A data-driven review facilitated by the Floating Storage platform reportshows the seasonality of floating storage since 2022 across VLCC, Suezmax, and Aframax fleets, the surge in Iranian-linked storage off Malaysia, and future outlooks marked by persistent oversupply risks and declining oil price estimates.

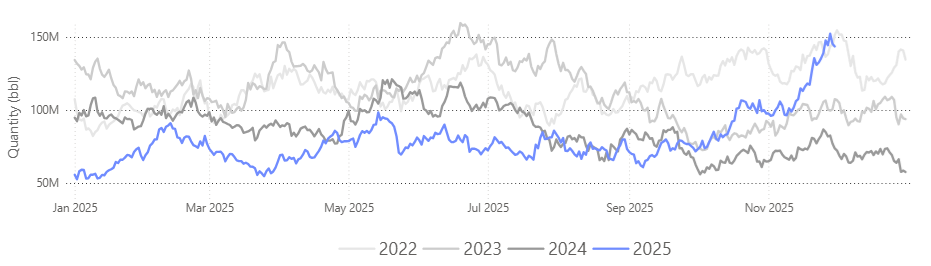

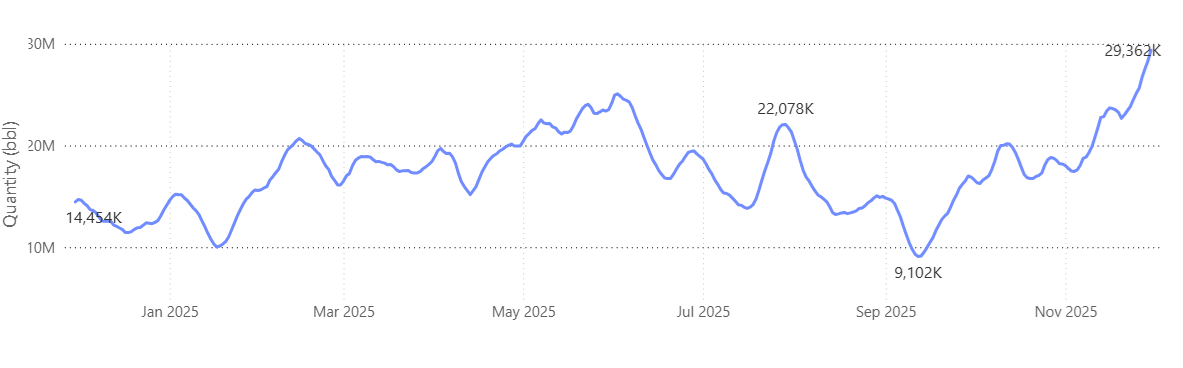

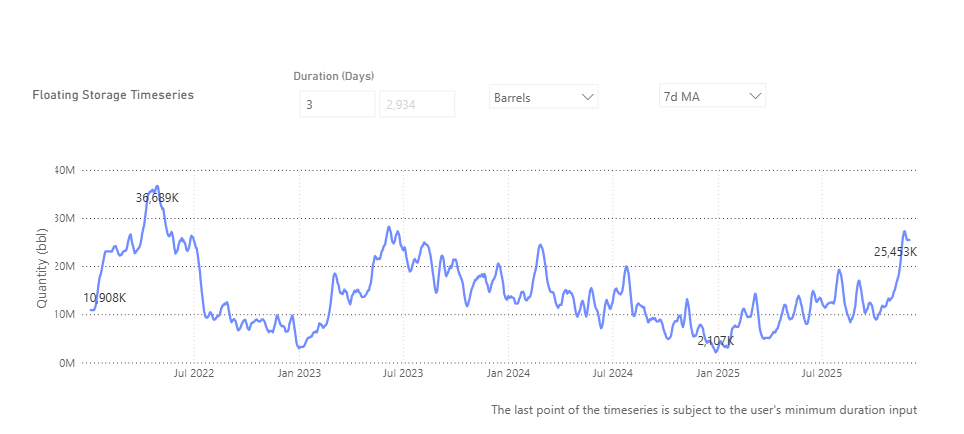

Floating storage is rising sharply across the tanker segments, VLCC, Suezmax, and Aframax, signalling a market increasingly shaped by oversupply concerns. The latest readings point to a decisive break higher through late 2025, with floating barrels approaching the 150 million bbl threshold peak recorded back in November 2022.

