drives these stories

Special Focus: Supramax & Panamax Coal Cargo Flow Trends from Indonesia

In 2025, Indonesia’s role as a key supplier of Supramax and Panamax coal cargoes is under pressure due to shifting energy trends in Asia. China and India, the two largest buyers of Indonesian coal, are reducing their reliance on coal-fired power by increasing domestic coal production and accelerating investment in renewable energy. These developments are reshaping the seaborne coal trade trends and challenging Indonesia’s export dominance. In response, Signal Ocean partnered with Carbon Research Pte Ltd. to host the Jakarta Coal Workshop in July, featuring Rodrigo Echeverri, Senior Bulks Markets Analyst. His data-driven presentation highlighted the mounting challenges for Indonesian coal exporters and freight market participants. Key insights focused on slowing industrial activity across Asia, rising protectionist measures, including the lingering effects of Trump-era tariffs, and Southeast Asia’s increasingly strategic role in shaping regional coal demand.

Rodrigo Echeverri, Carbon Research - Speaking at the Signal Ocean Jakarta Coal Forum

Rodrigo Echeverri, Carbon Research - Speaking at the Signal Ocean Jakarta Coal Forum

A central theme of the workshop was the divergence of Indonesia’s export patterns from historical norms. High-calorific-value coal from Australia, Colombia, and South Africa is gaining market share in specific regions, while Indonesian cargoes are becoming more vulnerable to short-term policy changes and macroeconomic volatility. Participants also examined how vessel supply-demand balances are shaping freight dynamics, including rising tonne days, port congestion at Indonesian loading terminals, and the impact of Red Sea disruptions on key waypoints such as the Cape of Good Hope and the Suez Canal.

These freight and trade developments are closely linked to broader macroeconomic trends across Asia. India, in particular, has emerged as a key driver of regional demand, supported by sustained economic growth, robust infrastructure investment, and a strong manufacturing sector. Its manufacturing Purchasing Managers’ Index (PMI) surged to a 17-year high of 59.2 in July 2025, while manufacturing output rose by 3.9% year-on-year in June. However, this momentum has been partially offset by contractions in the mining and electricity sectors, which have weighed on overall industrial performance.

In contrast, China is facing growing economic strain. The official manufacturing PMI declined to 49.3 in July, marking the fourth consecutive month of contraction. Second-quarter GDP growth also slowed to 5.2%, down from 6.3% a year earlier, well below the double-digit rates of previous decades. China’s industrial structure is gradually shifting away from traditional heavy industry toward high-tech manufacturing, such as electrical equipment and electronics, which are less coal-intensive. Coupled with rising domestic production and a growing share of renewable and nuclear power, this transition has sharply reduced China’s demand for thermal coal imports.

Elsewhere in Asia, similar headwinds are at play. In South Korea, the June PMI edged up to 48.7 but remained below the neutral 50 threshold, signaling the fifth straight month of contraction. Industrial growth was modest at 3.6% year-on-year in the first quarter of 2025, with recent indicators suggesting only a mild recovery in the second quarter. Indonesia’s manufacturing sector has struggled, with the June PMI falling to 46.9, reflecting one of the steepest contractions in the region. This weakness is linked to softening domestic demand and weak export orders, despite manufacturing output growing by approximately 4.3% in the first quarter. Vietnam presents a mixed picture: although the country recorded over 9% manufacturing growth in Q1, recent PMI data points to moderating demand, particularly in exports. Taken together, these regional dynamics are beginning to weigh heavily on energy consumption patterns, particularly for coal-fired electricity.

China and India reshape the coal map: Domestic growth meets renewable momentum

In China, coal production continued to rise steadily in the first half of 2025, extending the growth momentum seen earlier in the year. Output increased modestly on a year-on-year basis, with May recording one of the strongest monthly gains, reflecting stable demand from the power and industrial sectors. At the same time, coal imports dropped sharply, with declines deepening into double digits by late spring. This trend reflects the growing availability of lower-cost domestic supply and a structural shift toward renewables, which have increasingly displaced imported thermal coal in the energy mix. Despite accelerating investment in clean energy, China expanded its coal-fired power fleet, adding nearly 70 gigawatts of new capacity in 2024, the highest annual total since 2015. However, these additions are primarily designed to support grid reliability and serve as a flexible backup to intermittent solar and wind power, rather than to fuel a renewed surge in coal consumption. In July 2025, China also broke ground on the world’s largest hydropower project on the Yarlung Zangbo River in Tibet, a five-station cascade expected to generate around 300 billion kilowatt-hours annually, reinforcing the country’s push to expand renewable capacity and reduce reliance on fossil fuels.

