Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Strait of Hormuz | From Vital Energy Chokepoint Point to Pressure Point The sustained tensions since Saturday continue to diminish the prospects for de-escalation.

Tensions around the Strait of Hormuz are increasingly spilling into global oil markets, raising concerns about potential disruptions to one of the world’s most critical energy transit routes. As regional tensions evolve, the central question for markets is no longer whether disruptions may occur, but how long they could persist.

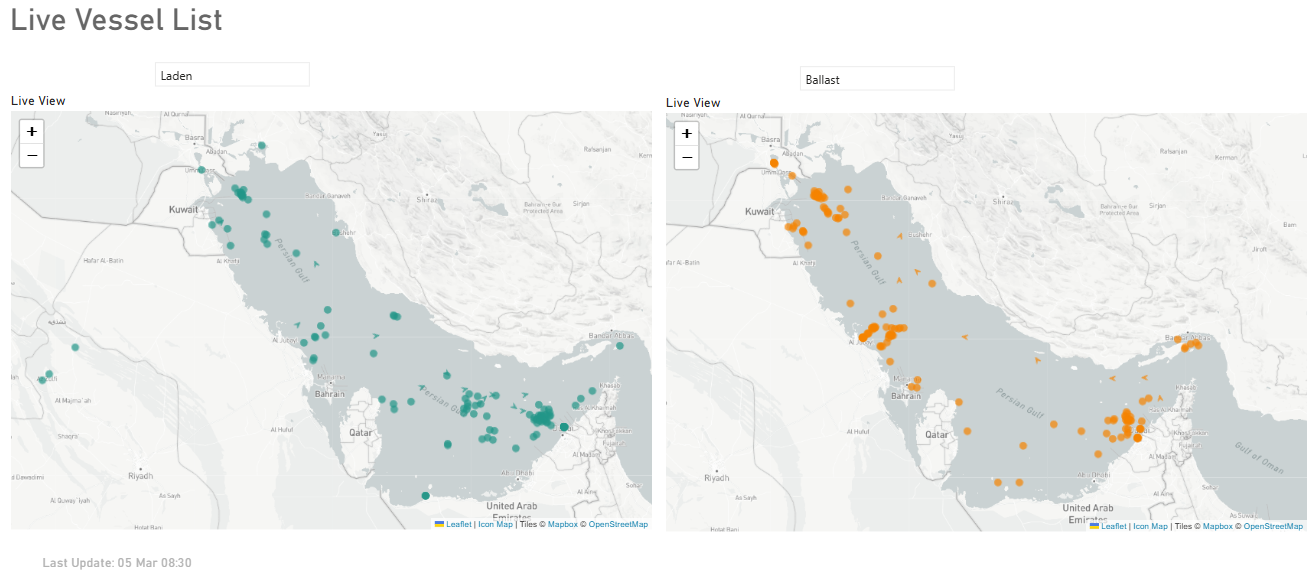

Major Asian importers appear particularly exposed. China and India remain heavily dependent on Gulf crude supplies, although India has indicated that national inventories could cover approximately 40–45 days of demand. Russia is expected to increase oil exports to both countries, which may partially offset any sustained disruption to Gulf shipments.

At the same time, the maritime risk environment in the Gulf is tightening. Marine insurers have issued notices regarding war-risk coverage for vessels operating in the region, with changes reportedly taking effect from 5 March 2026. Marine insurance brokers indicate that war-risk premiums have increased sharply, in some cases by 50–100%.

According to reports in Iranian state media, Iran's Islamic Revolutionary Guard Corps has announced a ban on the transit of vessels linked to the United States, Israel, Europe, and other Western allies through the Strait of Hormuz. In response to this tension, China has urged de-escalation. Furthermore, regional players such as the United Arab Emirates and Qatar are reportedly promoting diplomatic initiatives to avert a sustained interruption of regional trade and energy exports.

