Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Spotlight |Asset Benchmark Assessments — NB vs 5Y & NB vs Resale

Asset market anomaly - not just freight

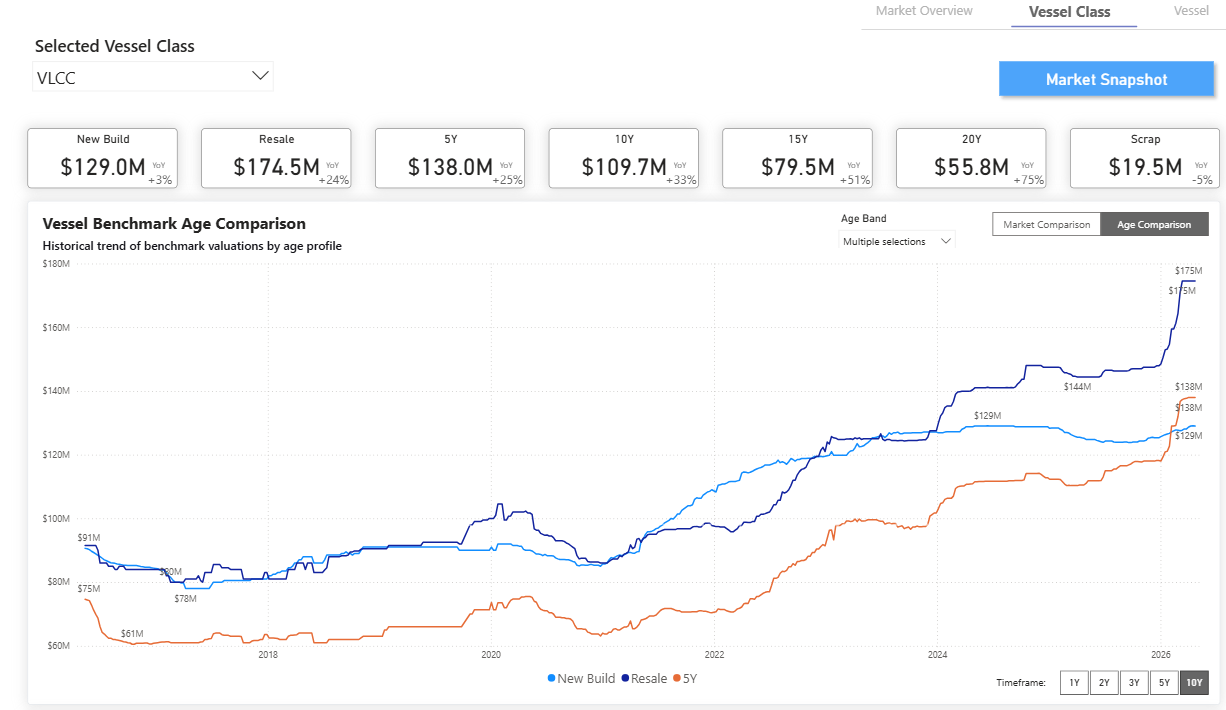

Indicative benchmark valuations by age profile

We take a closer look at the evolution of ship price assessment in the crude carrier segment. At the end of February, we highlighted growth in values for the VLCC segment and foresaw an upward trend, despite the threat of geopolitical risk at the time. We also highlighted the age discount tightening and the narrowing of the spread between five- and ten-year-old vessels, with buyers’ interest in mid-aged tonnage. Now, after more than 60 days of Hormuz disruption, we review the evolution again, and it seems that the age depreciation curve has been lost.

