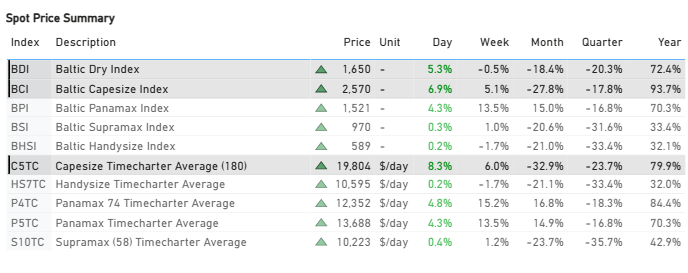

The Baltic Capesize Index opened the week marginally firmer, while weekly performance remains lower, indicating continued sensitivity in the freight market.

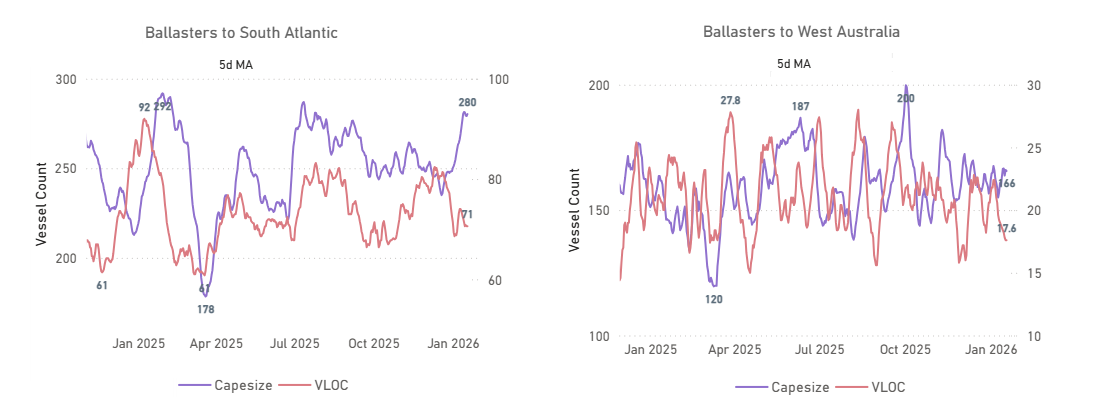

Ballaster availability remains elevated across both basins, with approximately 160 vessels (5-day MA) in West Australia and around 280 vessels (5-day MA) in the South Atlantic.

South Atlantic ballaster counts are around 40 vessels higher than at end-December, highlighting increased vessel availability relative to recent month-end levels.

Market Overview

Spot dry freight indices showed modest daily gains.

The past week delivered a series of developments with potential implications for dry bulk freight demand in the months ahead. At the opening of the third week of January (19 January), market conditions were reflected in Baltic Dry Index value (BDI) of around 1,650, alongside Baltic Capesize Index (BCI) near 2,570 and Baltic Panamax Index (BPI) at approximately 1,520.

On the iron ore front, as of 19 January, prices had declined for a fifth consecutive session, reflecting concerns around oversupply. The move followed confirmation from Beijing of a substantial reduction in steel output, alongside rising port inventories and the arrival of initial cargoes from Guinea’s Simandou project.

In parallel, developments in the coal sector continue to underline China’s central role in bulk commodity demand. China is preparing to commission more than 100 new coal-fired power generation units in 2026, accounting for 85 of the 104 projects planned globally and adding approximately 55 GW of capacity. Other countries, including India, Vietnam, and Indonesia, are also expanding capacity, with India contributing roughly 24 GW. As a result, China is expected to represent 86% of new global coal-fired power capacity entering operation in 2026, up from 78% in 2025, supporting expectations of sustained coal-related trade flows despite the overall energy transition.

Agricultural trade activity also remained firm. China was active in the soybean market, with up to 20 cargoes of US and Brazilian soybeans reportedly traded in the week ending 16 January. Market sources indicated that China is nearing completion of its 12 million metric tonne US soybean purchase target, with some participants suggesting total commitments could exceed this level.

