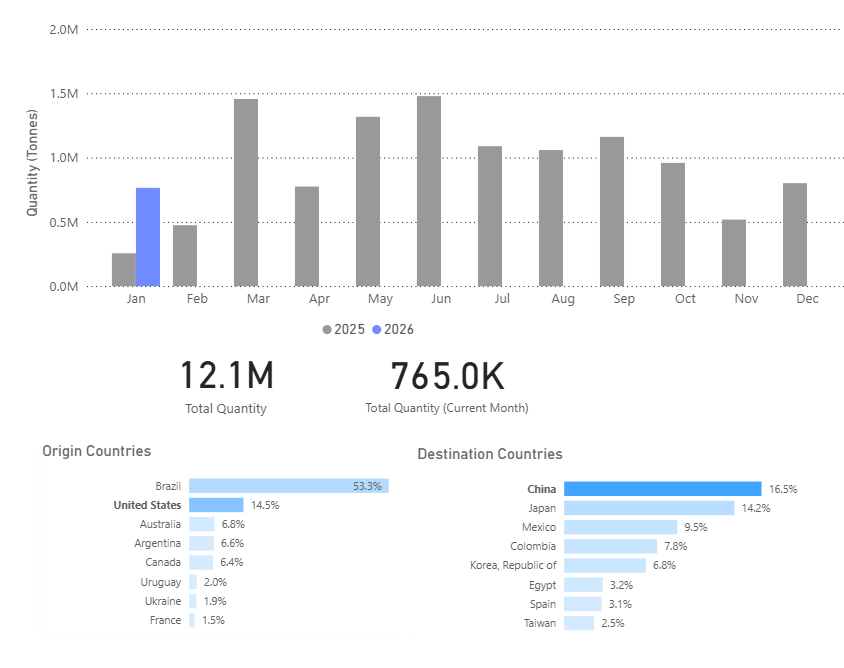

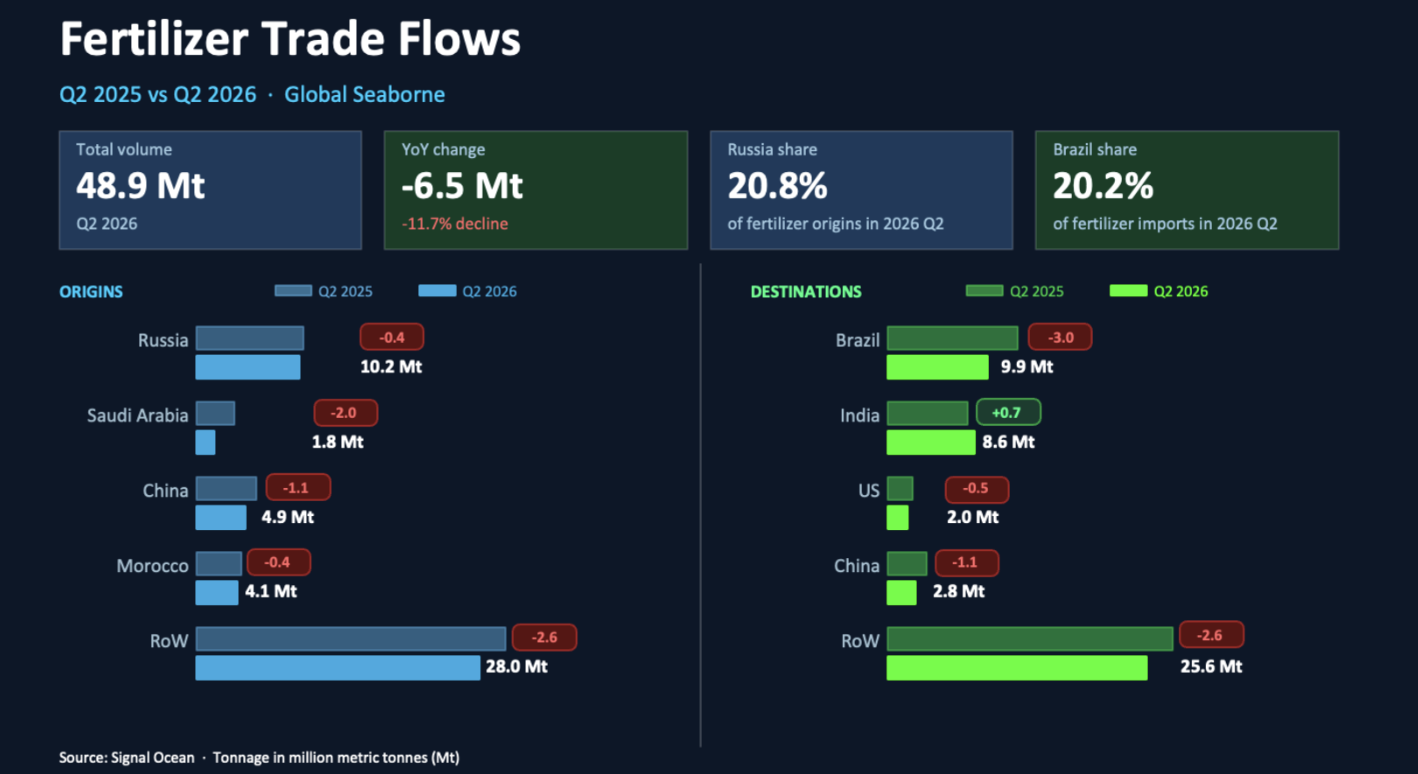

China continues to favour Brazilian and South American supplies into early 2026

U.S. soybean shipments have resumed, but flows remain episodic and seasonally concentrated rather than continuous.

Brazil enters early 2026 with expanding export availability, reinforcing its role as China’s primary supplier.

Shipment patterns indicate continuity rather than transition in China’s sourcing strategy.

China resumed imports of U.S. soybeans in 2025, with cumulative shipments estimated at approximately 12 million tonnes. These volumes were concentrated early in the year, primarily during January–February, with shipments declining thereafter and remaining limited for the rest of the year. The shipment profile does not indicate a sustained increase beyond this early-season period.

Brazil remained the primary supplier to China throughout the year. Brazilian-origin shipments accounted for more than half of cumulative China-bound volumes, reflecting consistent export availability rather than reliance on short-term shipment windows. While monthly volumes eased toward year-end, Brazil maintained a steady presence across destinations.

Brazil Supply Outlook

Brazil’s 2025/26 soybean harvest is currently projected at approximately 160–165 million tonnes, placing production near record levels and modestly above the prior year. Harvest activity typically accelerates from January, with export availability increasing into Q1 2026. This timing has supported advance sales and scheduled shipments to China ahead of peak export months.

The moderation in Brazilian shipments observed late in 2025 is consistent with typical seasonal patterns, as export volumes often ease following the main mid-year shipping window and ahead of the next harvest cycle. This timing aligns with the gradual drawdown of old-crop supplies rather than a deterioration in import demand. Import activity during this period appears consistent with advance coverage and scheduling decisions linked to expected early-2026 harvest availability, rather than short-term changes in consumption.

U.S. Shipment Pattern

Data from early January 2026 indicate a resumption of U.S.–China soybean shipments, although volumes remain below earlier peaks and lower than Brazilian loadings. Viewed alongside the 2025 shipment pattern, U.S. exports to China continue to occur primarily within defined seasonal or pricing-driven periods.

Based on shipment timing and volume distribution, there is no clear evidence of a structural change in China’s sourcing behaviour. Brazil’s production scale and export timing continue to underpin its position in China’s import mix, while U.S. shipments remain intermittent.