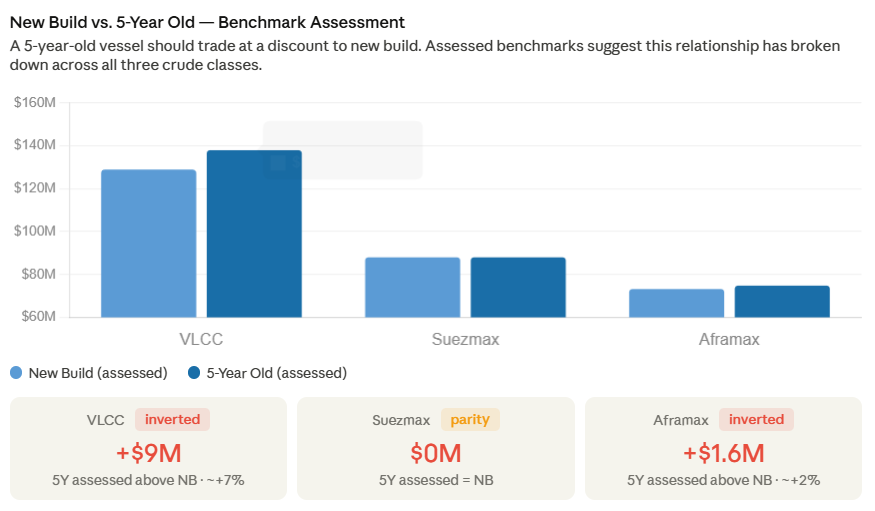

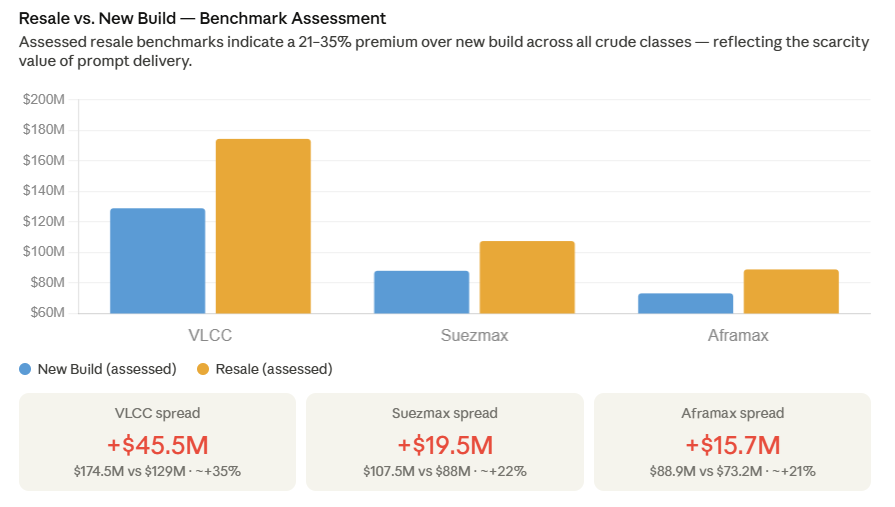

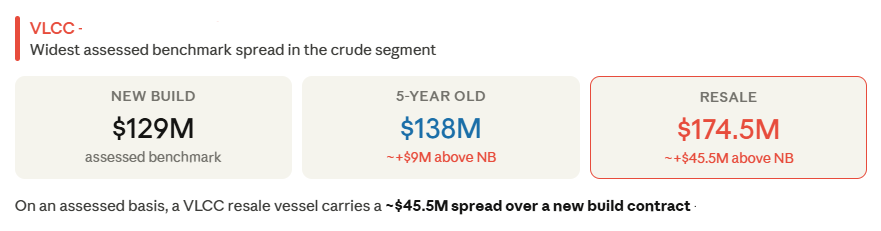

In normal conditions, a resale vessel earns a modest premium for saved wait time, and a 5-year-old ship trades at a clear discount to a new build. Neither is true today. VLCC 5-year-old tonnage trades $9M above a new build contract; Suezmax sits at dead flat; Aframax has also inverted. On the resale side, buyers are paying 21–35% over NB, $45.5M excess on a VLCC alone, purely for prompt availability.

