Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

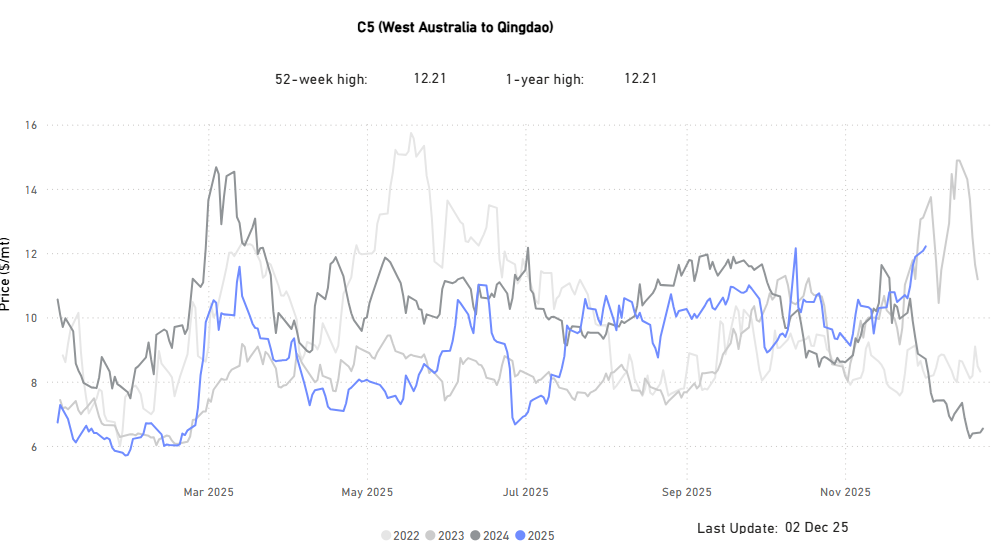

Market Insights | C5 Spikes to Year-High, Matching 4Q23 Peak

Rising Australian ore loadings keep upward pressure on WA–China freight.

In our previous market insights, we explored the Simandou iron ore story and whether it could meaningfully challenge the long-standing dominance of Australian and Brazilian exporters. This week, we shift focus to Western Australia’s iron ore dynamics behind the recent strength in the C5 freight route assessment. With year-end approaching, we review how shipment volumes have evolved and whether Q4 is on track to deliver a firm close for Australia’s iron ore industry.

C5 assessments have climbed back to the peak levels last seen in 4Q23, the highest in nearly a year.

The momentum from October carried straight into November. Even with the Australian cyclone season beginning in November and running through April, and with no cyclone disruptions so far, sentiment remained firm.

Chinese demand remains a key driver: despite the drag from the property sector, iron ore imports continued to rise through October and November, with Port Hedland at the forefront of the increase.

Iron ore stockpiles across China’s 45 major ports (tracked by Mysteel) increased by 1.6 million tonnes, or 1%, in the week of Nov 21–27, reaching 152.1 million tonnes, the highest level in nine months and 1% above last year’s level, marking the first year-on-year increase since mid-April.

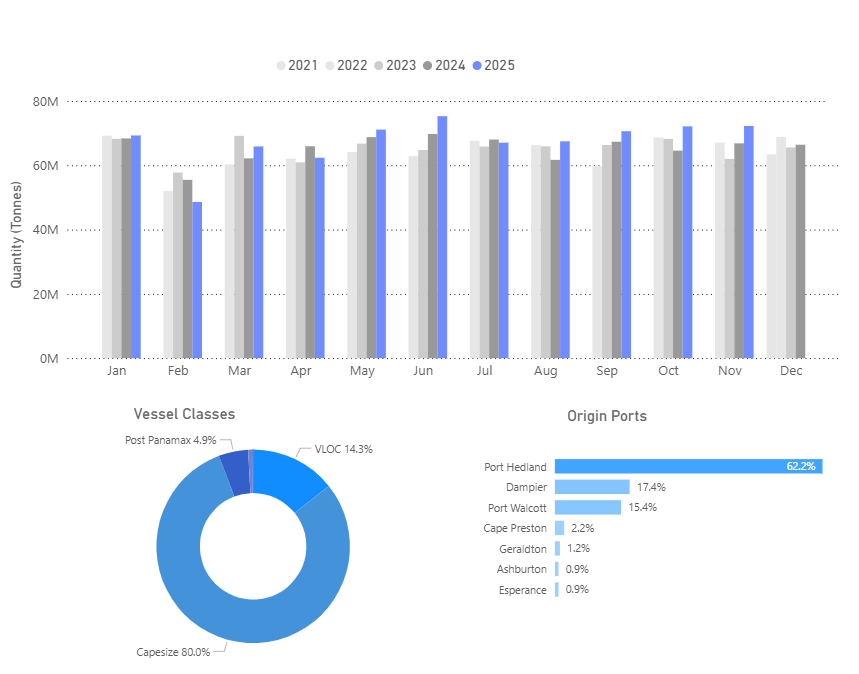

Spotlight on West Australian Iron Ore Flows | China

Seasonal High: China’s Iron Ore Intake from Western Australia exceeded 70M mt in Q4

The strong sentiment from October continued into November, with the early start of Australia’s tropical cyclone season not yet impacting the market. Chinese iron ore imports increased through October and November despite ongoing pressure from the property sector. Export volumes from Port Hedland were also firm, confirming that Western Australia’s shipments held up well ahead of the main cyclone months. Looking ahead to the November–April period, weather-related risks could affect export activity, while wider economic challenges will continue to weigh on Chinese iron ore demand.

