Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

COMMODITY RADAR | Spotlight: STEEL

The war in Iran will have knock-on effects for the steel markets in the upcoming months.

Indonesia continues to absorb excess Chinese steel in 2026

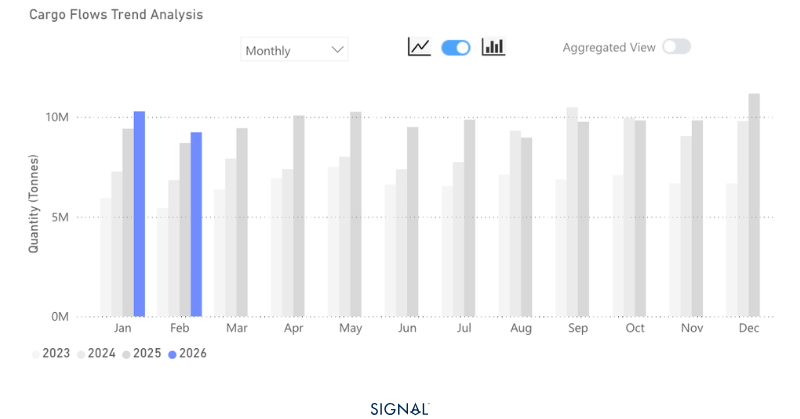

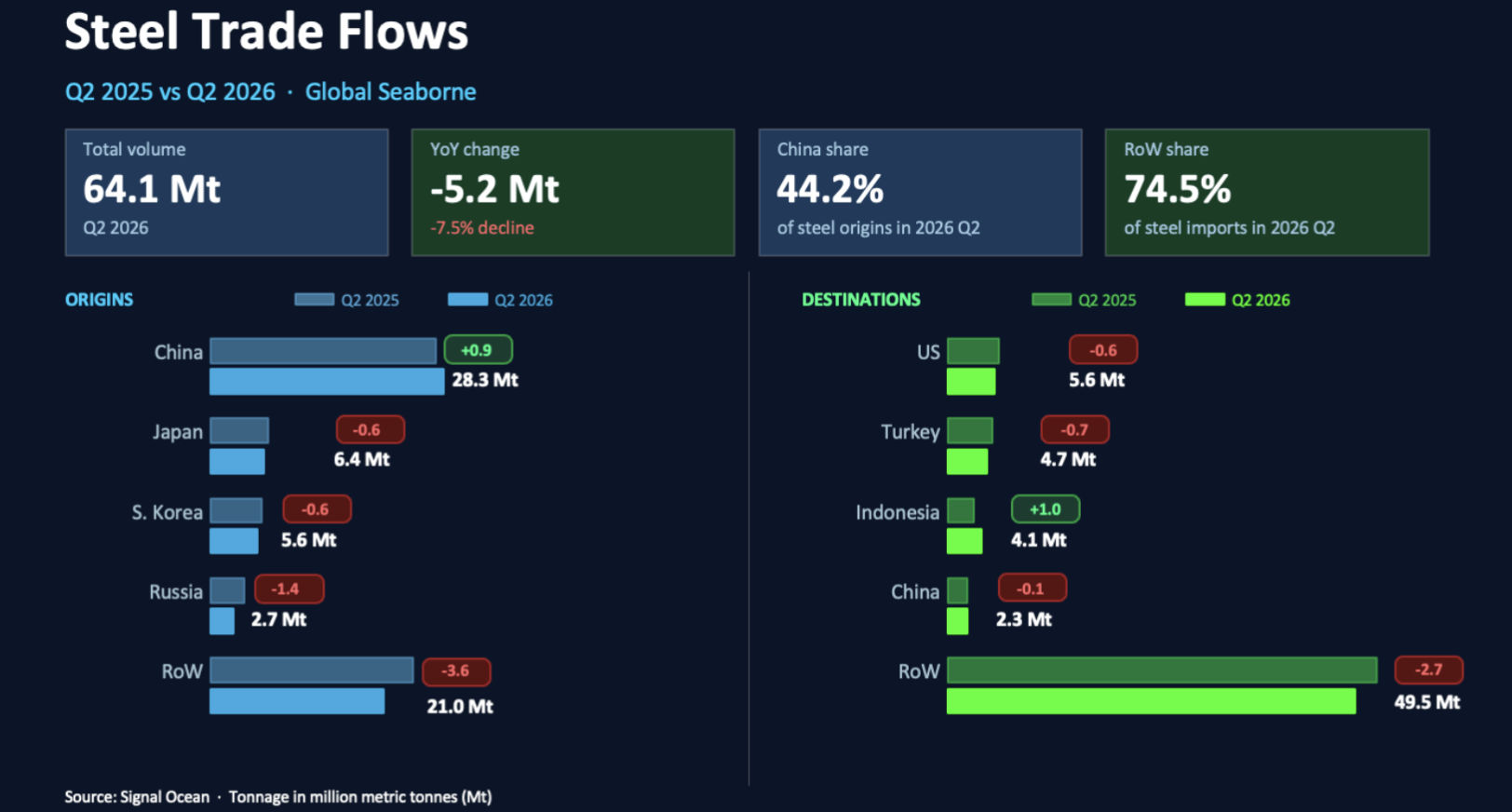

Global steel flows remain flat in February.

