Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

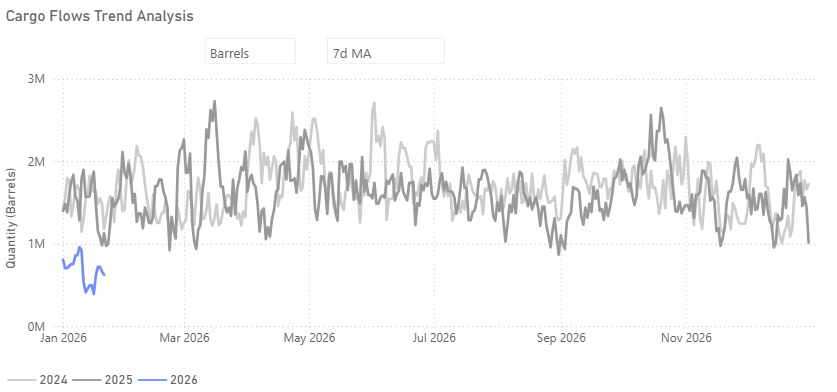

Chart of the Week| Dirty Oil Flows Russia - India

The downward trend in the 7-day moving average points to easing demand momentum

Figures reflect market-based estimates as of 22 January and remain subject to further revision.

Cargo-flow analysis indicates that Russian crude shipments to India slowed in early January, as reflected in the 7-day moving average across the first three weeks of the month. While India remains one of the most important destinations for Russian oil, current trends indicate a more gradual pace of arrivals compared to recent years.

By late January, the 7-day moving average indicated lower Russian crude shipments to India compared to prior years, with flows approximately 20% below 2022 levels and more than 50% below early-2024 benchmarks, based on rolling estimates that continue to be revised.

Publicly available tender data suggests that some Indian refiners are increasingly turning to Middle Eastern crude suppliers. Bharat Petroleum Corporation Limited is reported to have issued tenders for Iraqi and Omani crude covering periods of more than one year, and to have sought Murban crude from the United Arab Emirates under a separate tender. Similarly, Reliance Industries, one of the largest buyers of Russian crude earlier in the year, has publicly stated that it does not expect Russian deliveries in January. These developments help explain why aggregate Russian crude inflows into India did not strengthen during the month.

As a result, January Russian crude deliveries to India appear increasingly concentrated among a narrower group of buyers. These include Nayara Energy and select state-owned refiners, most notably Indian Oil Corporation, as several other refiners, both private and state-owned, have sought alternative crude supply.