Read more at AXSMarine:Asia, Africa, Europe: Where Is Steam Coal Demand Growing?

India is following a similar trajectory. National coal production exceeded 1 billion tonnes in FY 2024–25, and the government plans to boost output to about 1.5 billion tonnes by 2029–30, aiming for an annual growth of 6–7%. Coal India Ltd (CIL) targets reaching a production milestone of 1 billion tonnes by FY 2026–27, after producing a record level in FY 2024–25. Coal-fired generation decreased sharply in May 2025, marking the largest yearly decline since 2020, despite rising overall energy demand. India’s dependence on coal imports also continued to decline. While coal imports increased during certain months, such as July and October 2024, the overall total for FY 2024–25 declined compared to the previous year. Imported coal now accounts for a shrinking share of overall consumption. Meanwhile, India’s renewable energy capacity continues to grow steadily, with a substantial addition over the past year. Although coal still dominates the electricity mix, current government plans focus on expanding renewable sources, with most new coal capacity projects already under construction. Nevertheless, some long-term forecasts still include new coal plants through 2030. The share of coal in power generation is projected to decrease significantly by 2030 and further by 2047. To help ensure short-term supply security, CIL is reopening inactive coal mines and launching new sites, though this increase does not alter the overall trend toward reduced reliance on coal.

Demand shifts in China and India threaten Supramax and Panamax trade flows

Supramax and Panamax vessel utilization, historically supported by steady flows to China and India, may come under pressure as both countries increase domestic coal production and gradually expand their use of cleaner energy sources. In this scenario, Indonesia would need to reconsider its export strategy.