Flows from China have increased by 6%.

Flows from outside of China have decreased by 4%.

Indonesia's seaborne imports of steel surged by over 42% in February.

Source: Steel tonne-miles from Signal Ocean https://app.signalocean.com/dry/dynamic/timeseries_dry

Seaborne steel flows reached 21.1mt in February 2026, up less than 1% from the same period last year. The global flatline came despite a 6% rise in steel flows from China, as this was mitigated by an aggregated fall of 4% elsewhere.

The relationship between Chinese steel exports and domestic steel production continued in the typical trend in 2026 so far. Weaker domestic production, a result of weak domestic demand, drives producers to find export markets. For the first two months of 2026, Chinese crude steel production fell by 4%, as exports rose by 9% in January and 6% in February.

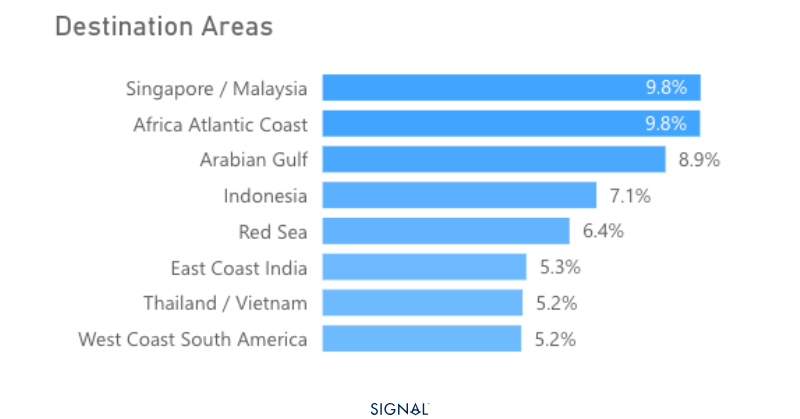

The largest receiver of these increased flows has been nations in South East Asia, most notably Indonesia, Singapore, and Malaysia, which have combined to account for just shy of 20% of all Chinese steel exports in 2026 so far. These regions have absorbed the surge in shipments due to their expanding construction and infrastructure sectors, as well as their strategic positions as regional trading hubs. This shift underscores a growing reorientation of Chinese steel exports away from traditional Western markets toward the dynamic economies of the Asia-Pacific region.

Source: Seaborne steel flows from China from Signal Ocean https://app.signalocean.com/dry/dynamic/drybulkflows

The disruption in the Arabian Gulf has yet to materially impact global steel flows, although early signs of regional dislocation are emerging. Historically, the region accounts for around 11% of Chinese steel exports, making it the single largest regional destination. In 2026, this share has declined to 8.4%, falling behind key Southeast Asian markets and the African Atlantic coast. While this may partly reflect an acceleration of pre-existing trade reorientation toward Southeast Asia, continued disruption to transit via the Strait of Hormuz would likely reinforce this trend by increasing both cost and uncertainty around deliveries into the Gulf.

To date, the limited global impact reflects the relatively low time sensitivity of steel shipments, alongside the ability of markets to absorb short-term disruption through inventory drawdowns and shipment delays. As such, the primary transmission mechanism is likely to be indirect, via energy markets rather than physical trade flows.

Steel production remains highly energy-intensive, accounting for approximately 7–8% of global final energy demand. Sustained increases in energy prices would push production costs and compress margins. Rather than driving immediate demand destruction, this is more likely to trigger supply-side adjustments, with higher-cost capacity curtailments in regions such as Europe.

While this could, in theory, widen arbitrage opportunities and support import demand, the extent of any increase in trade flows will be constrained by existing protectionist frameworks, including safeguard measures. As a result, any uplift in imports is likely to be incremental, reflected in higher quota utilisation rather than a step-change in volumes.

Against this backdrop, Chinese steel exports are expected to remain resilient. The ongoing structural shift toward Southeast Asia, where demand is underpinned by construction-led growth and trade barriers are relatively limited, provides a stable outlet for surplus Chinese production. As such, the net effect of current geopolitical disruption is likely to be a reinforcement of existing trade patterns rather than a material reconfiguration of global steel flows.

Source: Chinese steel exports in 2026 by destination region from Signal Ocean https://app.signalocean.com/dry/dynamic/drybulkflows

China’s steel exports can withstand the war in Iran

In summary, the disruption in the Arabian Gulf is unlikely to drive a material reconfiguration of global steel trade flows, at least in the near term. While regional dislocations are emerging, these appear to reflect a combination of logistical friction and an acceleration of existing trade shifts rather than a structural break. The more meaningful transmission channel remains indirect, via higher energy prices, which are likely to compress margins and prompt supply-side adjustments in higher-cost regions such as Europe. However, any resulting increase in import demand will be tempered by entrenched protectionist measures. Against this backdrop, China’s export position remains robust, supported by strong demand across Southeast Asia and limited exposure to energy-driven cost inflation. As such, current geopolitical tensions are more likely to reinforce prevailing trade patterns than to materially disrupt them

Luke has over 8-years of experience analysing and forecasting commodity markets, with particular expertise in stainless steel raw materials and the wider metals markets.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)