Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Panamax Supply Outlook as Hormuz Faces Strain | Market Insights

The ongoing uncertainty surrounding the Strait of Hormuz is impacting the Panamax dry bulk segment. According to recent media reports, a potential two-week extension to ceasefire discussions is under consideration, although this remains unconfirmed at the official level.

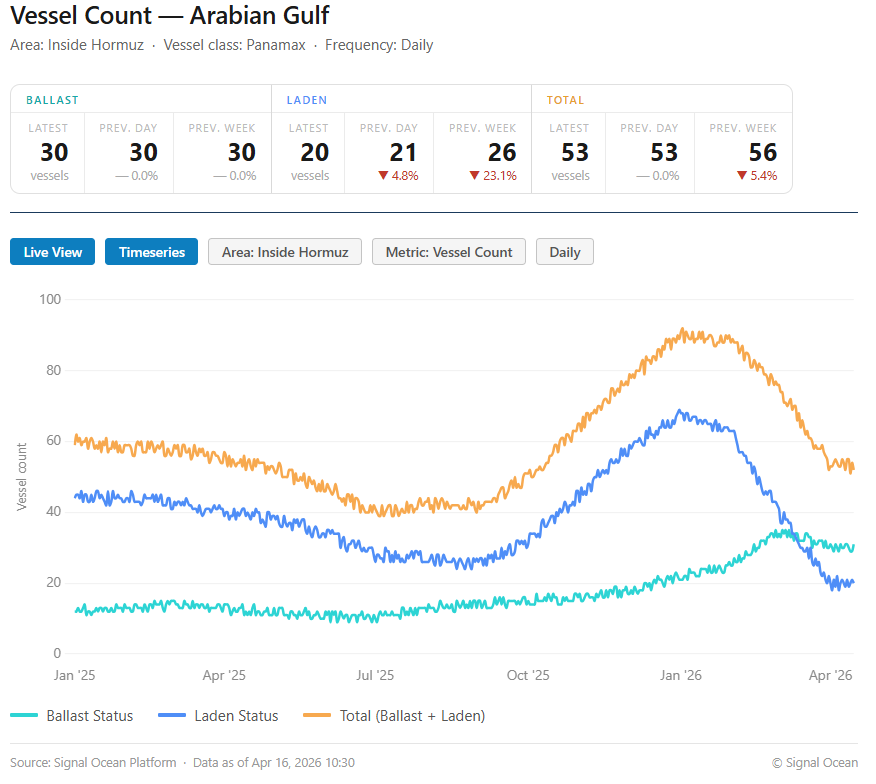

In this context, Signal Ocean data show that the number of Panamax vessels in ballast condition within the Strait has remained stable at around 30 (as shown in the chart below), while laden vessel counts have declined sharply from late-February highs. This divergence points to emerging delays in loading or transit for vessels operating in the region amid ongoing disruptions.

