Tanker Trade in Turbulence: Beijing Strikes Back with Port Fee Policy

China’s targeted port fee on U.S.-linked ships signals a sharper divide in global tanker trade.

drives these stories

Tanker Trade in Turbulence: Beijing Strikes Back with Port Fee Policy

As of October 14, 2025, the U.S. and China have implemented reciprocal port fees targeting vessels associated with the opposing nation. These fees are levied on a per-net-ton basis, determined by a vessel’s identity, specifically its ownership, operation, flag, or build, rather than its cargo. Initial market observations suggest selective rerouting patterns, a potential rise in tonne-mile demand, and increased compliance and verification costs as firms intensify due diligence on vessel ownership and flag to mitigate exposure to reciprocal port fees.

China’s special port fee

China’s new port-fee regulation, effective 14 October 2025, marks a targeted response to escalating U.S.–China trade frictions. The measure applies to vessels with a defined U.S. nexus, encompassing ownership, operational control, or equity participation of at least 25%, as well as vessels flagged or built in the United States.

The fee structure introduces a variable levy starting at RMB 400 per net ton in 2025, rising to RMB 1,120 by 2028, and applied at the first Chinese port of call per voyage. Each vessel is capped at five chargeable voyages annually. Owners or their agents must report vessel and ownership details seven days before arrival, with penalties for non-compliance including denial of port entry or clearance.

A critical feature of the policy is the exemption for Chinese-built vessels, even if they are owned or controlled by U.S. interests. This carve-out reinforces Beijing’s dual objective: to penalize U.S. maritime interests while incentivizing construction in Chinese yards and consolidating domestic industrial competitiveness.

From an operational perspective, the regulation introduces a structural cost asymmetry in the global shipping industry. U.S.-linked tonnage faces higher port costs and potential route adjustments, while non-U.S. or Asian-built vessels retain a relative advantage in China-bound trades. The policy thus sharpens the commercial segmentation of the fleet and may accelerate reflagging, corporate restructuring, or the redirection of vessel investments toward non-U.S. entities to preserve market access.

Exemptions Update

Following the “Announcement on Charging Special Port Fees for Ships to US Ships”, the Chinese Ministry of Transport announced implementation measures regarding the special port fees, including several critical exemptions.

According to the Notice, the following ships are exempt from paying the special port fees:

- Chinese-built ships

- Empty vessels that only visit Chinese yards for repairs.

- Other ships that are recognised and approved for exemption

No further elaboration has been provided at this time on the meaning of “Other ships that are recognised and approved for exemption”.

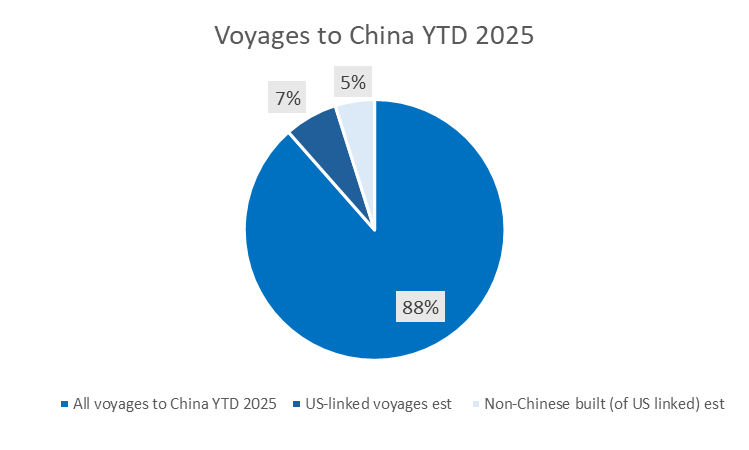

Limited Exposure: Few US-Linked or Non-Chinese-Built Tankers Trade Into China

Based on the below graph, Signal Ocean voyage data for the year-to-date 2025 indicate that US-linked vessels account for roughly 7% of all oil tanker voyages to China, underscoring that any proposed Chinese fees on US-affiliated shipping would have a limited overall impact on crude and product tanker flows. Within this subset, only about 5% of voyages involve non-Chinese-built tonnage, largely constructed in South Korea or Japan. These estimates are based on US-linked commercial operators with a minimum equity threshold of 25%, excluding US-flagged or US-built vessels, both negligible within this trade flow. As a result, roughly 88% of China-bound oil voyages would remain unaffected by such measures.

Data Source: Signal Ocean Voyages Data

Data Source: Signal Ocean Voyages Data

Even when breaking down the data by vessel class, the exposure remains limited across all segments, with only minor differences between the crude and product fleets:

- VLCC (YTD 2025, est.): Of an estimated 1,438 VLCC voyages to China, around 68 involved non-Chinese-built ships linked to US commercial operators, an exposure of approximately 5%. Despite VLCCs being the core carrier for Chinese crude imports, the policy reach here is narrow.

- Suezmax (YTD 2025, est.): With 139 voyages, only about 10 were non-Chinese-built and US-linked, around 7% exposure.

- Aframax (YTD 2025, est.): Among 829 voyages, 27 fall under the non-Chinese-built, US-linked category, just 3% exposure, the lowest among the dirty tanker segments.

- LR2 (YTD 2025, est.): From an estimated 63 LR2 voyages, 7 involved non-Chinese-built, US-linked vessels, about 11%, the highest proportional exposure, though the total volume remains modest.

- MR2 (YTD 2025, est.): Of 589 MR2 voyages, 57 were non-Chinese-built and US-linked, representing around 10% of MR2 calls, making it the largest affected group by count, though still a minor share of total product flows.

