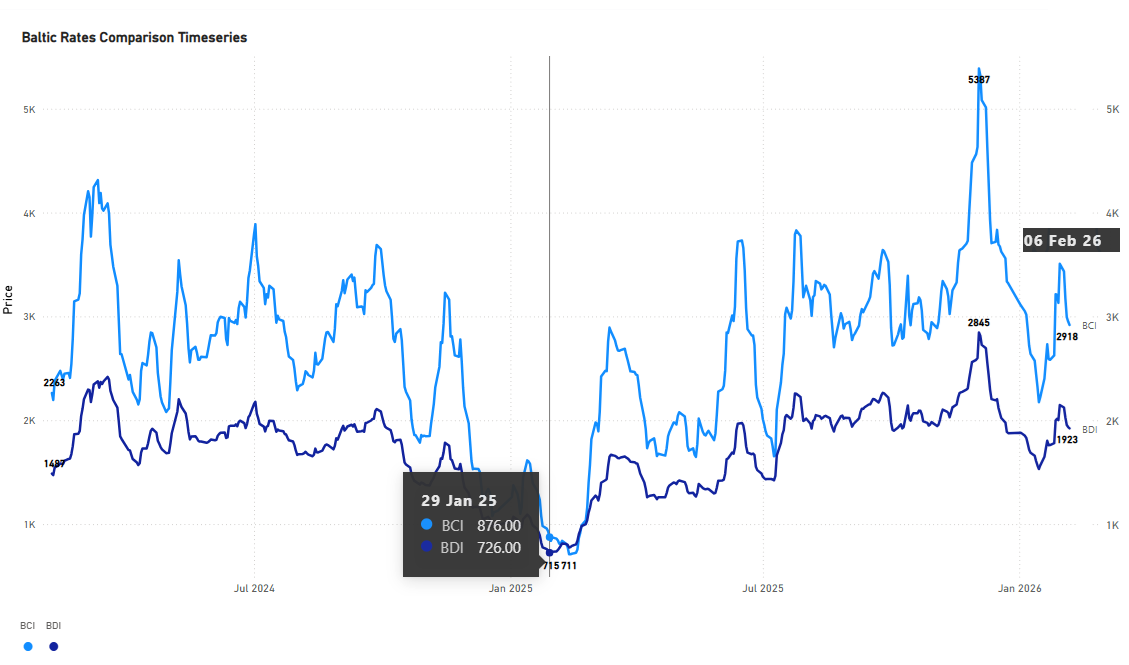

The Baltic Dry Index (BDI) recorded a sharp recovery ahead of the Lunar New Year before correcting on Friday, 6 February 2026. While dry bulk indices have historically softened into the holiday period due to seasonal disruptions, index levels this year remained firmer than at the start of 2025.

Index Performance

The BDI closed on 6 February at more than double its level on Chinese New Year 2025 (29 January). A comparison between the BDI and the BCI confirms that Capesize vessels were the main contributors to the index’s strength. The continued firmness was largely driven by steady iron ore flows and China's prevailing steel production mix.

Seasonal Context

Attention is focused on the late timing of the 2026 Lunar New Year, which falls on February 17th. Historically, the holiday has fallen after 10 February roughly once every three to four years, while particularly late occurrences around 19–20 February are observed about once per decade. The most relevant historical comparison is 2015, when the Lunar New Year fell on 19 February, and the BDI reached multi-decade lows (approx 500 points). That downturn was triggered by a sharp contraction in vessel demand, severe fleet oversupply following heavy newbuilding deliveries between 2008 and 2014, and record-low Chinese imports.

China and Iron Ore

Industry focus remains centered on the Chinese steel sector, where iron ore prices have shown signs of softening amid ample supply relative to demand. Despite this, the outlook is not expected to turn decisively bearish. Available data indicate that the 2025 decline in Chinese crude steel production was not concentrated in electric arc furnace output, which would otherwise have led to a sharper reduction in iron ore demand. While further pressure on steel production is anticipated in 2026, the prevailing production mix is expected to remain supportive of iron ore-based steelmaking.