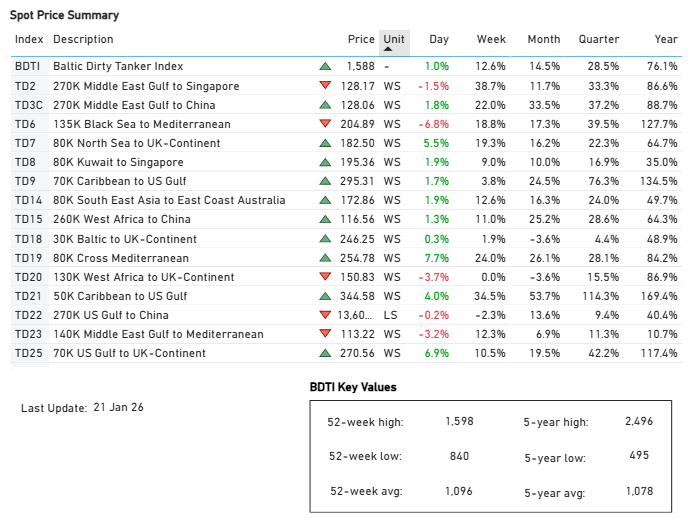

Market Overview

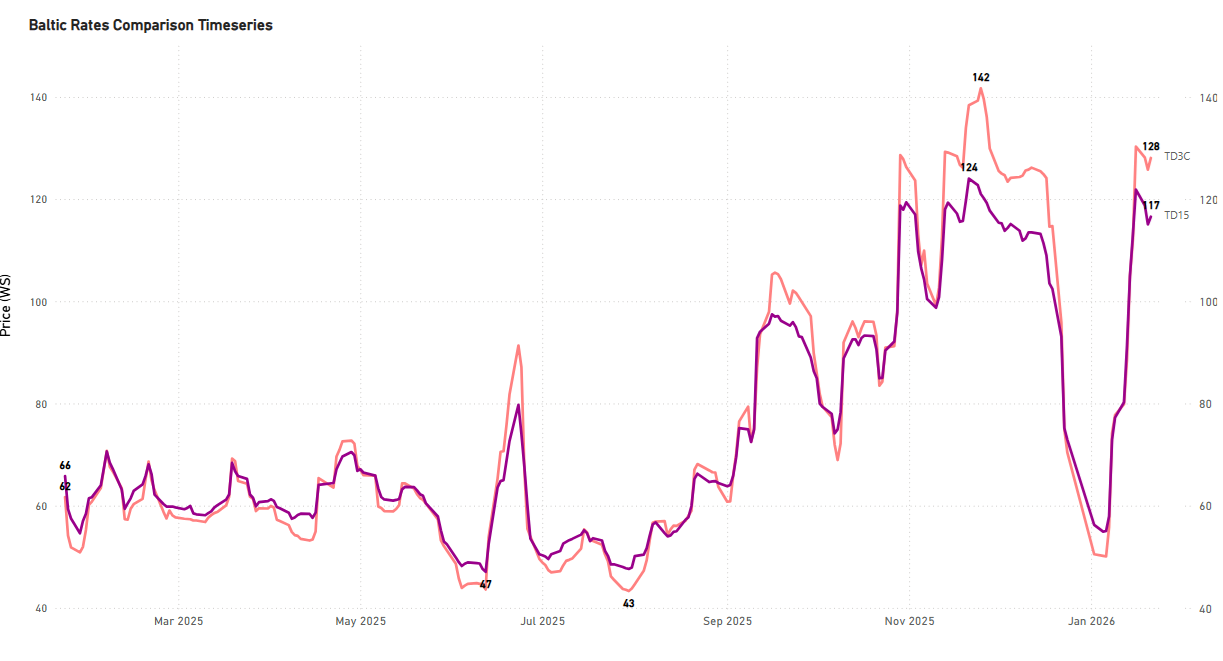

Spot freight indices showed a mixed mid-week picture, supported by firmer Aframax rates, while VLCC WS momentum corrected below WS130. Some of last week’s gains were nevertheless retained, after TD3C closed Friday at around WS130, below its most recent peak of WS139.28 on 24 November.

VLCCWeaker

WS rates for MEG–China (TD3C) and WAF–China (TD15) have rebounded from recent lows, but current levels remain below last Friday’s close. Both routes are now trading below WS 130, suggesting that the recent upside correction has yet to be fully confirmed. While near-term gains point to improving sentiment, the market will need to be tested through the remainder of the month to assess whether this upward correction can be sustained.