**Read more at AXSMarine:Tanker Market Tightens on MEG Liftings, OSP Cuts, and China Port Fees**

Emerging Exposure: Non-Chinese-Built Tanker Orderbook Points to Gradual Upturn in Potential Risk

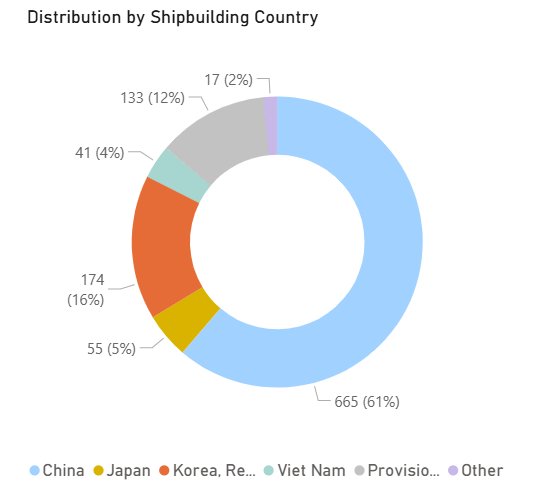

While the current exposure of US-linked or non-Chinese-built tankers trading into China remains limited, the forward outlook points to a gradual structural increase as new capacity enters the global fleet. This assessment focuses on the non-Chinese-built portion of the tanker orderbook, as these vessels could theoretically fall within the scope of China’s proposed measures if they are also US-linked, combining both foreign construction and commercial affiliation criteria.

According to Signal Ocean fleet data, about 39% of the global tanker orderbook is non-Chinese-built, with the remaining 61% under construction at Chinese shipyards. Within the non-Chinese segment, the largest shipbuilding centres are South Korea (16%), Japan (5%), and Vietnam (4%). These shipyards dominate foreign construction, meaning a large share of forthcoming deliveries could, by extension, fall under potential scrutiny if China’s policy targets foreign-built, US-linked tonnage.

https://app.signalocean.com/tanker/dynamic/orderbook_tanker

https://app.signalocean.com/tanker/dynamic/orderbook_tanker

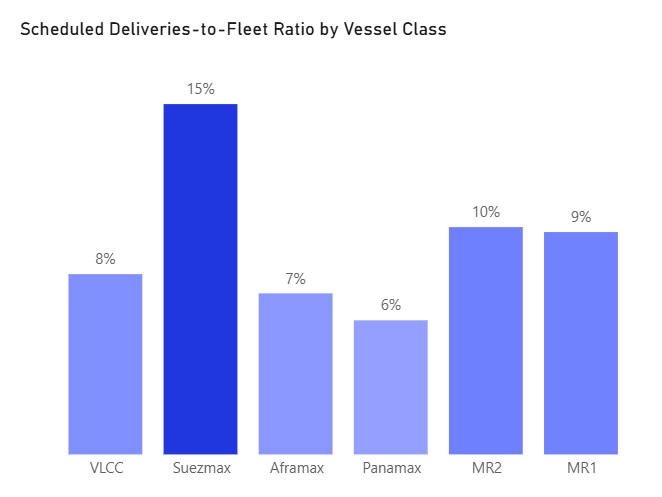

At the same time, the scheduled deliveries-to-fleet ratio, calculated for the non-Chinese-built portion of the global orderbook, highlights where upcoming exposure may concentrate. Suezmaxes show the highest renewal rate (15%), followed by MR2s (10%), MR1s (9%), VLCCs (8%), Aframaxes (7%), and Panamaxes (6%).

https://app.signalocean.com/tanker/dynamic/orderbook_tanker

https://app.signalocean.com/tanker/dynamic/orderbook_tanker

Looking ahead

The recent exemptions, particularly for Chinese-built vessels, offer a practical relief from the initial measures, alleviating concerns about widespread cost increases. This suggests that for most fleet operators, the overall financial exposure should remain manageable. However, this is contingent on careful oversight of vessel ownership structures and limiting direct U.S. affiliations. Consequently, the long-term impact of this policy is likely to be more administrative, emphasising prudent compliance rather than fundamentally altering trade flows.

Frequently Asked Questions

What is China's special port fee and who does it apply to? China's special port fee, effective October 14, 2025, applies to vessels with a U.S. nexus — defined as ownership, operational control, or equity participation of at least 25%, or vessels flagged or built in the United States. The levy starts at RMB 400 per net ton in 2025 and rises to RMB 1,120 by 2028.

Are Chinese-built vessels exempt from the fee? Yes. Chinese-built vessels are fully exempt, even if owned or controlled by U.S. interests. This exemption is a deliberate policy choice to incentivise construction at Chinese shipyards while penalising U.S.-linked foreign-built tonnage.

How much of the China-bound tanker trade is actually affected? Based on Signal Ocean voyage data for YTD 2025, US-linked vessels account for roughly 7% of oil tanker voyages to China. Of that subset, only about 5% involve non-Chinese-built tonnage. In total, approximately 88% of China-bound oil voyages remain unaffected.

Which tanker segments face the highest exposure? LR2s (11%) and MR2s (10%) show the highest proportional exposure among vessel classes, though both represent modest absolute volumes. VLCCs, which dominate Chinese crude imports, have just ~5% exposure — limiting the policy's overall market impact.

What should fleet operators do to manage compliance risk? Operators should review vessel ownership structures to identify any U.S. equity stakes above the 25% threshold, monitor reflagging and corporate restructuring options, and ensure agents submit required ownership disclosures at least seven days before arrival at a Chinese port.

Stay Ahead with Signal Ocean

Stay ahead of the curve. Get access to the Signal Ocean Platform. Stay updated with*****platformenhancements, insights, and market analysis. For demo inquiries,reach outto us and visit theSignal Ocean Newsroomfor the latest updates on market trends and platform developments. To check out our previous newsroom articleclick here.***

Ready to get started and outrun your competition?

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)