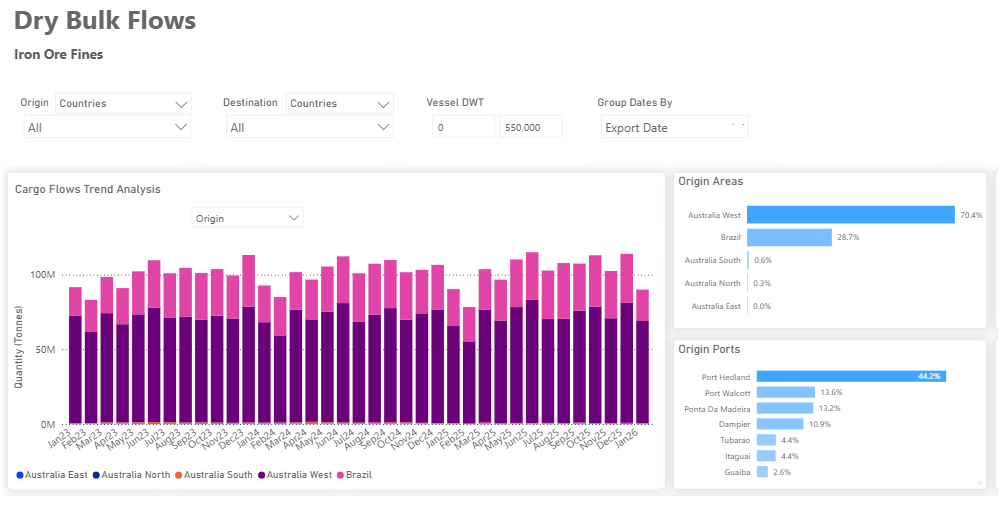

Iron ore trade flows continue to be supported by almost steady annual volume growth of shipments from Australia and Brazil (3.8bn total quantity tonnes in the period 2023-ytd), alongside initial cargoes from Guinea’s Simandou project, which reached China in December 2025 and January 2026. Although iron ore prices traded below USD 100 per tonne in the run-up to the holiday period, current levels reflect softer demand rather than a collapse.

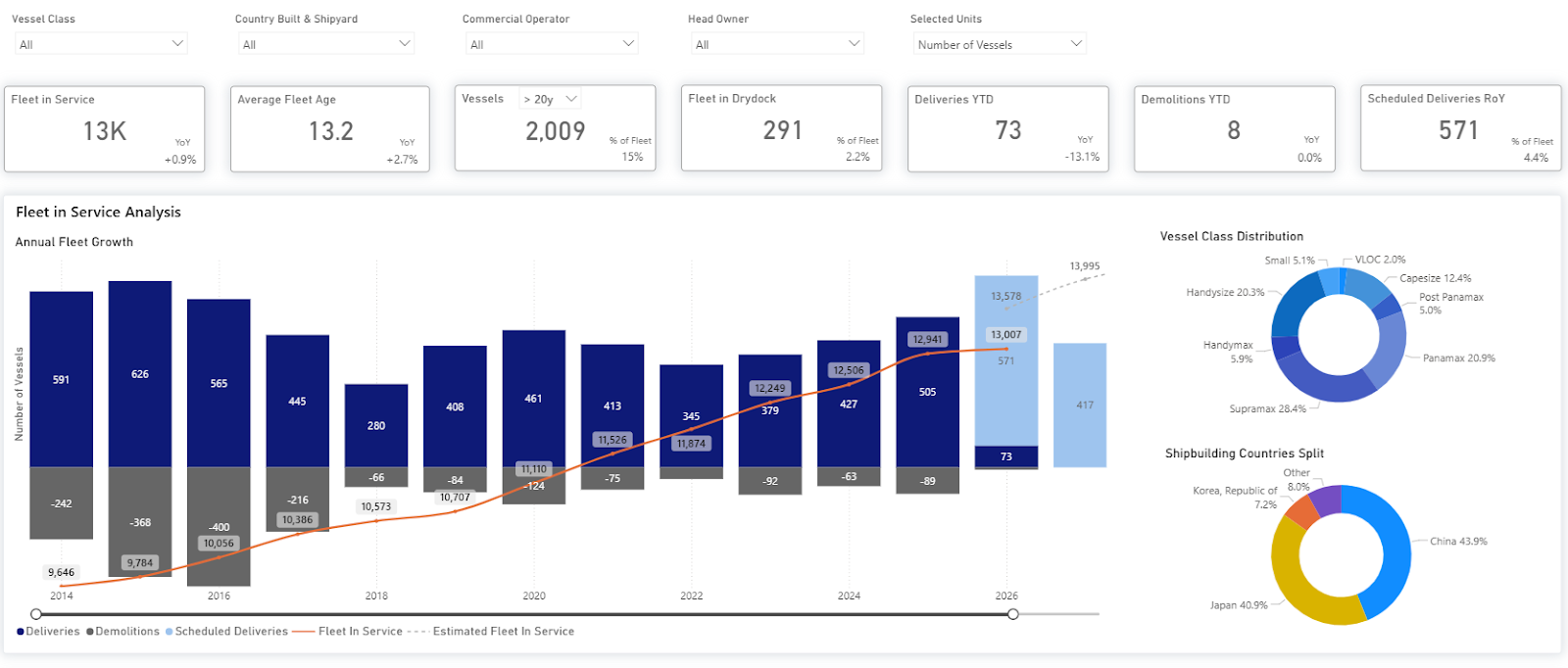

Fleet supply dynamics remain a key risk factor. In early 2015, freight rates collapsed amid an unprecedented surge in vessel deliveries. While scrapping activity has remained limited and the dry bulk fleet continues to expand, scheduled vessel deliveries have remained below 2014–2016 levels. Current conditions, therefore, do not mirror the wave of vessel deliveries that characterized the 2015 market collapse, when the fleet in service grew rapidly, surpassing 10,000 vessels.

The dry bulk market enters the 2026 Lunar New Year period with stronger momentum than in previous late-holiday cycles. Capesize earnings continue to provide meaningful support to the BDI, while iron ore trade flows remain supportive despite moderating steel demand growth. Elevated port inventories, ongoing fleet growth, and anticipated pressure on Chinese steel output in 2026 warrant close monitoring, with the post-holiday period expected to provide clearer signals on the durability of current rate strength.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)