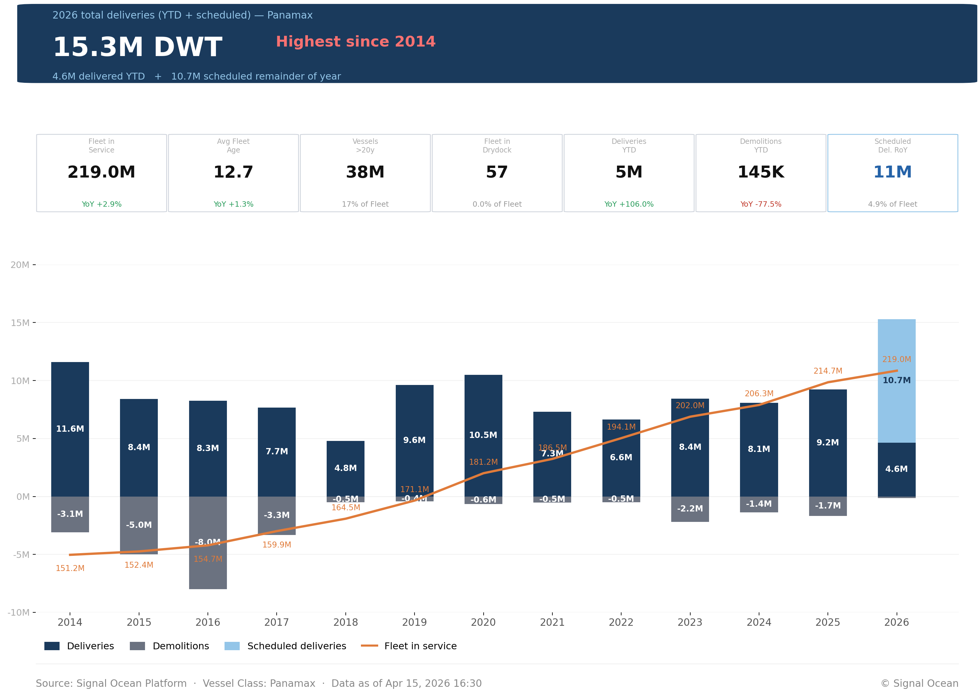

Scheduled Vessel Deliveries Highest since 2014

Panamax vessel deliveries are projected to reach a record high in 2026, with approximately 15 million dwt of new capacity entering the market, up from roughly 10–11 million dwt in the prior year. This expansion is expected to push the global dry bulk fleet near 220 million dwt, reinforcing a clear supply-side growth cycle.

This increase in fleet capacity is taking place against a plateauing outlook for coal demand. According to projections in the IEA's Coal Mid-Year Update (July and December 2025), global coal demand was expected to reach a record ~8.85 billion tonnes in 2025, before edging slightly lower in 2026 and stabilising near ~8.7–8.8 billion tonnes.

Coal Demand Outlook: Policy Shifts and Market Pressures

Energy Mix Trends

The latest coal demand trend reflects structural changes in the global energy mix, particularly in China and India, which together account for the majority of consumption. While both countries are expanding renewable capacity at scale, coal continues to play a central role in energy security. This is resulting in a dual-track approach, combining ongoing coal utilisation for system stability with continued investment in renewables.

China Market Dynamics

In China, recent developments point to a gradual shift. While earlier data indicated a slowdown in coal plant approvals, geopolitical developments have reinforced coal’s role as a reliability buffer. At the same time, policymakers continue to advance a broader transition toward renewables and nuclear power. Domestic coal production remains a priority, limiting incremental import demand.

India Market Dynamics

In India, policy has moved more decisively toward reducing reliance on seaborne coal. The government is targeting an approximate 30% reduction in thermal coal imports in 2026, replacing imports with increased domestic production. At the same time, coal-fired plants are being operated at full capacity during peak demand periods, indicating higher utilisation without a corresponding rise in imports.

Short-Term Drivers

Recent geopolitical developments in the Middle East have introduced short-term volatility into energy markets, tightening gas supply and prompting temporary fuel switching toward coal in some regions. At the same time, these developments are accelerating investment in renewables and broader energy security measures.

Demand Outlook

If disruptions to energy markets persist, coal demand could see modest short-term support, potentially offsetting part of the expected decline in 2026. However, policy direction in major consuming countries suggests that any increase is likely to remain cyclical rather than structural, with long-term demand stabilising rather than returning to sustained growth.

Will Vessel Orders Surge Continue…?

Geopolitical tensions in the Middle East are likely to keep Asian buyers focused on energy security, slowing efforts to reduce reliance on coal imports. This may lend some short-term support to coal demand, although the broader trend still points to a more stable, rather than growing, demand profile as the energy transition continues.