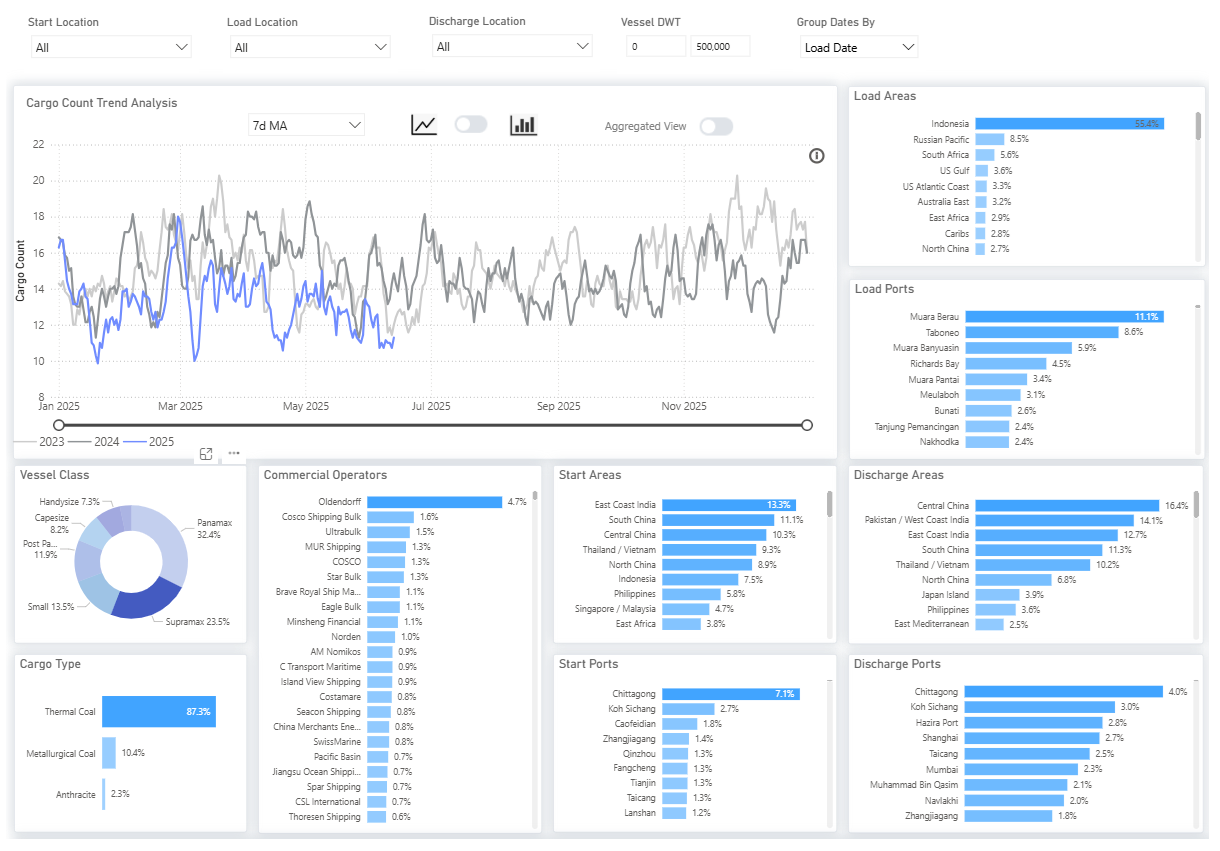

In 2025, Indonesia accounted for 54% of all coal load areas, far outpacing other exporters. This dominant share highlights the country’s central role in the Panamax and Supramax coal markets, which are particularly sensitive to changes in Asian coal demand.

https://app.signalocean.com/dry/dynamic/voyages-dashboard-dry

https://app.signalocean.com/dry/dynamic/voyages-dashboard-dry

Supramax and Panamax vessels together account for over 85% of tracked coal shipments, highlighting their dominant role in transporting Indonesian exports and reflecting the scale and operational structure of the country’s coal logistics. The cargo type breakdown shows that 87% of all shipments are thermal coal, indicating a high level of exposure to the energy policies and consumption trends of key buyers such as China and India.

At the port level, Indonesian terminals like Muara Berau (11%), Taboneo (8%), and Muara Banyuasin (6%) rank among the top coal load ports. However, these shipments are heavily concentrated toward a few discharge regions. Central China (16.4%), Pakistan/West Coast India (14.1%), East Coast India (12.7%), and South China (11.1%) make up the largest destination areas, demonstrating the critical dependence of Indonesian exports on these markets. With both India and China increasing domestic coal output and accelerating renewable energy adoption, structural demand risks are mounting.

The cargo count trend for 2025 shows a visible decline compared to 2023 and 2024, suggesting a reduction in voyage activity. This observation is consistent with the key takeaways from the Signal Ocean Jakarta Coal Workshop in July, which emphasized weakening coal-fired power demand in China and India, as well as a regional slowdown in industrial production.

As coal demand from China and India declines, Indonesia faces mounting pressure to diversify its exports, adopt cleaner technologies, and realign its policy priorities.

In response, the government is actively pursuing new markets and investing in higher-value coal derivatives, such as gasification and briquettes. According to Indonesia’s Ministry of Energy and Mineral Resources (MEMR), there is a growing emphasis on expanding coal exports beyond traditional buyers.

MEMR reports and trade data point to increased shipments to emerging markets, including Vietnam, the Philippines, Bangladesh, and destinations in the Middle East and Africa. However, these alternative buyers are generally smaller in scale, more price-sensitive, and subject to more volatile demand, which constrains their ability to fully replace the potential decline in export volumes to China and India, Indonesia’s two largest coal import partners.

The government is also working to align coal policy with domestic energy transition goals, including greater integration of renewables and the adoption of cleaner coal technologies. Still, this shift poses a significant policy challenge: balancing export revenues and economic security with the long-term imperatives of decarbonization and energy transition.

Indonesia’s thermal coal sector is entering a pivotal phase. The dual forces of rising domestic coal output in China and India, alongside their accelerating shift toward renewable energy, are steadily reducing traditional seaborne coal demand. For Indonesia, this signals the onset of a critical transition, one that demands strategic rebalancing, export diversification, and investment in future-proof energy solutions to maintain its role in the global energy landscape. How Indonesia adapts to these evolving conditions will shape the future trajectory of coal trade flows across Asia and beyond.

Request a Signal Ocean Demo

Stay updated with platform enhancements, insights, and market analysis. For demo inquiries, reach out to request a Signal Ocean demo and visit the Signal Ocean Newsroom for the latest updates on market trends and platform developments. To check out our previous newsroom article click here.

Ready to get started and outrun your competition?

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)