FREIGHT MARKET

Capesize |Firmer

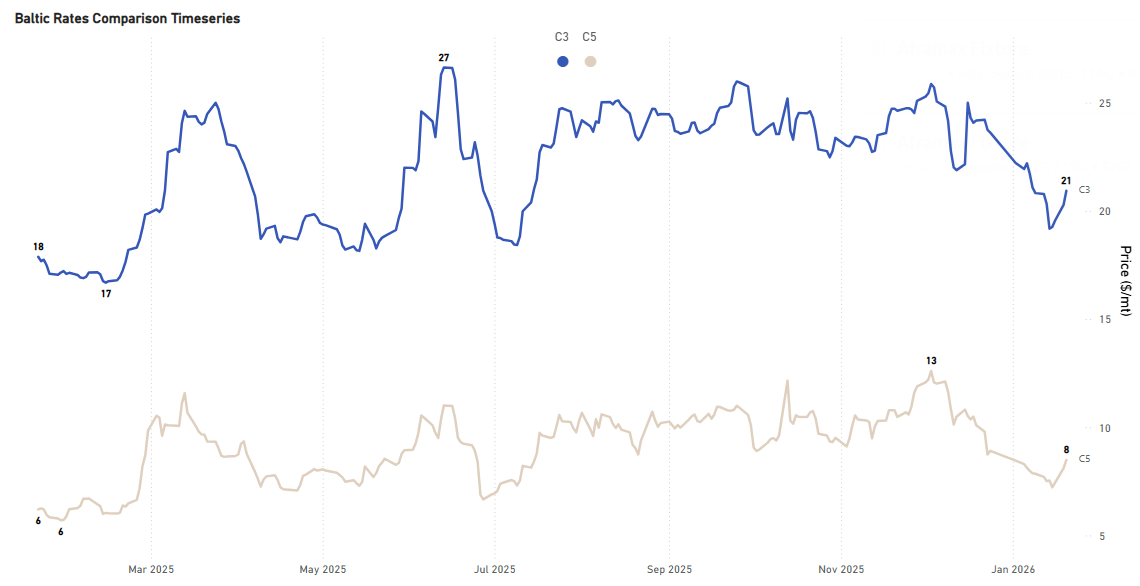

C3 – Tubarao to Qingdao is currently assessed at around $20.9/mt, with recent day-on-day (+3.2%) and week-on-week (+3.0%) increases. Over longer horizons, the performance remains lower, with rates 13.6% below month-ago levels and 14.6% below quarter-ago levels. Year-on-year comparisons remain higher at +17.0%. C3 is presently trading below its 52-week average of approximately $22.0/mt, indicating that current levels remain within the lower range of recent historical observations.

C5 – West Australia to Qingdao is currently assessed at around $8.5/mt, with recent day-on-day (+4.7%) and week-on-week (+13.0%) increases. Over longer horizons, rates remain lower, standing 13.3% below month-ago levels and 18.9% below quarter-ago levels. Year-on-year comparisons are higher at +36.8%. Similar to C3, C5 continues to trade below its 52-week average of approximately $9.1/mt.