SuezmaxWeaker

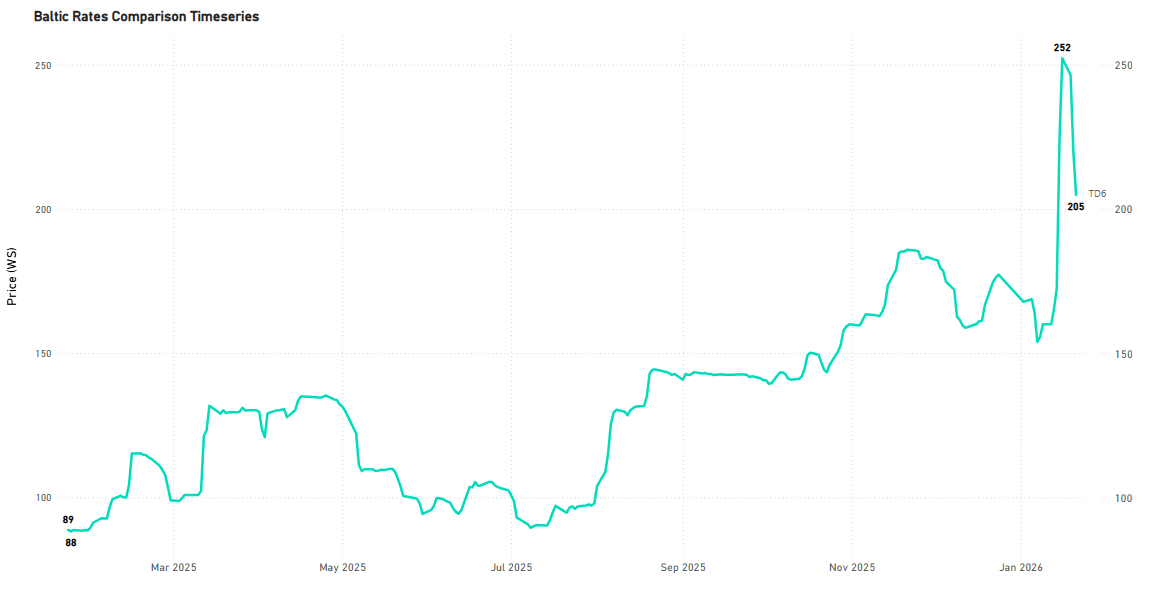

After peaking in mid-January, WS rates for Black Sea - Mediterranean (TD6) have retreated significantly, dropping from roughly WS 252 to the low-WS 200s, as supply conditions in the Black Sea increasingly signal oversupply.