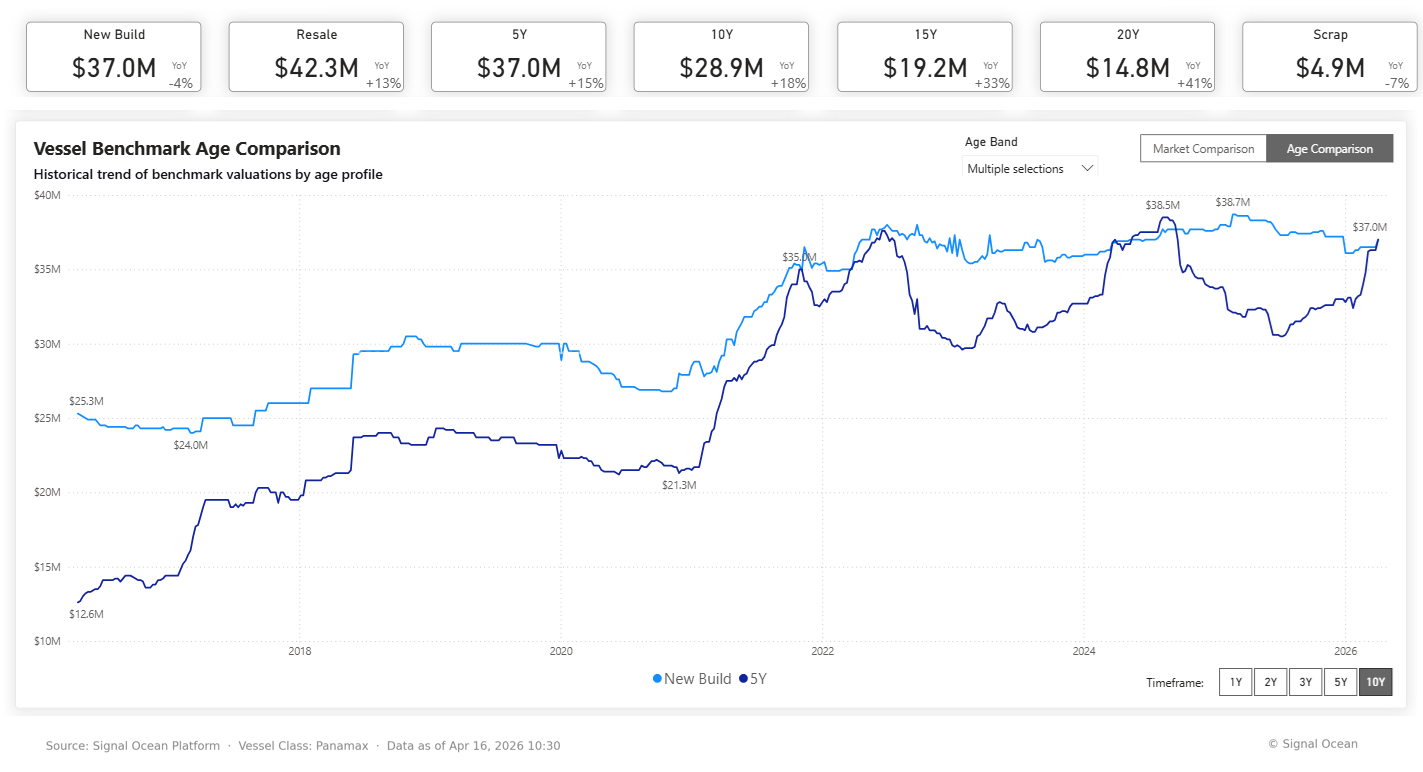

At the same time, newbuilding prices have recently moved in line with second-hand values, with a 5-year-old Panamax bulker valued at approximately USD 37 million. This shift may begin to support newbuilding orders relative to second-hand purchases, although ordering activity remains sensitive to geopolitical market conditions.

Against this backdrop, the key question remains whether the recent momentum in orders can be sustained, as the market continues to watch oil prices, potential supply disruptions, and ongoing uncertainty around bunkering in the Arabian Gulf.

Maria Betzeletou, Senior Market Analyst - Signal Ocean

All data, estimates, and projections presented herein are based on information available as of [April 16, 2026]. While every effort has been made to ensure accuracy, the analysis is subject to revision as additional information becomes available.

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)