in determining how and where oil is held, subtly influencing perceptions of available supply.

https://app.signalocean.com/tanker/dynamic/floating_storage

https://app.signalocean.com/tanker/dynamic/floating_storage

Recent Individual Vessel Behaviour Further Illustrates Market Distortion

Recent voyage behaviour in the dirty tanker segment has highlighted cases of mid-route reversals and destination changes, illustrating how market uncertainty can affect fleet efficiency. In two notable instances, tankers initially appeared bound for U.S. discharge zones before altering course toward European destinations, while another shifted direction via the Mediterranean before continuing west.

These shifts may reflect a mix of revised trading programs, buyer policy adjustments, or compliance reviews introduced late in the voyage. In certain instances, vessels have remained in waiting positions for extended periods before receiving new discharge instructions, suggesting clearance complications or shifting commercial priorities rather than simple port congestion. Each change adds time-on-water and limits effective fleet rotation, tightening the supply of available tonnage in the spot market.

Load Trends Reflect Timing Slips, Not a Major Supply Surge

Voyage data indicates a slight increase in dirty cargo shipments in October, with approximately 1,450 recorded. This represents a 4.9% month-on-month rise and an 8.0% year-on-year increase. While this suggests a modest uptick in export activity, it's important to note that this increase occurred before the November announcement of OPEC+'s 137,000 b/d output adjustment for December, and therefore cannot be attributed to the new quotas.

https://app.signalocean.com/tanker/dynamic/voyages-dashboard-tankers

https://app.signalocean.com/tanker/dynamic/voyages-dashboard-tankers

Looking ahead, 2026 is expected to mark the peak of the current supply expansion cycle. Goldman Sachs projects global oil production to grow by around 4% year-on-year in Q4 2025, driven by core OPEC+ producers and non-OPEC growth in Brazil and Guyana. Described as “the last jump” before moderation from 2027 onward, this phase could temporarily pressure prices lower. Goldman’s Brent forecast for 2026 sits near US$56 per barrel.

Despite this, voyage data continue to imply that barrels are moving more slowly through the system, with delayed cargo programs and extended transit times still visible. The overall picture remains one of timing mismatches rather than genuine oversupply, where nominal production gains have yet to manifest as sustained seaborne flows.

When filtering by sanctioned vessels, grouped by discharge data, results exhibit remarkable discharge bottlenecks, particularly into the Far East, led by China. The recent turbulence surrounding Russian crude exports to China and India has further distorted flows, particularly on the AG–China corridor, amplifying voyage times and tonnage inefficiency. As a result, the increase in oil-at-sea volumes and tonne-days is less a signal of oversupply and more a reflection of trade friction and fragmented fleet utilisation.

https://app.signalocean.com/tanker/dynamic/voyages-dashboard-tankers

https://app.signalocean.com/tanker/dynamic/voyages-dashboard-tankers

Even though the oil supply seems to have grown faster than demand in recent times (which is also depicted in the softer oil prices as well), demand remains healthy, and the forward curve is mildly backwardated, at least for now. Whether contango will follow remains to be seen.

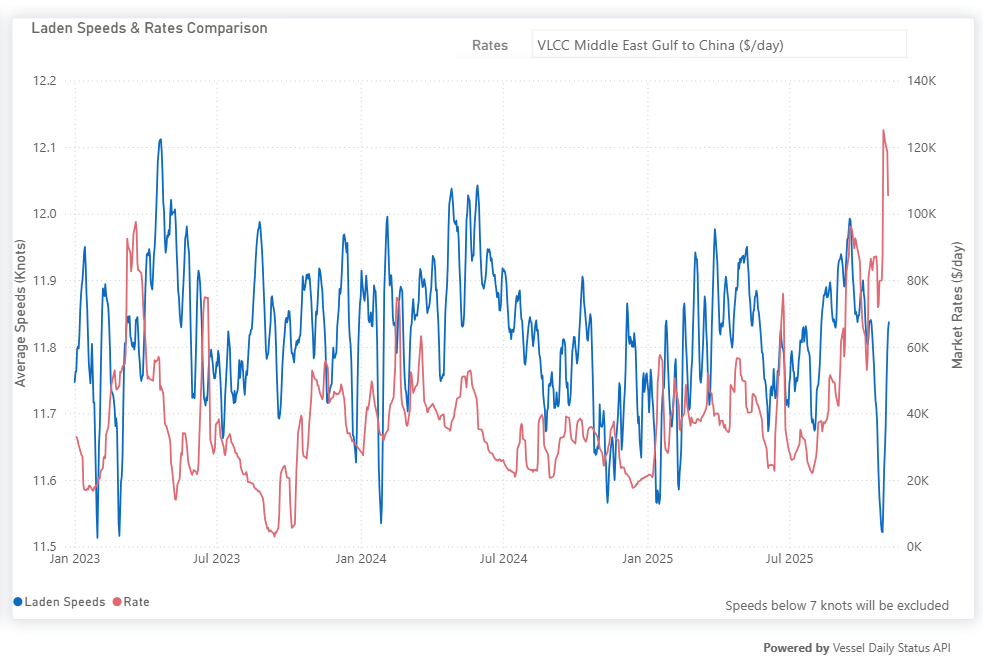

Speed as a Signal of Market Inefficiency

Recent data on VLCC, Suezmax, and Aframax speeds adds a critical dimension to understanding current market behavior. Laden speeds, particularly among VLCCs, have slowed notably, even as Time Charter Equivalent (TCE) earnings exceed $100,000 per day. Under typical market conditions, such exceptional returns would prompt shipowners to accelerate turnaround times and maximize utilization. Yet the opposite is occurring.

https://app.signalocean.com/tanker/dynamic/timeseries_tanker

https://app.signalocean.com/tanker/dynamic/timeseries_tanker

Market Outlook: Bullishness Rooted in Inefficiency

In sum, the current rally in crude spot rates is not just a story of increased demand or longer voyages; it is one of structural inefficiency, logistical inertia, and informational asymmetry. When these dissipate, it will become clearer as to what extent oil supply exceeds demand and whether significant crude oil inventories have formed by then. The task ahead is to leverage data to bridge these gaps, turning observation into understanding, and understanding into strategic advantage.

*“### Request a Demo — The Signal Group

Use real-time analytics from the Signal Ocean Platform to track laden and ballast speeds, congestion patterns, and fleet positioning — quantifying inefficiencies before they translate into rate spikes.

Ready to get started and outrun your competition?

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)