Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Iran- USA/Israel Conflict impact on fertiliser markets

While global markets are currently preoccupied with the potential impact of escalating Middle East tensions on oil, the crisis also poses a significant, though less discussed, risk to fertiliser supply chains. This disruption could ultimately affect global agriculture and food prices. Given the Arabian Gulf's crucial role in global fertilizer production and export, it is essential to consider the implications of the current crisis for the agricultural sector, apart from the primary focus on energy.

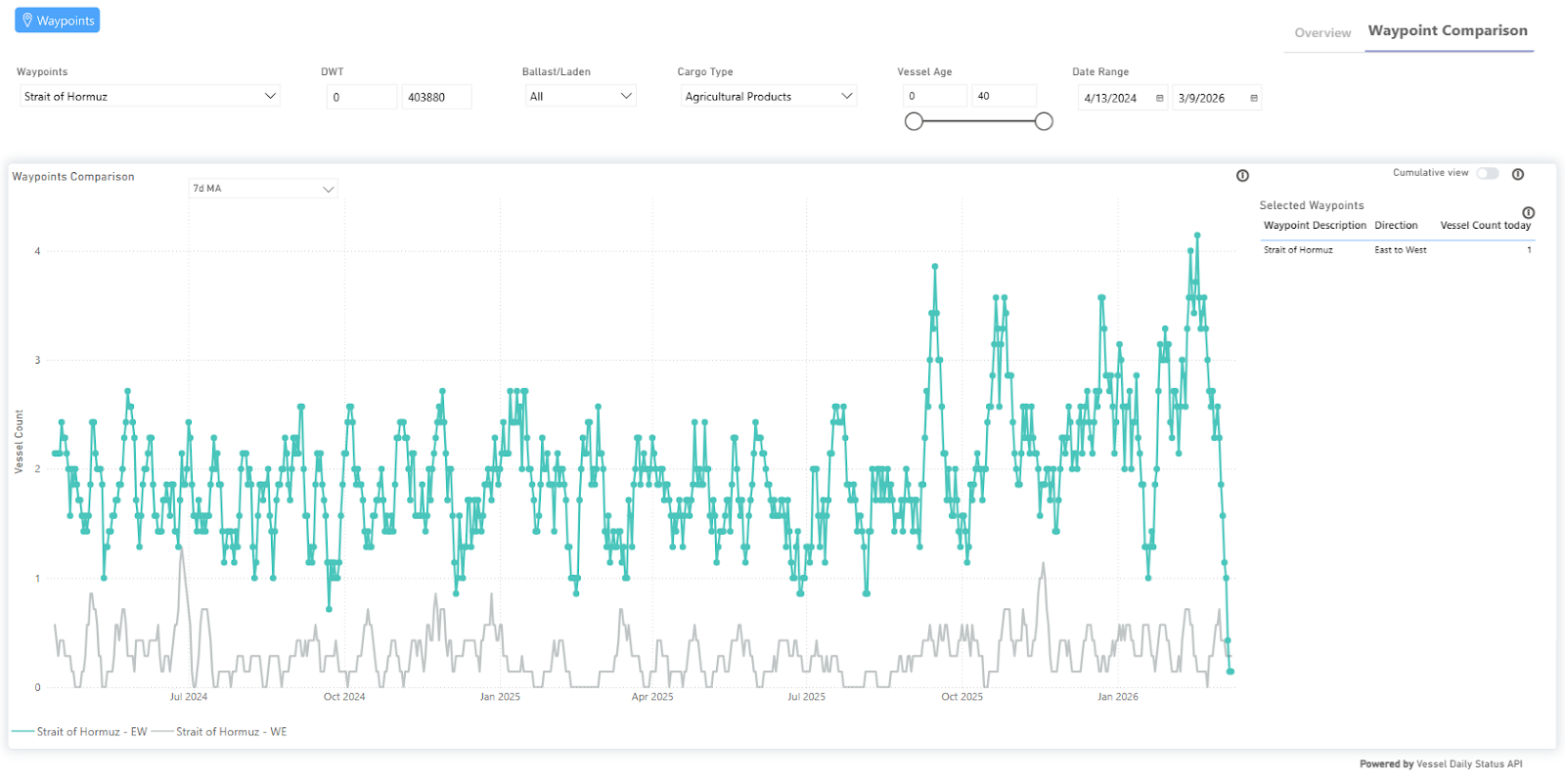

TSOP waypoints data (Strait of Hormuz EW), for the agriculture cargo type, is already capturing the near standstill of vessel count from the onset of the crisis. If sustained, disruptions to fertiliser exports could create challenges for agricultural producers, potentially influencing crop yields and contributing to upward pressure on food prices in the months ahead.