Benchmark MethodologyValuations for newbuilds, resale, and age-specific benchmarks are derived from statistical models based on benchmark vessels per vessel class.· VLCC benchmark: 310k dwt (44,170 lwt), built in Korea · Suezmax benchmark: 157k dwt (24,387 lwt), built in Korea · Aframax benchmark: 114k dwt (18,899 lwt), built in Korea

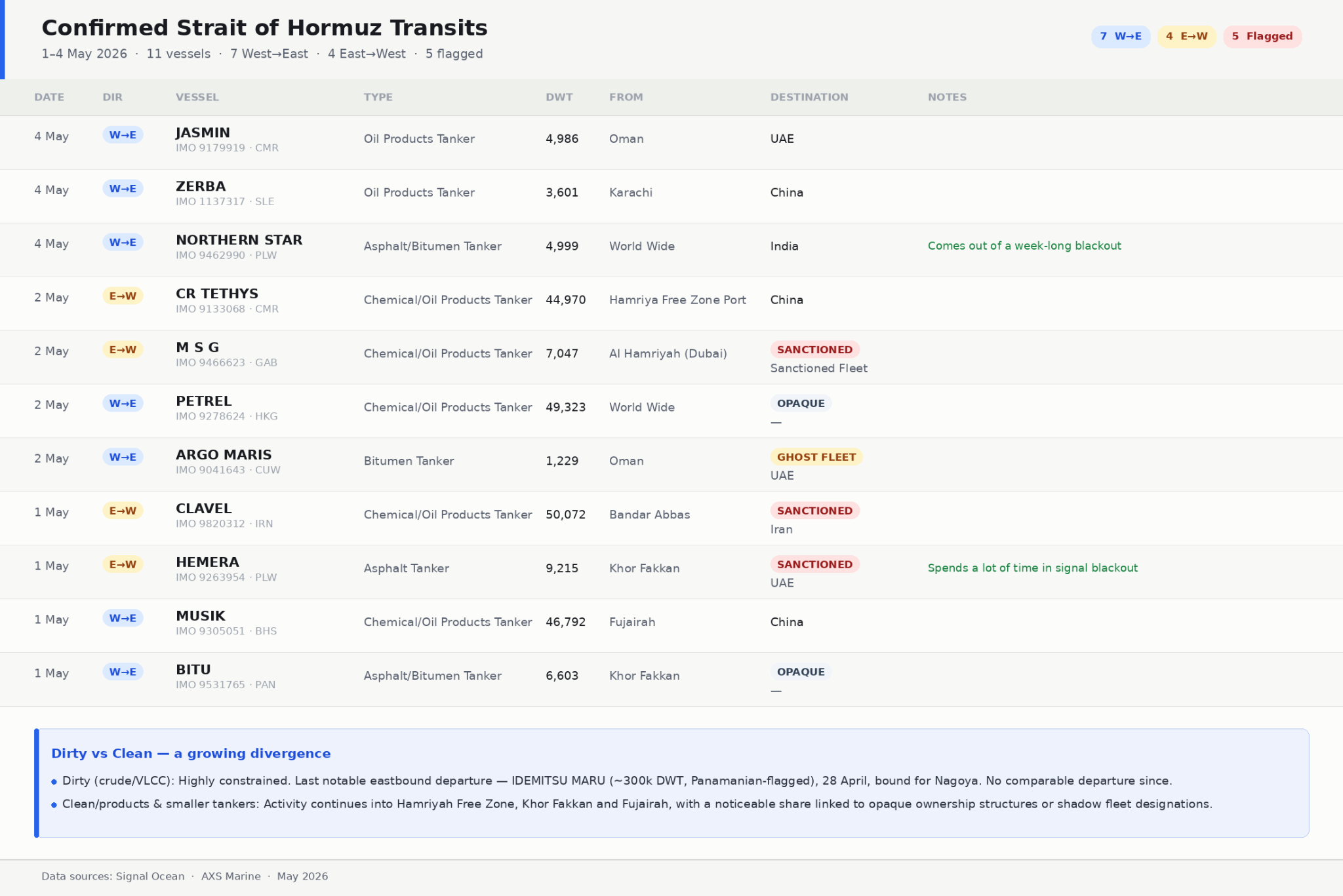

Vessel Crossings | May observations

Disruption in the Middle East has continued to dominate oil and tanker market dynamics, with tanker transits through the Strait remaining >95% below pre-conflict levels.