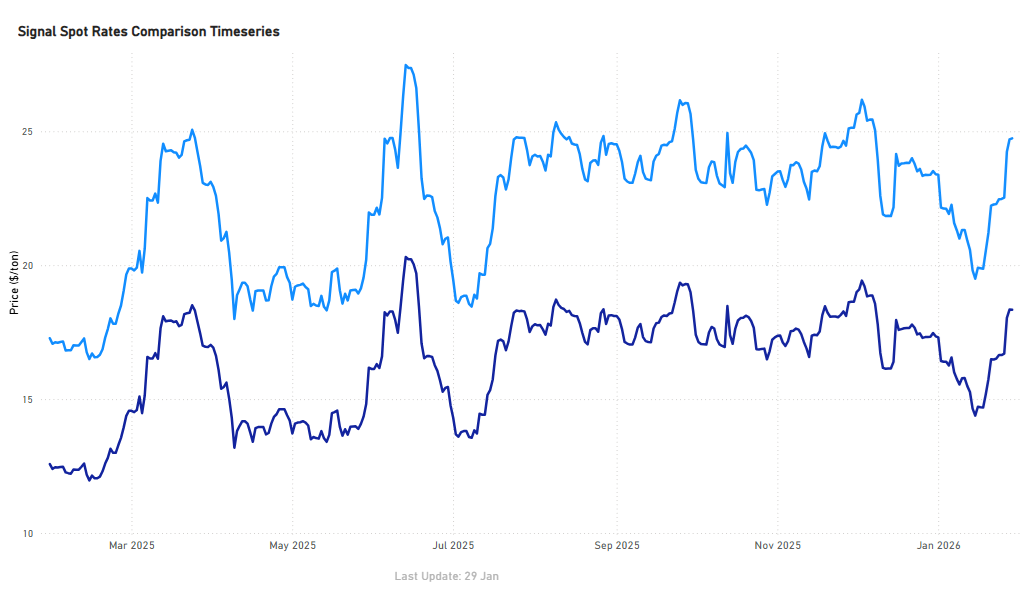

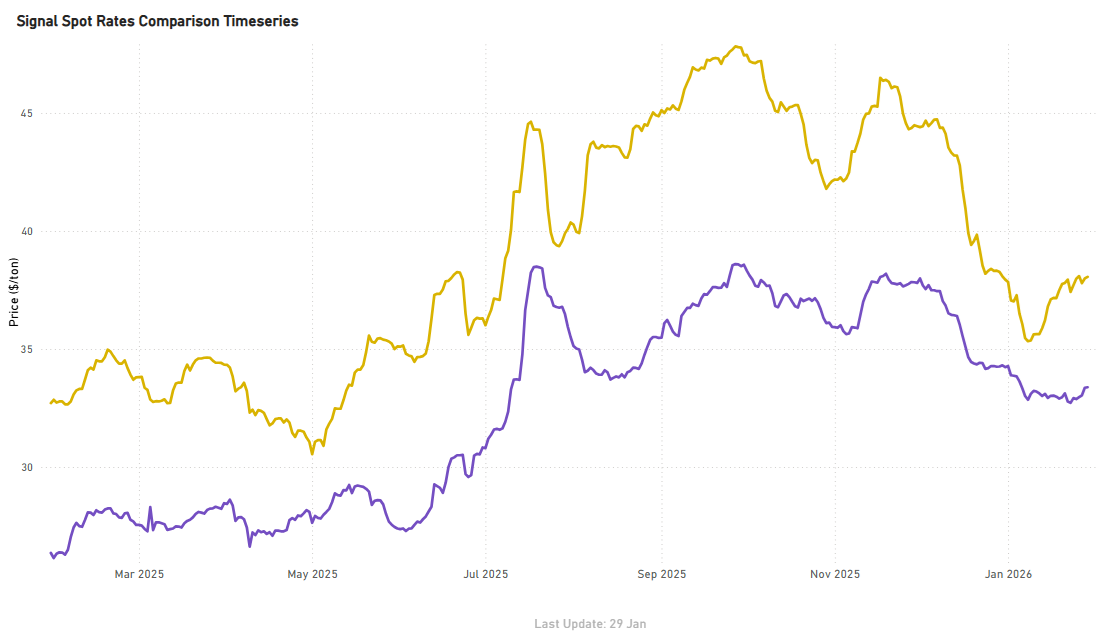

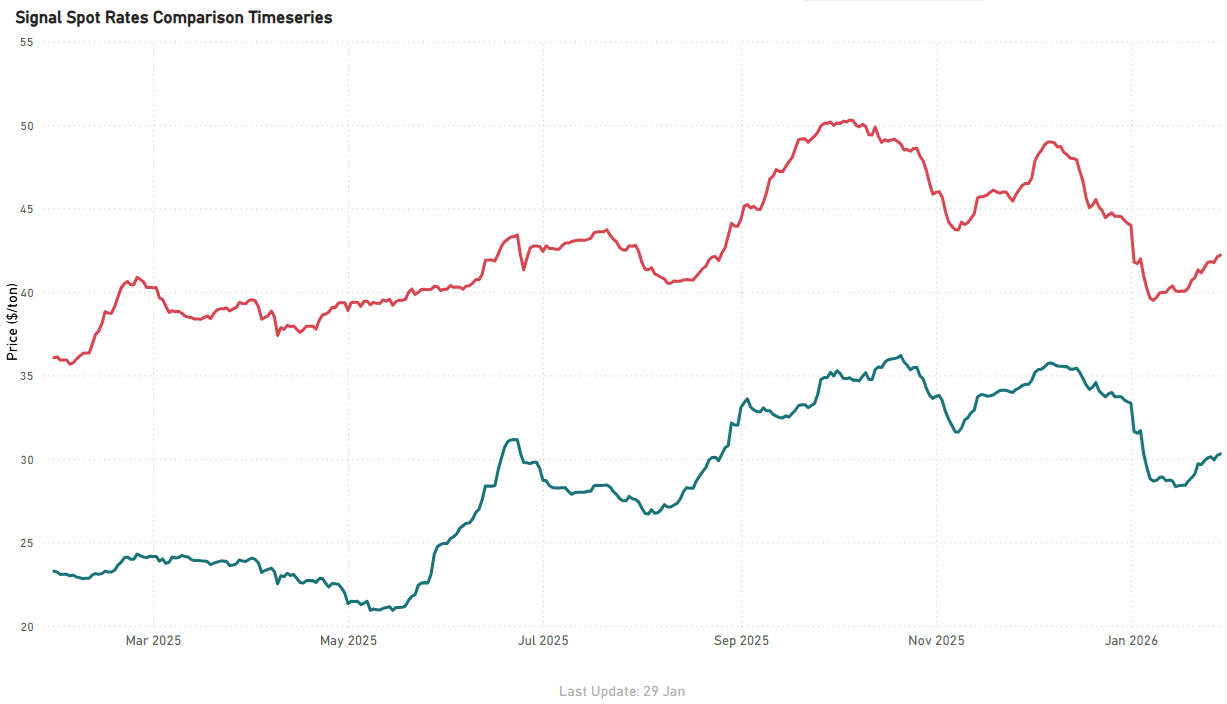

FREIGHT

Capesize | Atlantic Firmer

Atlantic Capesize routes firmed into the close of January, rebounding from mid-January lows, with Brazil–China recovering to around $24.7/tonne (≈+6–7% from mid-Jan troughs) and South Africa–China rising to about $18.3/tonne (≈+5–6%).