Taken together, these developments point to a rapidly evolving risk environment in the Strait of Hormuz, where geopolitical tensions and rising insurance costs may increasingly shape vessel movements through one of the world’s most strategically important shipping corridors.

What We Know So Far

The Strait of Hormuz has long been central to geopolitical tensions affecting global oil markets. While the Strait has never experienced a prolonged closure, periods of escalation have historically influenced shipping costs and operational conditions across the Gulf. What makes the current situation notable is that market indicators began adjusting even before the escalation resulted in confirmed disruption.

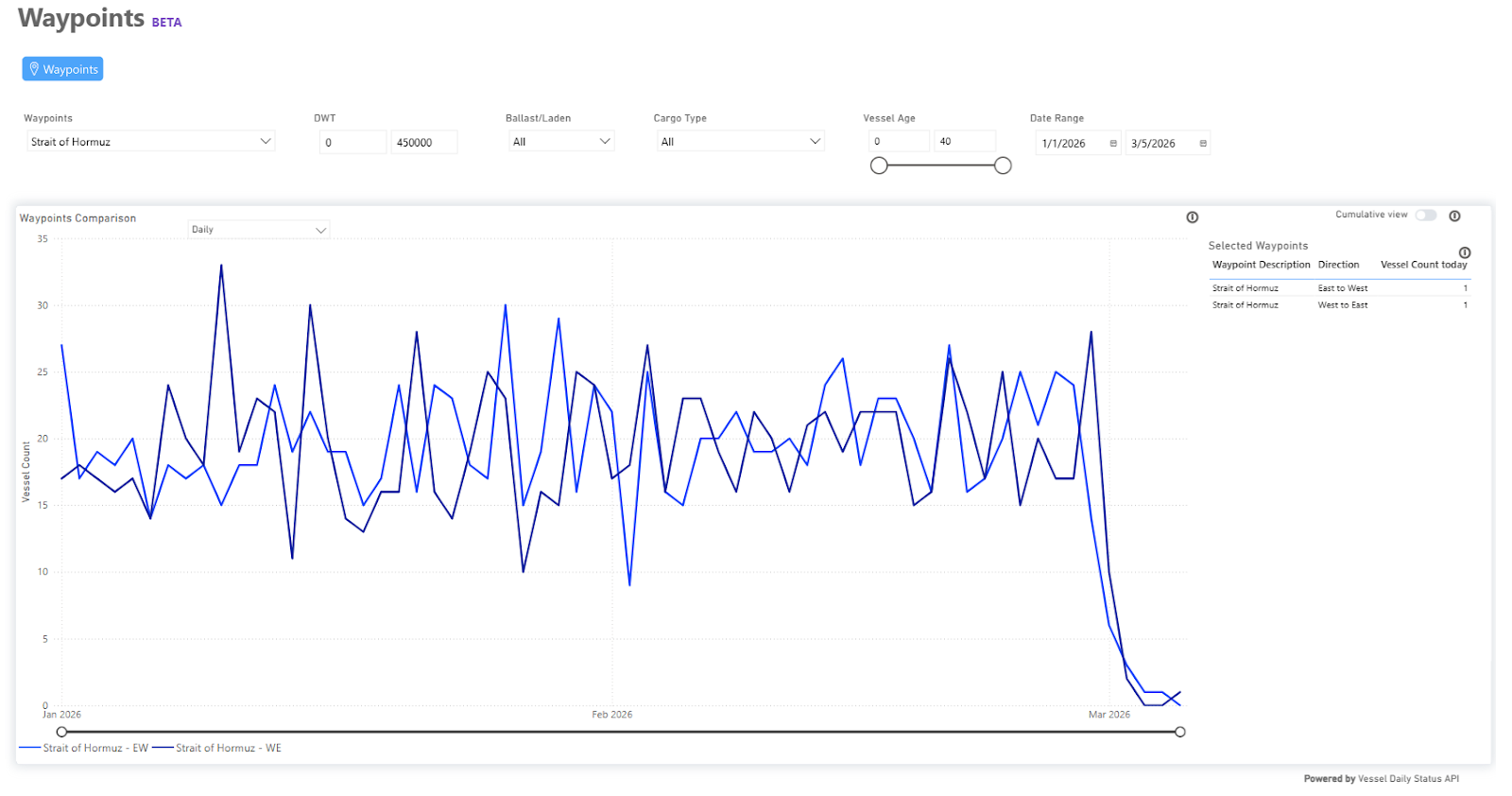

Ship traffic has nearly stopped in the Strait of Hormuz

Based on TSOP AIS vessel tracking data, daily crossings through the Strait of Hormuz declined sharply in early March to near zero.

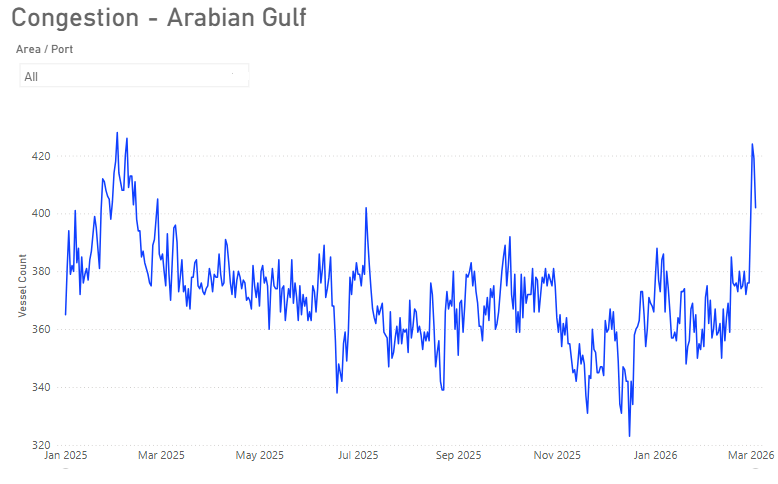

Security disruptions in the Strait of Hormuz appear to be pushing up Arabian Gulf port congestion, which increased by ~7% between 27 February and 4 March 2026.

The path of oil prices will largely depend on how long the disruption lasts.

If tensions ease within about a week, Brent crude could stabilize in the $80–$90 per barrel range before gradually retreating toward $70 as the geopolitical risk premium fades.

If disruptions persist for several weeks, supply could tighten, and Brent may move above $100 per barrel as inventories decline and refiners seek alternative barrels. In a prolonged disruption scenario, Brent prices could move well above $100, with some industry estimates pointing toward $120 per barrel. Export bottlenecks could force production cuts across the region as storage facilities fill and logistics become increasingly strained. A disruption lasting around twenty-five days could turn market volatility into a more structural supply shock.

What’s Next

At this stage, the central question across the industry remains straightforward: is the Strait of Hormuz actually closed, and what would that mean in practice? From a legal standpoint, the strait has not been closed, and no official announcement or navigation notice has been issued suspending transit. Operationally, however, the situation can look very different. When security risks rise, crews become reluctant to sail in the area, and war-risk insurance is restricted or withdrawn, the strait can effectively become extremely difficult to use, even if it technically remains open.

Based on current data, the duration of the disruption remains uncertain. A prolonged crisis scenario currently appears less likely, as an extended interruption would place increasing pressure not only on the major import-dependent economies of Asia but also on Gulf economies. In response to potential disruptions in the Strait of Hormuz, Saudi Aramco has already activated contingency measures, including the use of its Red Sea export route via Yanbu to bypass the strait. In any case, shipping has already experienced one of the most significant disruptions in recent decades, and even if tensions ease, it may take time before normal conditions in maritime transport are fully restored.

All data, estimates, and projections presented herein are based on information available as of [March 5, 2026]. While every effort has been made to ensure accuracy, the analysis is subject to revision as additional information becomes available.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)