Transits on Iranian waters

Iran’s new routing regime around Larak Island has increased the degree of political and military oversight applied to commercial transit through the Strait of Hormuz.

Iran’s Islamic Revolutionary Guard Corps (IRGC) has instructed commercial vessels seeking transit through the strait to coordinate with Iranian authorities and follow designated routes near Larak Island.

Under the reported routing pattern, inbound vessels heading into the Gulf pass north of Larak Island near the Iranian coastline, while outbound vessels transit south of the island. The arrangement shifts traffic closer to waters claimed by Iran and gives the IRGC greater ability to monitor passing ships.

Iran has also described controlled or restricted monitoring areas between the traffic lanes overseen by the IRGC. This represents a departure from the traditional traffic separation scheme, which relied more heavily on routes associated with Omani waters and internationally managed navigation patterns.

While international maritime law still recognizes transit rights through the Strait of Hormuz, critics argue that the new system increases Iranian operational control over vessels during passage.

The Mine Threat

Crucially, the operational outlook remains constrained by the mine threat. Although US and allied naval forces are expected to prioritize mine countermeasure operations, some warnings indicate that fully securing the Strait could take months, and that some residual mine risk may persist even after clearance efforts.

This lingering uncertainty is central to the freight outlook, as marine insurers are generally less constrained by volatility than by difficult-to-quantify security risk. Without clear visibility on residual mine threats, predictable operating conditions, and sustained freedom of navigation, war risk cover is likely to remain restricted, selectively available, or prohibitively expensive.

As a result, even if partial transit resumes through routes designated by Iranian authorities, traffic is likely to remain constrained and operationally inefficient, reinforcing vessel displacement toward the Atlantic Basin and sustaining elevated freight rates.

The net effect could be a more durable reconfiguration of tanker markets, in which insurance constraints and security uncertainty, not just physical disruption, support Atlantic Basin strength and increase the strategic importance of US Gulf-driven flows.

Oil Macro

Hormuz transit risk is no longer a temporary overhang, and the East-West split deepens in the freight market. The supply shock is historic in scale. IEA has placed the current disruption above 1973, 1979, and 2022 in severity, 12 million bpd of crude supply affected versus 5 million bpd during the OPEC embargo. Brent above $110 and WTI above $100 are the market's response to that arithmetic.

Two producer-side developments complicate the picture. The UAE's departure from OPEC signals a longer-term pivot toward unconstrained output growth, relevant for post-normalisation supply, less so for today's constrained flows. Meanwhile, the 188kbd OPEC+ increase agreed by remaining members, including Kuwait, appears to be too small to significantly offset Hormuz-scale disruption and reads more as a political signal than a market intervention. Asian importers are feeling the squeeze most acutely, with Middle Eastern crude arrivals down sharply and U.S. barrels partially, but not fully, filling the gap.

