Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Spotlight | Ballasters Vs Baltic Rates

Capesize Vs Panamax

April ends with firm sentiment in both Capesize and Panamax segments. On the C3 route, freight levels are supported by ballaster counts trending below the 12-month average. In Panamax, low ballaster availability across the P1/P2/P7 routes signals an undersupplied market, underpinning current rate strength.

Source: Signal Ocean Platform | Cape - Panamax Insights Data (last update: April 28, 2026)

FREIGHT MARKET OVERVIEW

The Baltic Dry Index is approaching 2,700 points, with gains recorded across all sub-indices: Capesize leading at +117.4% YoY, followed by Supramax +58.2%, Handysize +41.8%, and Panamax +40.9%.

Source: Signal Ocean Platform | Market Prices Data (last update: April 28, 2026)

P7 | US Gulf to Qingdao grain | 68.69 $/MT | Day: +0.01 | Week: -0.78 | Year: +22.37

Supramax S4A / Handysize HS4_38 Firmer

S4A | US Gulf trip to Skaw-Passero | 28,100 $/day | Day: -143 | Week: +1,379 | Year: +14,021

HS4_38 | US Gulf trip via US Gulf or North Coast South America | 14,071 $/day | Day: +392 | Week: +1,600 | Year: +3,850

FREIGHT PACIFIC

Capesize | C5 Firmer

C5 West Australia–Qingdao

C5 | West Australia to Qingdao | 13.20 $/MT | Day: +0.17 | Week: -0.32 | Year: +5.13

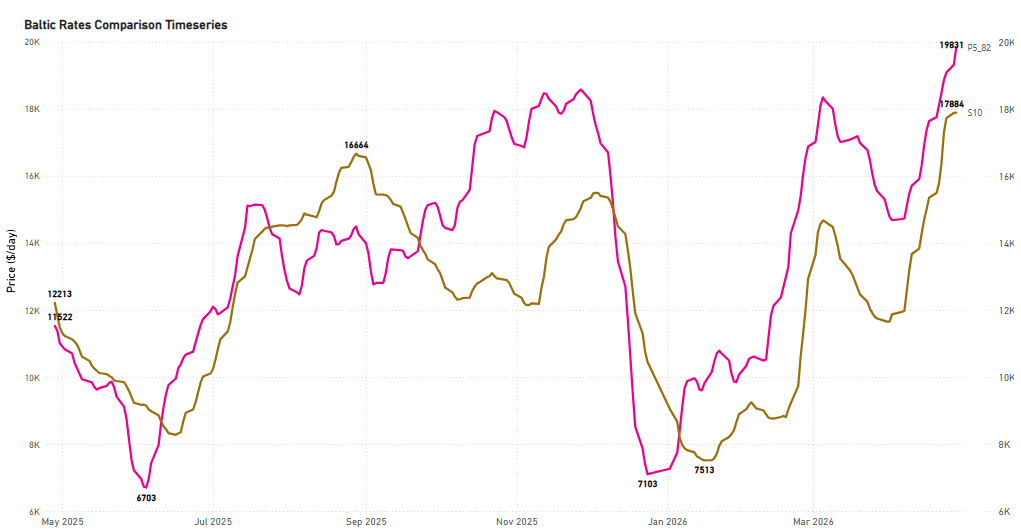

Panamax P5_82 / Supramax S10 Firmer

P5_82 | South China, Indonesian round voyage | 20,244 $/day | Day: +413 | Week: +1,772 | Year: +8,863

S10 | South China trip via Indonesia to South China | 17,668 $/day | Day: -216 | Week: +1,305 | Year: +5,832

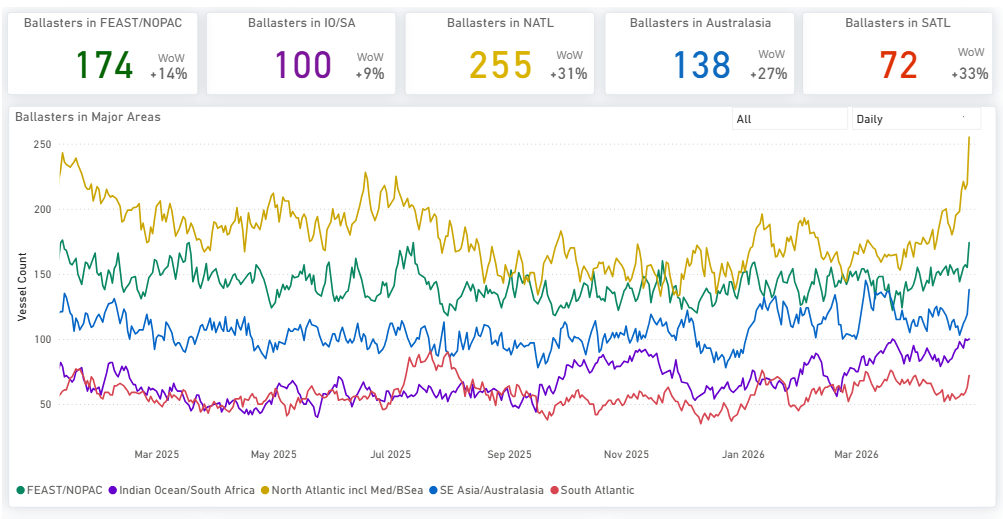

BALLASTERS OVERVIEW

We take a closer look at the basins of ballast count increases per vessel size segment.

Capesize:Ballasters are rising in the Indian Ocean/SA to more than 160 (+8% WoW), while in Australasia the count has sustained at 200.

Panamax: Atlantic basins are surging. NATL up +38% WoW and SATL up +32% WoW, while FEAST/NOPAC basin shows modest growth.

Supramax: The North Atlantic basin is surging with the count up +40% WoW and FEAST/NOPAC up +20% WoW.

Handysize: Ballasters are surging in the Atlantic and Pacific, with NATL and SATL leading at +31% and +33% WoW. The Indian Ocean is growing at a more measured pace of +9%.

By the end of April, Supramax and Panamax are losing momentum, while Capesize is showing a renewed upward trend. Despite the recent softening, both Capesize and Panamax indices remain above the 100% threshold, indicating still-elevated demand levels, whereas Supramax continues to lag below.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)