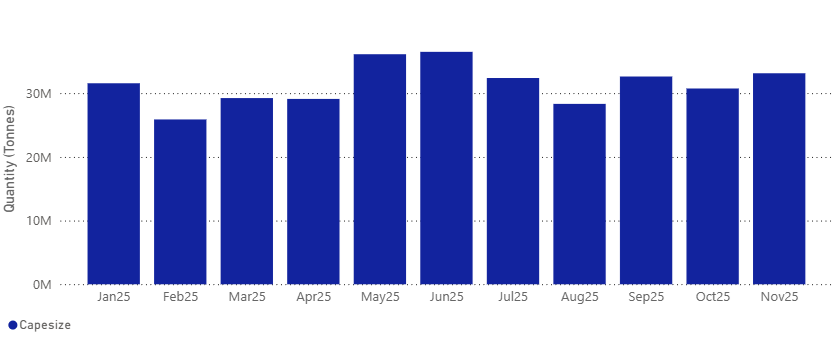

Port Hedland | Capesize Iron Ore Exports to China Exceeded 33million metric tonnes in November

In November, Port Hedland’s Capesize iron ore shipments to China climbed past 33 million metric tons, coming close to the May high of more than 35 million tons. Dampier and Port Walcott added meaningful volumes as well, but Port Hedland remained dominant, representing over 60% of Western Australia’s total exports to China.

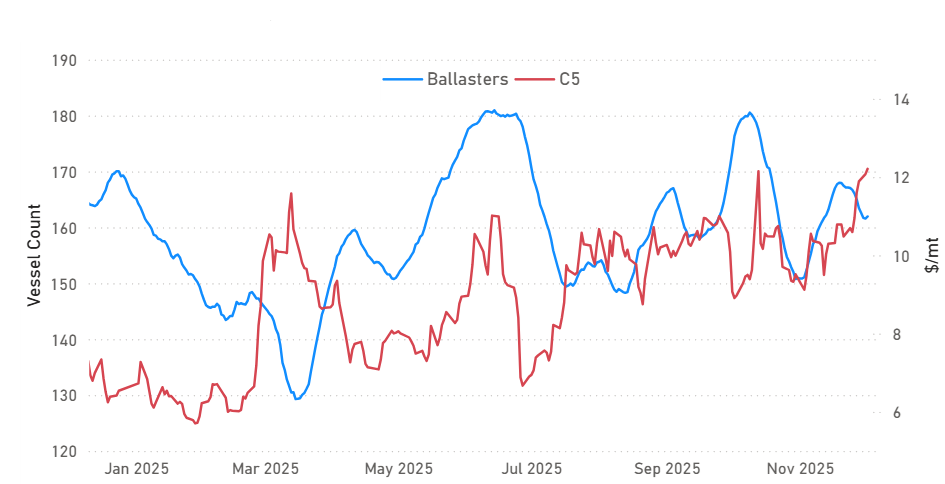

Ballasters Vs C5 Rates

Ballaster availability has tightened, with the 21D MA dropping to 162 vessels

Ballaster numbers have retreated significantly from their early-October peak of roughly 180 vessels to around 160 by late November. This decline aligns with the pick-up in iron ore loadings out of Western Australia, which has helped absorb the excess tonnage. The tighter vessel supply, together with stronger export flows, has supported firmer C5 sentiment, with rates rising from around $10/mt in early October to approximately $12/mt by late November.

Pilbara Infrastructure Keeps the Flow Moving

Western Australia’s iron ore export capacity remains well supported by ongoing investment and operational improvements.

Pilbara miners continue to upgrade and digitalise their supply chains, from Rio Tinto’s US$733m West Angelas investment to recent AI-driven rail efficiency gains, strengthening the underlying infrastructure that enables stable production and shipment capability. While the official cyclone season is underway and weather risks remain, these developments point to a robust export system. Combined with the firm shipment levels seen in recent months and steady Chinese offtake, the increased flow of cargoes from Western Australia has helped absorb ballasters and supported the firmer sentiment observed in the C5 market.

Q1 26: Short-Term Downside Risks

The C5 market is entering the most weather-disrupted phase of the year, when even brief cyclone-related outages at Port Hedland or Dampier can materially derail cargo programs and impact vessel availability in the Pacific. At the same time, deteriorating steel mill margins and ongoing output restrictions in China raise the likelihood of a near-term slowdown in iron ore intake, particularly if mills prolong production cuts or defer restocking.

Overall, in the absence of a meaningful rebound in downstream steel demand or consistently robust Pilbara export performance, the sustainability of the recent C5 upswing appears increasingly challenged heading into early Q1.

Use Signal Ocean’s Voyage Details to spot emerging signals and stay ahead of shifts in the oil world. For more insights, please contact our team. Stay ahead of the curve. Get access to the Signal Ocean Platform.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)