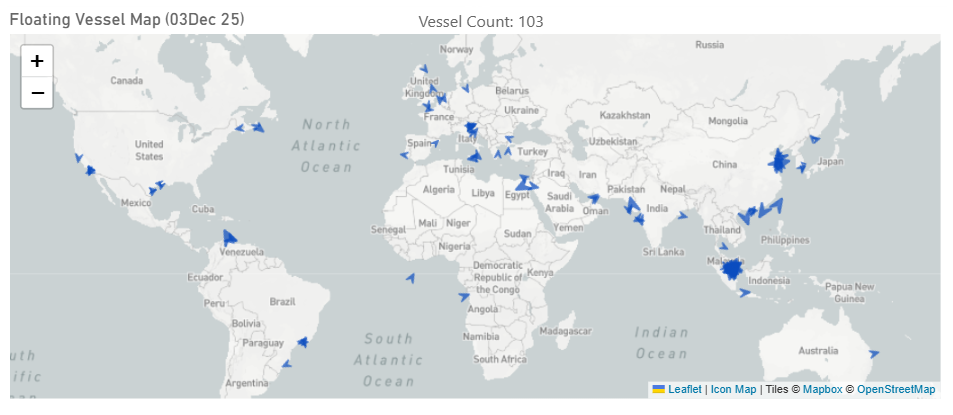

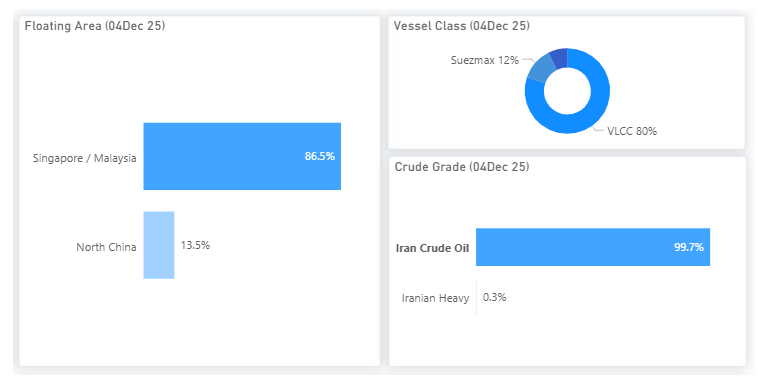

As of 3 December, VLCCs dominate floating storage with a 48% share, while Suezmax and Aframax fleets contribute 28% and 24%, highlighting the heavier concentration of crude held on larger tonnage.

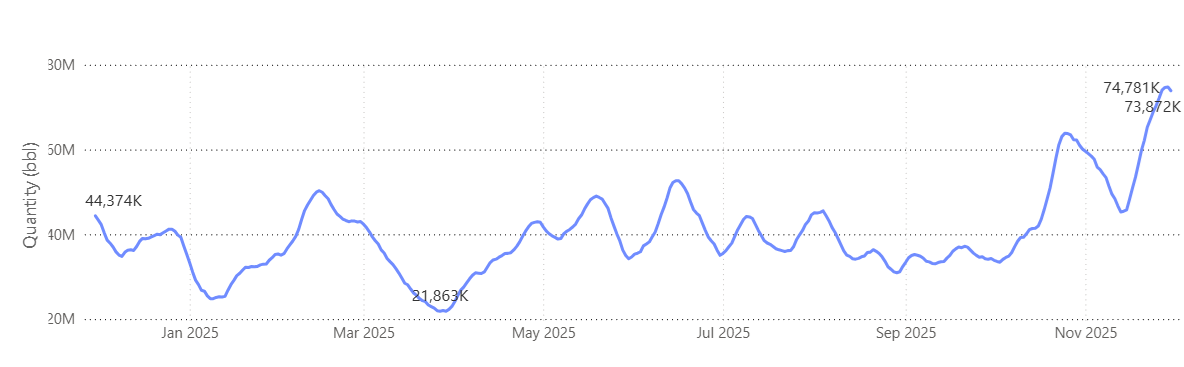

VLCC | 7D MA: > 70 Mbbl, compared with ~22 Mbbl in March (+230%)