In our analysis below, we take a closer look at what if the conflict persists could mean for the fertiliser supply chain that also depends heavily on the Gulf.

Fertiliser Flows

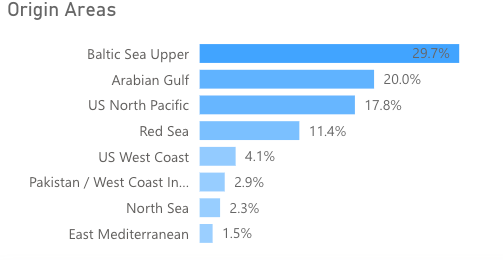

~20% of all fertiliser flows originate from the Arabian Gulf

~46% of global urea flows from the Arabian Gulf

Source: Vessel Count TSOP | Fertiliser flows from the Arabian Gulf

The Arabian Gulf is one of the most important regions for global fertiliser production and trade. Countries including Saudi Arabia, Qatar, Oman, and the United Arab Emirates host major facilities producing key inputs such as urea, sulphur, and ammonia. Iran is also a notable producer of ammonia, an essential component used in nitrogen-based fertilizers.

Given the region’s central role in fertiliser production and exports, developments affecting logistics and maritime transit in the Gulf are closely monitored by agricultural and commodity markets.

Signal Ocean recorded that 20% of all fertiliser flows originated from the Arabian Gulf in 2025. This proportionality increases to 46% when considering only urea, the most widely used nitrogen fertiliser globally.

As a result, with the Iran-US/Israel war effectively closing the Strait of Hormuz, the market could lose between 3-4mt of fertiliser a month, with the two most populated countries in the world, India and China, being the most exposed.

Exposure of Major Importers

India and China are most exposed to limited fertilizer flows from the Arabian Gulf, as the region accounts for 23% and 20% of all fertiliser imports, respectively.

Source: Fertiliser flows to India TSOP , fertiliser flows to China TSOP

Potential Agricultural Effects of Reduced Fertiliser Flows from the Arabian Gulf

A reduced flow of fertiliser from the Arabian Gulf will have substantial knock-on effects for agricultural yields in the coming year. In situations like this, there tends to be a chain of events that farmers use to mitigate the impact.

Lower fertiliser application

The first is that producers use less fertiliser. There is evidence that most producers use more fertiliser than needed as an insurance policy. However, less fertilizer does make crops less robust against challenging weather conditions such as drought or intense heat. This would likely lead to smaller crop yields, with the weather being the swing factor in terms of how much they fall.

Shifts in crop selection

The second is that farmers switch to crops that require less nitrogen, opting for legumes such as soybeans rather than corn. The obvious outcome of this is that there is a glut of a certain crop and a lack of another. Corn, for instance, is nitrogen-intensive to produce; if enough producers swapped out of producing this, animal feed prices would likely rise, impacting the cost of meat or farmed fish.

Reduced planting on marginal land

The third is that farmers reduce planting in marginal areas. This cuts initial costs and increases efficiency as less profitable land, which requires more fertiliser, is not used. The outcomes for farmers are a better return per acre planted. The issues arise from a compounding effect of multiple farmers following this, with a global decrease in yields. The effect of higher food prices comes later.

Takeaway

Overall, the disruption of fertiliser flows from the Arabian Gulf is likely to tighten global agricultural supply, particularly for nitrogen-intensive crops such as corn and wheat. While farmers may partially mitigate the impact through reduced fertilizer use, crop switching, and focusing on higher-yield areas, these measures cannot fully offset the loss of inputs. The result is likely to be smaller global harvests, higher feed and food prices, and increased volatility in agricultural commodity markets, with major importers like India and China feeling the effects most acutely. Markets will closely watch alternative exporters, such as the United States and Brazil, as they may step in to fill supply gaps, but the timing and scale of such responses will determine the severity of the impact.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)