AframaxFirmer

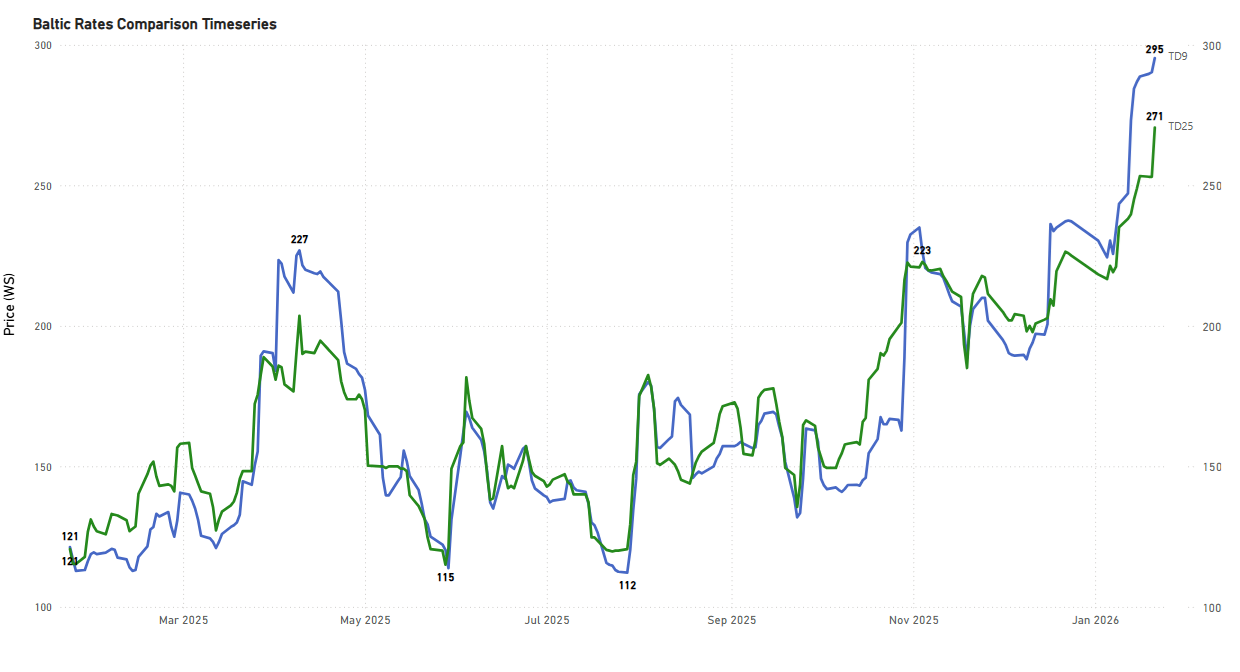

Since the start of the year, rates on TD9 and TD25 have steadily moved higher. TD9 has risen from around WS 230 in early January to close to WS 295, while TD25 has increased from the low WS 210s to above WS 270. The pace of gains has picked up in recent weeks, suggesting firmer underlying momentum as current supply conditions continue to underpin the market.

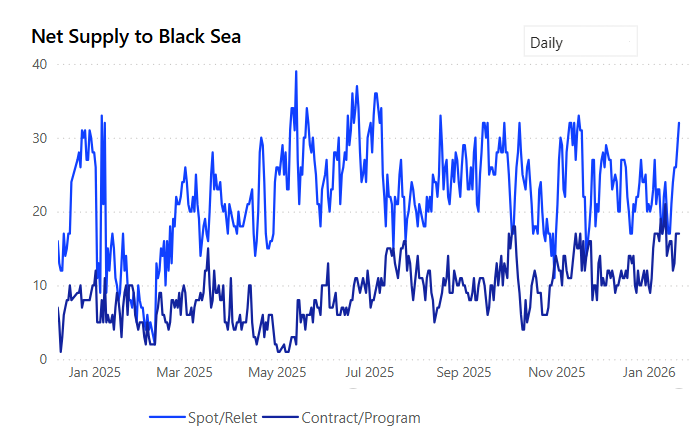

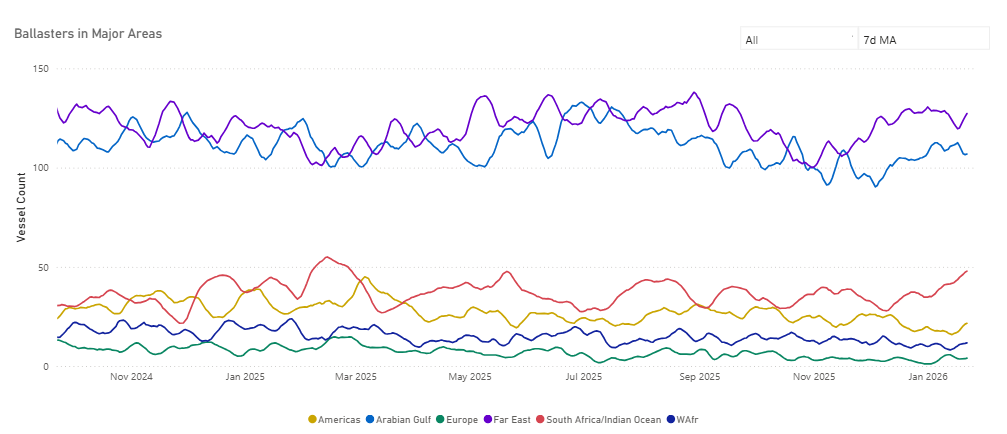

VLCC AG/India Supply Builds, Weighing on recent rate firmness

In line with our previous weekly estimate, ballaster counts in AG/India continue to sit in the upper tier (over 110 vessels), while the 7-day moving average shows a 5% week-on-week rise.

