Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

COMMODITY RADAR | Spotlight: IRON ORE

How long can China continue to grow its iron ore stocks?

A 3% increase in global iron ore flows masks weak downstream demand

Iron ore flows in 2025 3% higher than in 2024.

Demand from China, up 4% y/y, and India, up 72% y/y, drove the global increase.

Elsewhere, outward steel flows were marginally lower y/y.

Outlook to 2026, weak domestic steel demand and already high port stocks in China will impact demand, but India’s steel expansions offer upside, albeit limited.

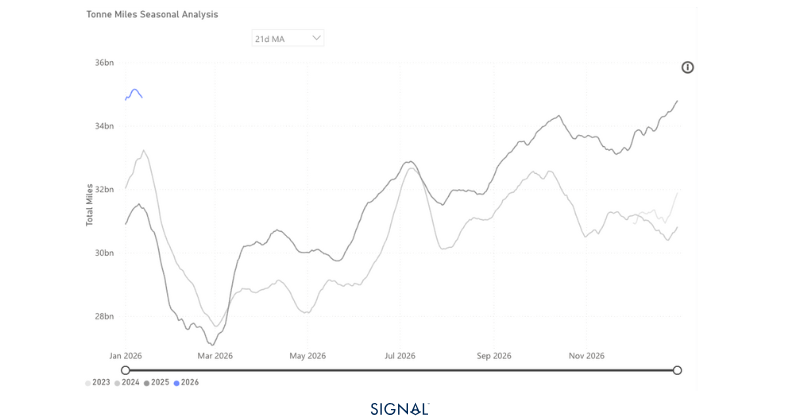

Source: Iron ore-driven tonne-miles from Signal Ocean

Global iron ore flows reached 1.7bt in 2025, 3% higher than in 2024. The growth was driven by strong growth in flows to China and extremely strong growth in flows to India. China saw an increase in iron ore flows of 3%, resulting in an extra 52mt of iron ore flowing to China. Iron ore flows into India surged by 72%, yet the absolute growth figure is just shy of 6mt.

The origin of iron ore was dominated unsurprisingly by Australia and Brazil, with annual growth from both regions. The two countries accounted for over 78% of the global seaborne iron ore on TSOP. The next largest originator for iron ore was Canada, with a share of less than 4%.

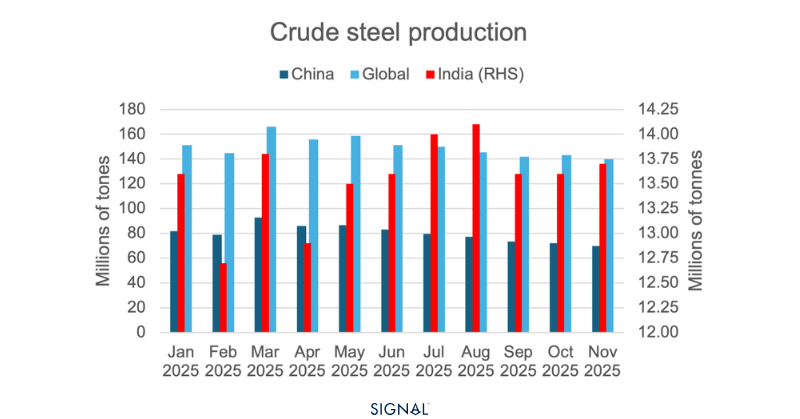

These flow figures would indicate a well-performing global steel sector, one that is seeing production increases in line with the improved flow figures. This is not the case, however. The WSA has member crude steel production for the first eleven months of 2025 down by 2%, with very few pockets of growth. Both China and Japan, the top two receivers of the most iron ore flows on TSOP, saw steel production decline by 4%.

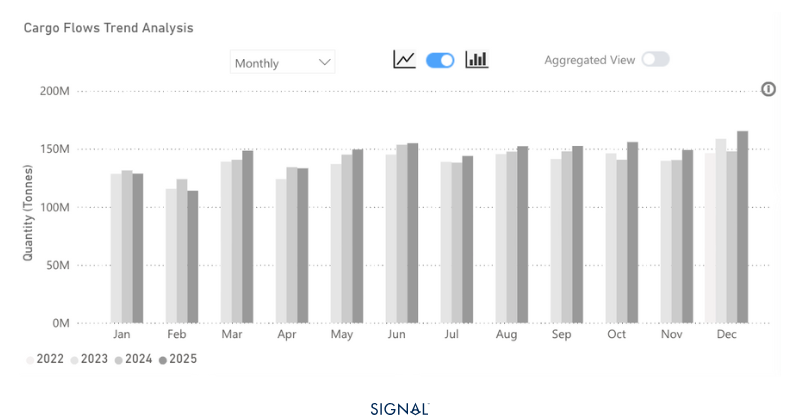

Source: Global iron ore exports from Signal Ocean

China’s steel production decline and increased imports of iron ore have led to a surge in iron ore stock levels in the country. Now, stock builds before the CNY period are not unusual but this time around, stocks have consistently building from the summer. Adding to this, downstream demand for steel has underperformed, leading to pressure on steel mills, which have cut back, and iron ore port stocks are now sitting at multi-year highs. The outlook for 2026 is that steel production in China will continue to decline, as the government looks control the over-capacity within the industry and trade barriers impact both the demand and supply side.

Indian steel production performed well, growing by over 10% in the first eleven months of 2025. This increased production drove the additional 6mt of iron ore flows into the country. The Indian steel outlook for 2026 is also incredibly positive. The government has implemented several policies to support domestic steel producers, and the nation plans to increase its steel production capacity by 50% to 300 million tonnes by 2030.

Yet, given that China consumes over 75% of the seaborne iron flows on TSOP, the overall market is heavily dependent on China, and even a stellar year for India would not significantly impact the market.

The opening and ramping up of the Simandou project in Guinea does offer a positive upside for 2026. The project will export 120mt of iron ore once at full capacity, but this isn't expected until late 2028 and is dependent on all systems and blocks being fully utilised. Rio Tinto has reported they expect the project to take 30months to reach 60mt of output, 50% of the total operational capacity. Despite this, the Guinea to China route is over double the nautical miles that iron ore from Australia travels to China. Meaning that if demand falls for iron ore, but the source of this iron ore shifts to Guinea, freight rates will be supported.

Source: Crude steel production from the World Steel Association

Shifting trade will change capesize outlook

The outlook for weaker Chinese steel production is the largest factor weighing on iron ore demand in 2026, which will ripple back through to capesize prices. The expected increase in India and elsewhere will be unable to meaningfully change this.

The upside from Simandou coming online is there, but it may take some time for impactful change. The much greater distance between Guinea and China, and the likelihood that Simandou displaces iron ore from Australia, is a net positive for capesize utilisation. It will take time to assess whether this will be enough to drag price higher y/y or whether continued weaker demand will be the heaviest factor.

Luke has over 8-years of experience analysing and forecasting commodity markets, with particular expertise in stainless steel raw materials and the wider metals markets.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)