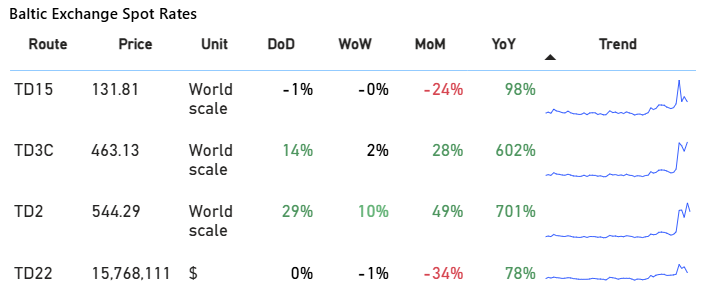

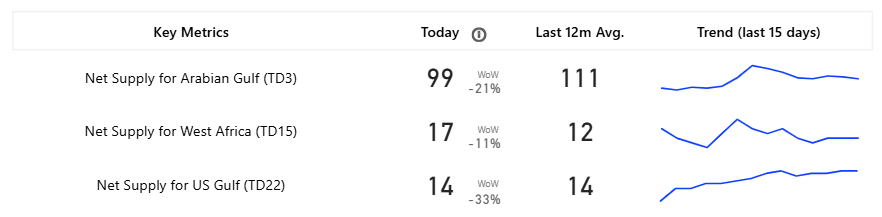

FREIGHT | VLCC latest signal trends

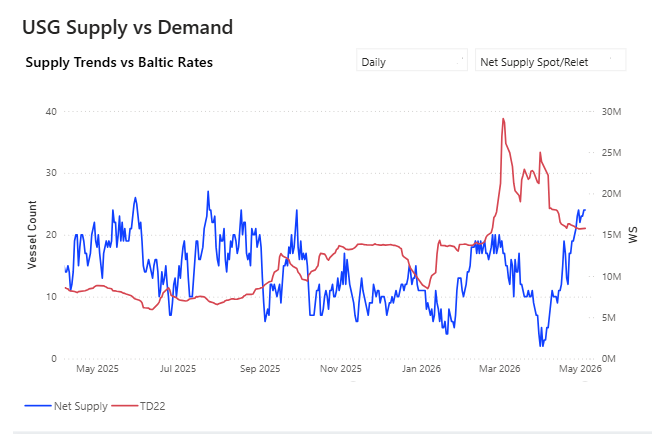

With Atlantic freight markets increasingly driven by supply-side signals, one clear trend has been the growing number of ballast VLCCs in the US Gulf. Average vessel counts have risen toward the 60 mark, contributing to the downward pressure on rates observed at the start of May.

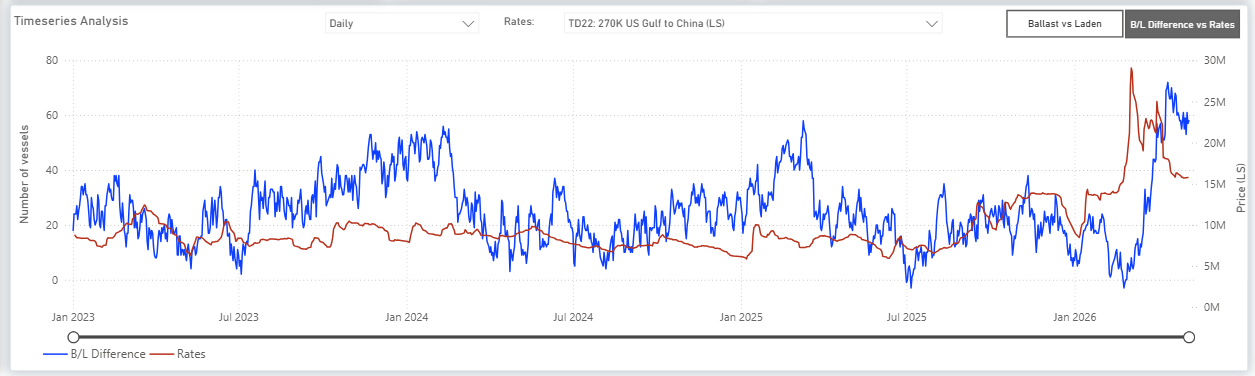

Based on the current supply levels, the TD22 route has shown an increasing trend over the last 15 days, with the daily vessel count now more than 20, compared with a record low of 2 at the start of April.

Current monthly freight metrics indicate a 34% decline, though the year-on-year increase remains substantial at 78%. While net supply has been trending upward since mid-April, this has not yet translated into a significant market correction. However, the rapid buildup of ballasting vessels may begin to exert more downward pressure in the near term. A review of the net supply over the past 15 days shows that the West African (TD15) route is experiencing a downward trend; despite this, market sentiment for the current week remains stable with no notable volatility.