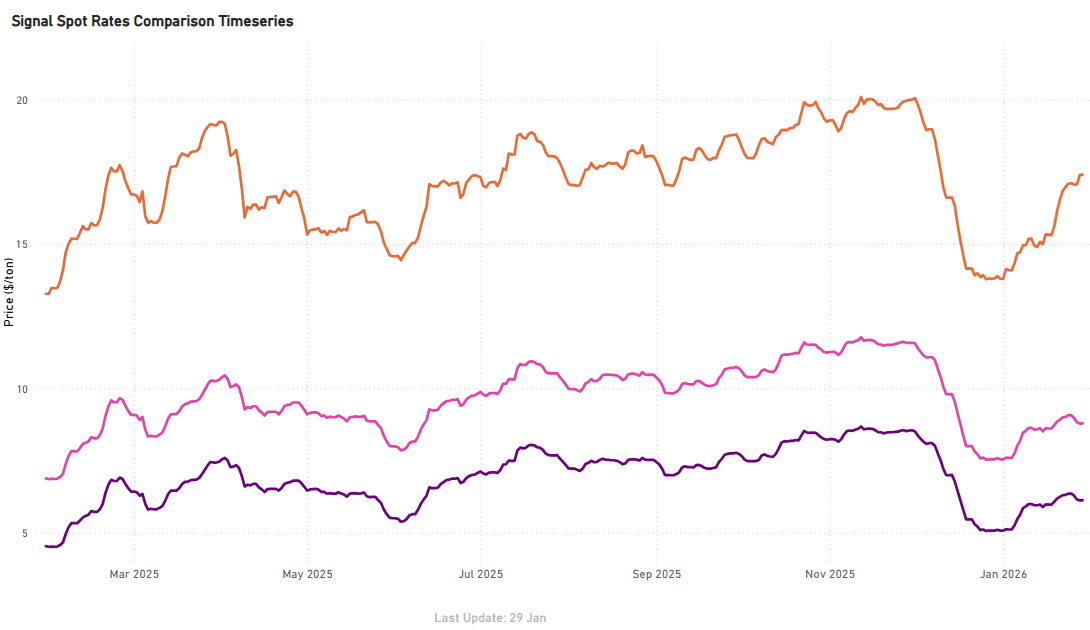

Panamax | Atlantic / Pacific Firmer

Atlantic Panamax (EAus–China) strengthened to around $17.4/tonne, up ~26% m/m, while Pacific Panamax also showed solid recovery, with Indo–China at ~$6.1/tonne (+~21% m/m) and Indo–India at ~$8.8/tonne (+~17% m/m).

