Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

COMMODITY RADAR | Spotlight: BAUXITE

Bauxite flows are redirected as the war in the Arabian Gulf closes the Strait of Hormuz.

India has emerged as a key destination for bauxite as risks in the Arabian Gulf rise.

Bauxite flows increased by 22% in February.

Flows have increased outside of China by 36% y/y.

Flows to China have increased by 19%.

India was the destination for close to 1.2 mt of bauxite in February, as flows to the UAE tumble.

Source: Bauxite carrying Capesize tonne-miles from Signal Ocean https://app.signalocean.com/dry/dynamic/timeseries_dry

At the start of 2026, seaborne bauxite flows reached 22 mt in February, up 22% from the same period last year. China remains the largest importer of seaborne bauxite, with Signal Ocean tracking a 19% y/y increase in February.

However, the more interesting growth came from India. Bauxite flows to India from shipments departing in February quadrupled. As a result, India received around 1.2 mt of bauxite, compared to the typical 200kt to 300kt.

These additional flows would likely have been destined for the Arabian Gulf, in particular, the UAE. Given the need for low-cost power for the processing of bauxite into alumina and then for turning alumina into aluminium, the Arabian Gulf has been a growing hub for bauxite imports, as there are limited domestic supplies.

Yet, with the war in Iran and the risks of transiting the Strait of Hormuz, many February shipments of bauxite destined for the UAE were diverted to India, given its geographic location and large bauxite processing capacity. As a result, February 2026 saw India leapfrog the UAE to become the largest receiver of seaborne bauxite excluding China, taking 5.2% of global shipments according to Signal Ocean. India typically takes less than 3%.

Source: Seaborne bauxite flow destinations in February 2026 from Signal Ocean https://app.signalocean.com/dry/dynamic/drybulkflows

Current bauxite prices have declined by around 50% since January 2025, and with buyers from the Arabian Gulf unlikely to be buying in the market, prices will continue to face some pressure. As a result, we are seeing China increase its market share of imports, moving to over 91% in March 2026 so far. This price slump has not gone unnoticed, with the Guinean government looking at curbing production or strictly enforcing mining companies to keep outputs within their licensed tonnage. This would impact capesize demand.

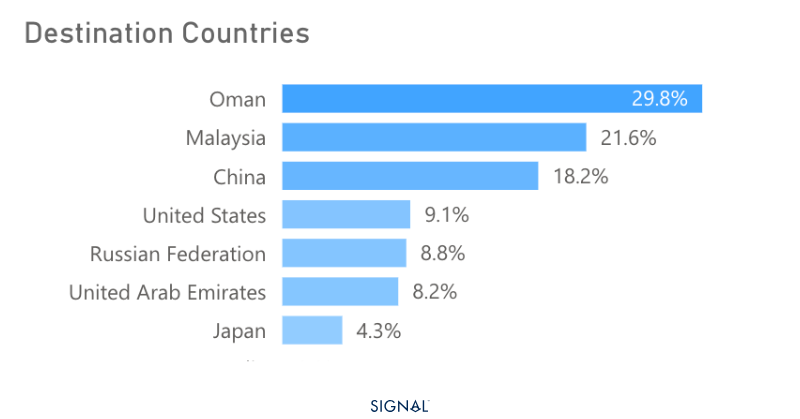

Bauxite flows to India in March so far have softened, likely a result of slower buying as stocks reach adequate levels. The data is also showing an increased quantity of alumina flowing out of India, 40% up YTD, as domestic production increased due to increased bauxite flows, while domestic aluminium production hasn't kept pace. Since February, Oman has been the largest recipient of Indian alumina, as other Gulf nations are deemed too risky to deliver to, given the Iran war. Oman is located before the opening of the Strait of Hormuz. We expect India to have consistently higher exports of alumina whilst the war in Iran continues.

Source: India alumina flows in February and March (at-time-of-writing) 2026 from Signal Ocean https://app.signalocean.com/dry/dynamic/drybulkflows

The war in Iran has shifted bauxite flows

India’s temporary emergence as a major importer reflects both geographic advantage and latent refining capacity, but is unlikely to be long-lived if the war ends without escalation. In the near term, weaker prices and shifting arbitrage routes will support alumina exports from India. Longer term, supply discipline from Guinea and evolving trade routes will be critical. Yet, given the expectation of aluminium demand growth, albeit modest, bauxite will continue to provide a positive pillar for capesize demand, particularly from West Africa.

Luke has over 8-years of experience analysing and forecasting commodity markets, with particular expertise in stainless steel raw materials and the wider metals markets.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)