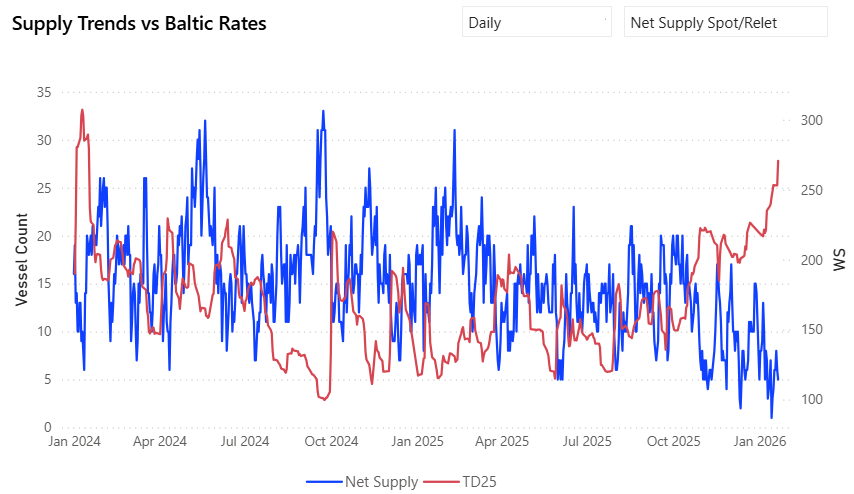

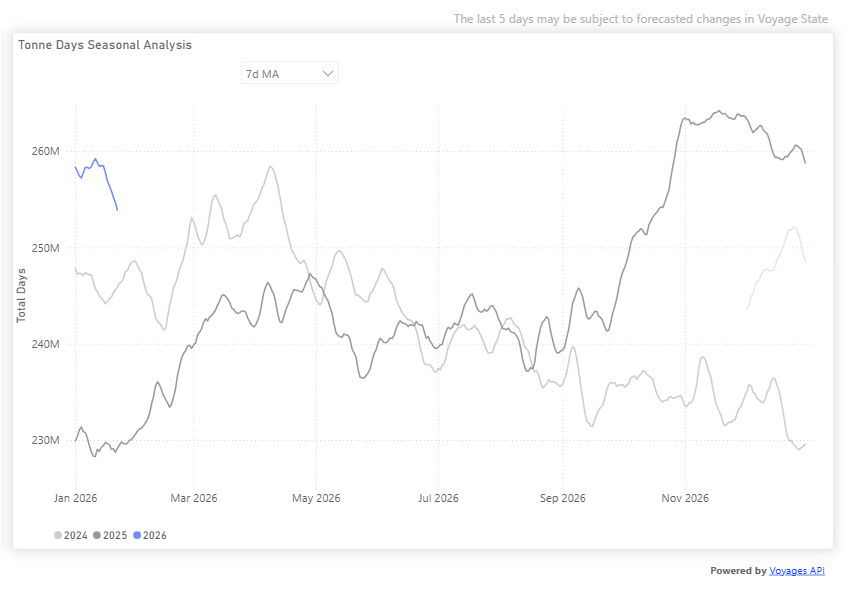

Dirty tonne-day growth has softened in recent weeks, pointing to a loss of momentum. Nevertheless, absolute tonne-day levels in 2026 remain notably higher than in prior years, running around 11% above 2025 levels and approximately 3% above 2024, suggesting that demand conditions are still relatively firm despite the recent easing.

Takeaway

VLCC rates have rebounded from recent lows, though current levels remain below prior peaks, suggesting that the recovery has yet to be fully confirmed.

VLCC Ballaster counts in AG/India remain in the upper range and continue to build on a week-on-week basis, limiting upside potential.

In the Suezmax segment, TD6 rates have corrected from mid-January highs, with supply conditions in the Black Sea increasingly weighing on sentiment.

Aframax rates on TD9 and TD25 have continued to strengthen since the start of the year, with momentum further improving.

Dirty tonne-day growth has softened in recent weeks, but overall demand levels remain above prior years.

For subscription to our FREE weekly market trends email, please contact us: research@thesignalgroup.com

-Republishing is allowed with an active link to the source

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.png)

.avif)

.avif)

.avif)

.avif)

.png)