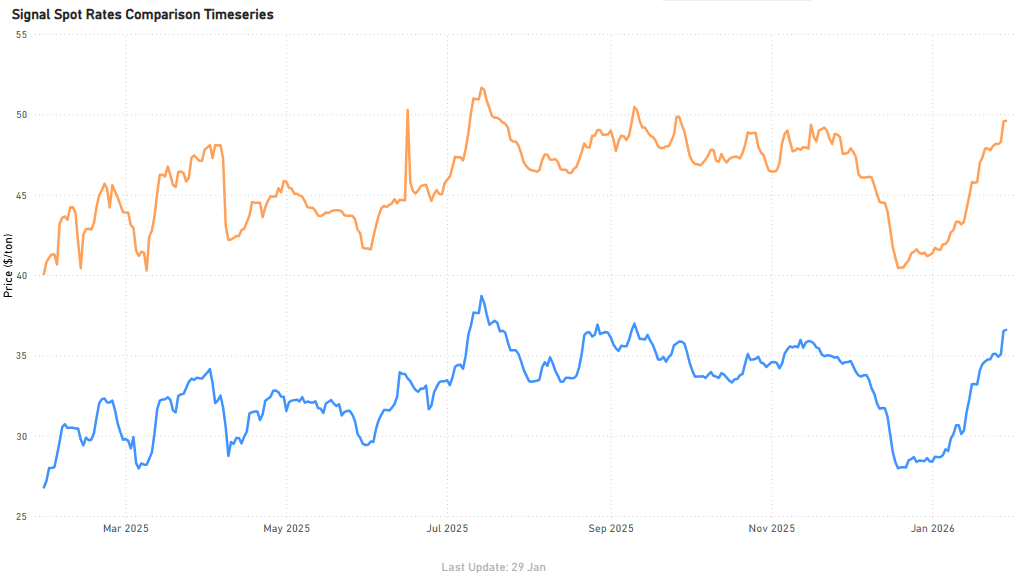

Supramax | Atlantic Firmer

Atlantic Supramax USG and ECSA softened on a month-on-month basis, but held firm week-on-week into late January. USG–Far East stood around $38.1/tonne (-0.5% m/m; +0.3% w/w), while ECSA–Far East was at approximately $33.4/tonne (-2.6% m/m; +1.8% w/w)

Handysize | Atlantic Firmer

Handysize Atlantic routes showed renewed weekly firmness, despite remaining softer on a month-on-month basis. Brazil–Skaw/Pass firmed to around $42.2/tonne (+2.2% w/w; -5.2% m/m), while USG–NCSA/Skaw-Pass strengthened to approximately $30.3/tonne (+2.0% w/w; -10.1% m/m)