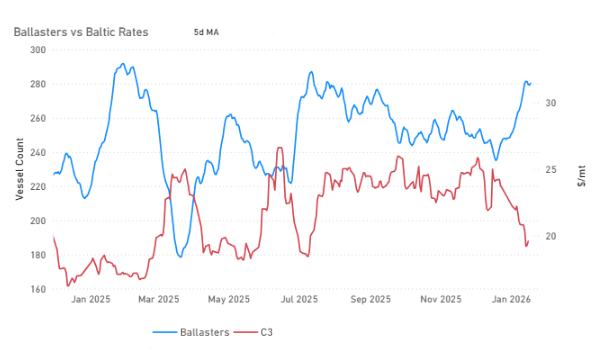

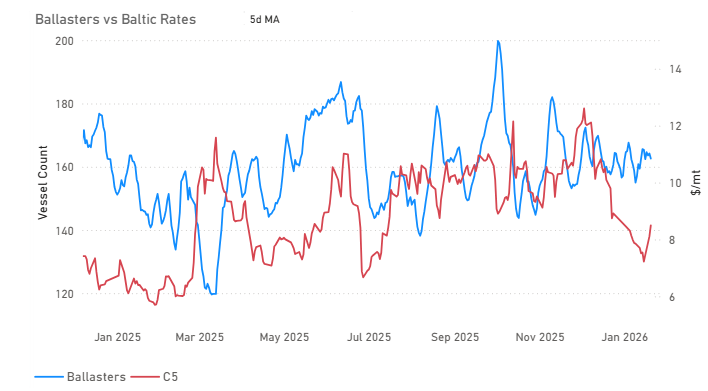

BALLASTERS | C3Increasing Vs Baltic Rates

Between 24 Dec 2025 and 20 Jan 2026, ballaster counts increased from 246 to 282 vessels, reaching a peak during the period between these two observation points, while C3 declined from $23.62/mt to $20.93/mt. This highlights higher vessel availability being observed alongside lower freight levels during January. With ballaster counts having reached a peak during January, subsequent changes typically reflect vessels being absorbed into employment, altering the level of visible ballaster availability.

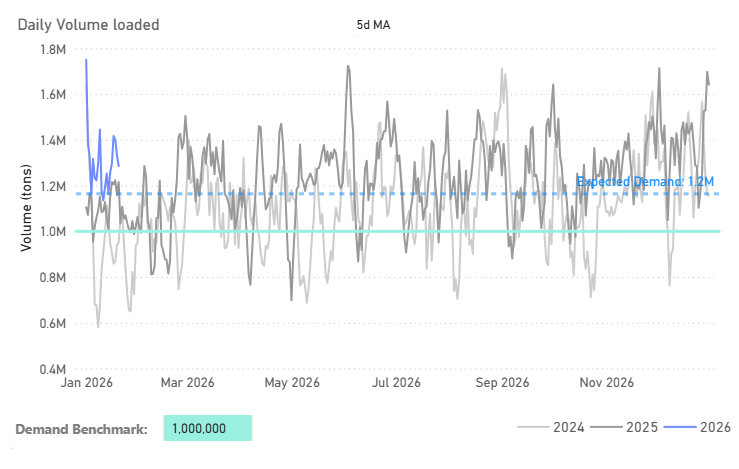

DEMAND | South Atlantic Daily Volume Loaded

When examining daily volume loaded in the South Atlantic for C3, recent data indicate that loadings have been occurring above the 1.0 million-ton benchmark. This suggests that cargo activity remains present, which may contribute to the absorption of vessel availability as the month progresses.

BALLASTERS | C5Steady Vs Baltic Rates

In contrast to the Atlantic, the Pacific market presents a different picture. As of 20 Jan 2026, ballaster counts stand at approximately 163 vessels, showing an almost steady trend for January, while C5 is assessed at around $8.50/mt.

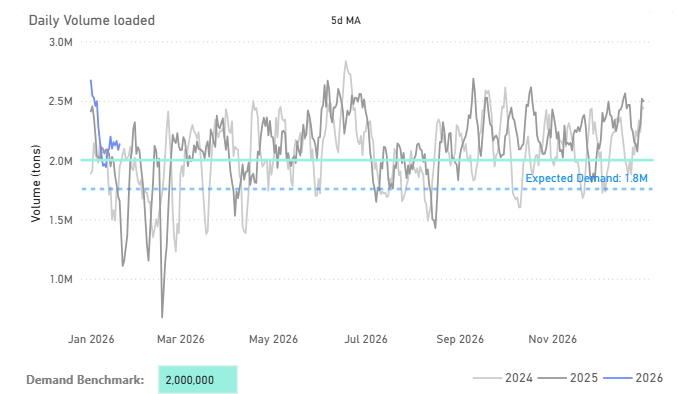

DEMAND | West Australia Daily Volume Loaded

Recent data indicate that Capesize demand in both the Atlantic and Pacific has been tracking close to, and at times above, established demand benchmarks. For West Australia, daily volumes have recently been recorded above the 2.0 million-ton level, highlighting sustained cargo activity in the region.

PORT CONGESTION | Discharge China

The number of vessels congested at Chinese discharge ports has recently been observed at higher levels, with current estimates around 150 vessels. This is above levels recorded toward the end of the previous year and higher than the lows seen earlier in the period, placing congestion toward the upper end of its recent range.

For subscription to our FREE weekly market trends email, please contact us: research@thesignalgroup.com

-Republishing is allowed with an active link to the source

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.png)

.avif)

.avif)

.avif)

.avif)

.png)