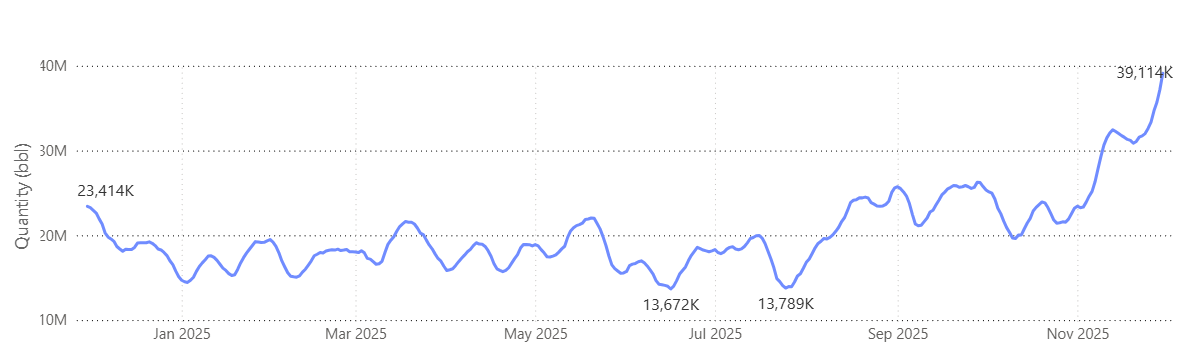

Suezmax | 7D MA:~40 Mbbl, compared with a mid-year low of ~13.7 Mbbl (+185%)

Aframax | 7D MA: ~29 Mbbl, up from an early-September low of ~9.1 Mbbl (+220%)

Iranian Barrels Dominate Floating Storage

Iranian crude represents the largest share of floating storage, with Malaysia acting as the main concentration point.

Compared with earlier months, the recent increase in floating crude volumes coincides with indications that China’s independent refiners had exhausted their import quotas and that teapot run rates had softened amid weak margins, both of which have historically influenced refiners’ willingness to take cargo from offshore. The time series shows a clear rise in floating barrels in early December, returning toward levels seen during previous spikes. However, the recent announcement of a new batch of crude import quotas for the remainder of the year will work in the direction of clearing those extra flows waiting on tankers.

At the same time, the distribution of stored volumes has shifted decisively toward offshore transfer hubs. As of 4 December, approximately 86% of floating barrels were concentrated in the Singapore/Malaysia area, which is commonly used for ship-to-ship transfers and the temporary holding of sanctioned or discounted crude, including Iranian grades. Vessel-level data further shows that the build-up is dominated by VLCCs (80%) carrying almost exclusively Iranian crude (≈99.7%), underscoring that the surge is not broad-based but tied to a specific supply stream facing slower onward absorption.

These refinery-side constraints, combined with refiners’ tactical choice to delay intake rather than accelerate discharge, help explain the longer waiting times, rising floating storage, and slower clearance into China that are now visible across the market.

Macro elements supportive of the high floating storage trends include oversupply and oil price projections

Macro conditions continue to align with the recent rise in floating storage. Several major outlooks point to a looser physical balance heading into 2026, with non-OPEC supply growth remaining a key feature. The latest forecasts still show incremental barrels led by U.S. shale, along with continued offshore growth from Brazil and Guyana.

Oil prices have softened in recent weeks as demand expectations are reassessed and broader risk sentiment cools. Forward spreads have also eased at times, creating periods where short-term storage economics become more viable, which can contribute to the build in offshore volumes when combined with already ample supply.

OPEC+ has signalled a cautious approach to supply management heading into early 2026, though analysts generally expect global balances to remain on the looser side. If oversupply persists and refinery maintenance intensifies into Q1, floating storage could remain elevated, tightening vessel availability and adding upward pressure to freight rates.

Use Signal Ocean’s Voyage Details to spot emerging signals and stay ahead of shifts in the oil world. For more insights, please contact our team. Stay ahead of the curve. Get access to the Signal Ocean Platform.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)