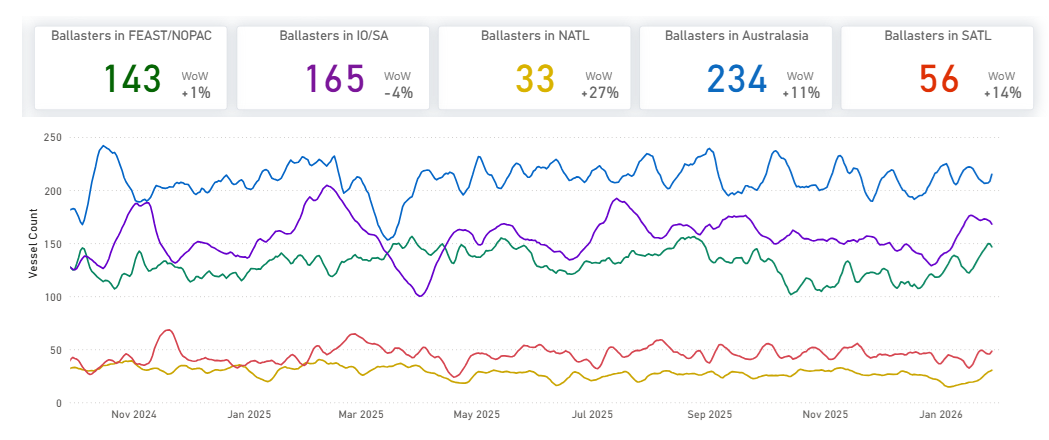

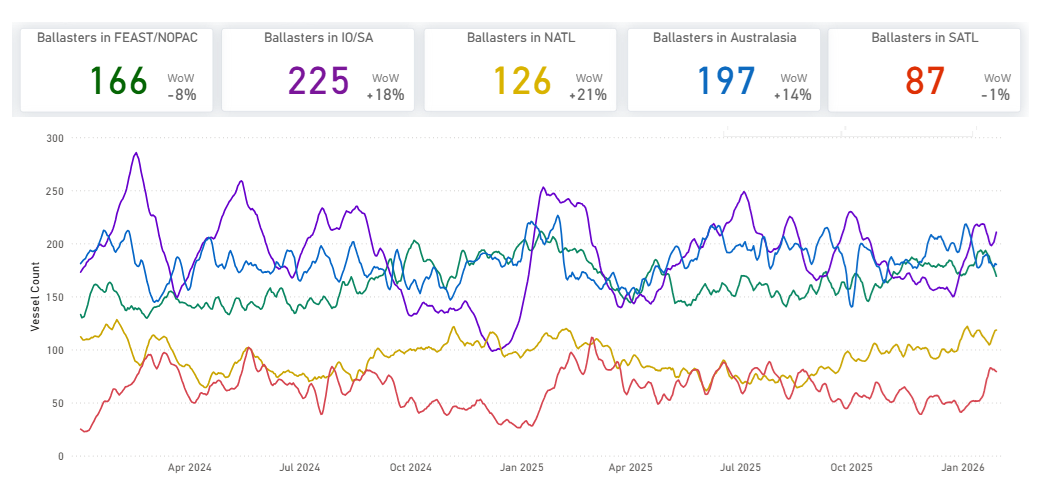

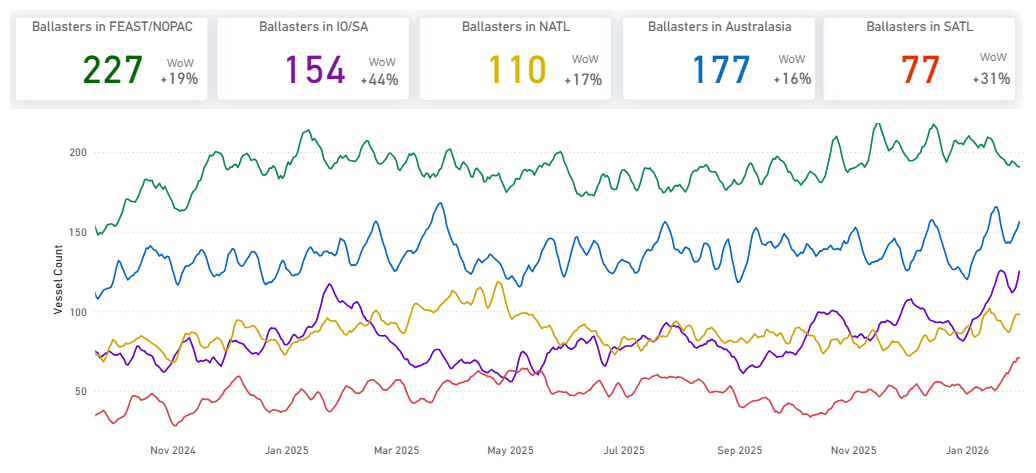

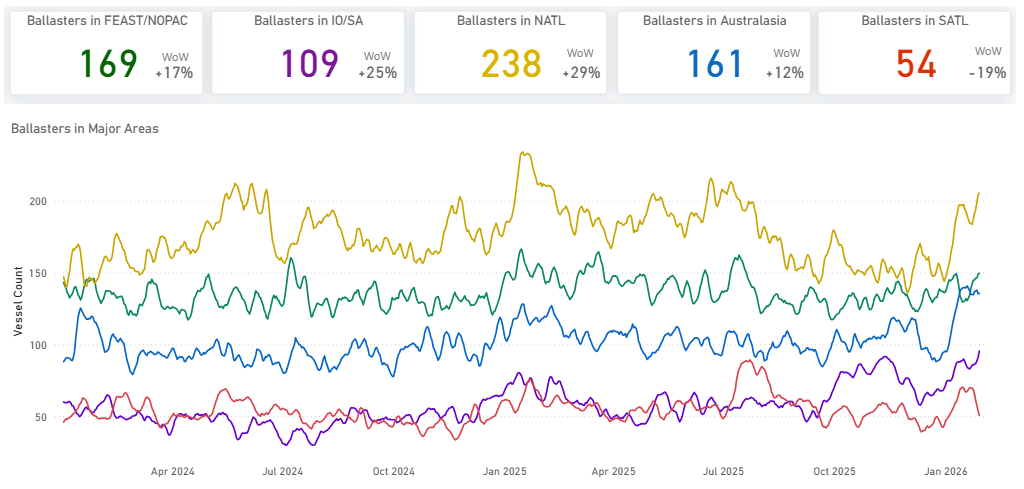

BALLASTERS OVERVIEW

Capesize | 5D MA Increasing

Supply pressure in the Atlantic significantly increased week-on-week, evidenced by a sharp rise in ballasters. Specifically, North Atlantic ballasters jumped to 33, marking a 26% week-on-week increase, while South Atlantic ballasters climbed to 57, an increase of 30% week-on-week.

Panamax | 5D MA Mixed

Supply pressure in the Pacific and Indian Ocean increased week-on-week. SE Asia/Australasia ballasters rose to 197 (+14% WoW), while Indian Ocean/South Africa ballasters climbed sharply to 225 (+18% WoW). FEAST/NOPAC ballasters stood at 166, remaining elevated despite an 8% WoW pullback.

Supramax| 5D MA Increasing

Supramax supply pressure increased both the Atlantic and Pacific week-on-week. North Atlantic ballasters climbed to 110 (+17% WoW) and South Atlantic rose to 77 (+31% WoW). In the Pacific, FEAST/NOPAC ballasters jumped to 227 (+19% WoW), while Australasia increased to 177 (+16% WoW).