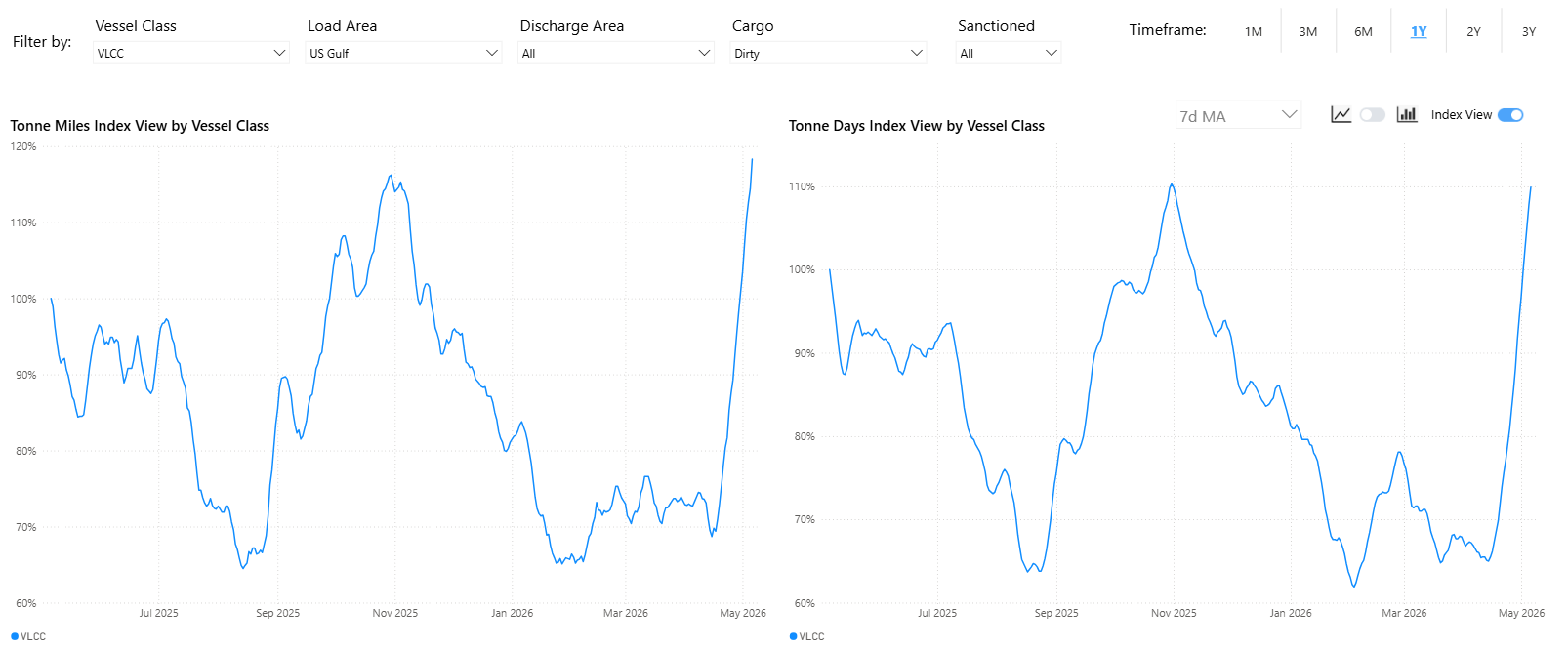

For freight markets, the impact is less about a complete halt in global flows and more about the severe distortion of vessel availability and trade patterns caused by the dual-sided blockade of the Strait of Hormuz. The combination of physical transit restrictions, unresolved mine risk, elevated war risk premiums, and the absence of reliable freedom of navigation has effectively prevented a large share of the mainstream international tanker fleet from operating through the region. This has accelerated the reallocation of vessels from the Gulf toward the Atlantic Basin, reinforcing the role of the US Gulf as a key marginal supplier, particularly into Asia, and driving a substantial increase in tonne-mile demand as longer haul Atlantic routes replace disrupted Middle Eastern exports.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)