Handysize| 5D MA Increasing

Handysize supply pressure remained elevated week-on-week, with increases seen in both the Pacific and Indian Ocean, while the North Atlantic was the sole area to see a decline. FEAST/NOPAC ballasters rose to 169 (+17% WoW), and Australasia increased to 161 (+12% WoW), while Indian Ocean/South Africa also increased to 109 (+25% WoW).

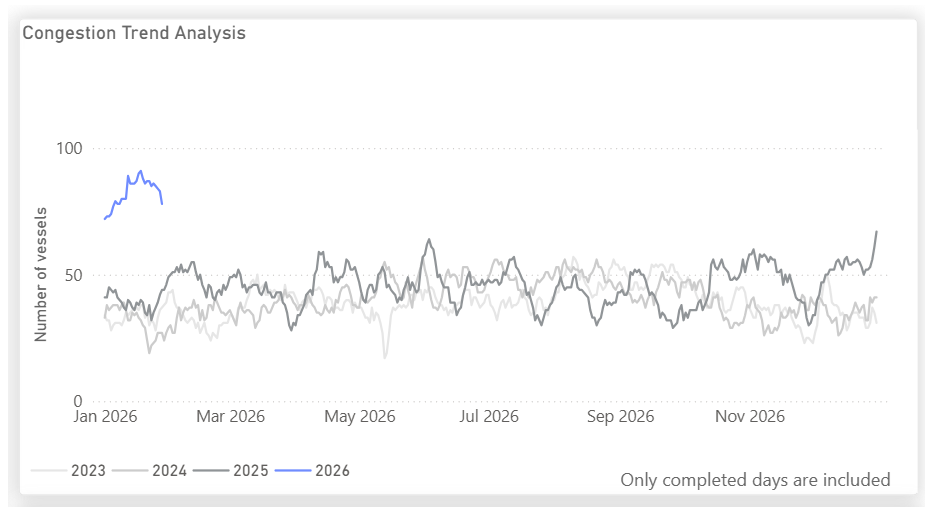

In January 2026, Chittagong experienced a notable increase in vessels anchored offshore, indicative of ongoing port congestion. This backlog aligns with recent news detailing slow discharge operations and limited unloading capacity, which have caused prolonged vessel turnaround times. The strain on berth and yard efficiency is evident, with sources indicating that importers are being pressed to clear cargo within a five-day window.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)