drives these stories

Asia realigns as Iraq expands and the U.S. targets Russian oil imports from Indian buyers

In late July 2025, the United States announced a 25 percent tariff on Indian exports, explicitly citing India’s continued purchases of Russian crude oil and military equipment. The move was widely interpreted as part of a broader strategy targeting countries that maintain strong commercial ties with Moscow.

On August 6, a follow-up executive order imposed an additional 25 percent tariff on Indian goods, scheduled to take effect 21 days later. If implemented as planned, this would raise India’s total tariff exposure to 50 percent, one of the highest faced by any U.S. trading partner. Indian officials have condemned the measure as discriminatory, noting that other major importers of Russian oil have not been subjected to similar punitive actions by the United States. It is important to highlight that the latest actions reflect a broader U.S. effort, including proposed secondary sanctions and potential tariffs of up to 500%, targeted at countries importing Russian energy, notably China and India.

Iraq’s Position in Asian Crude Demand

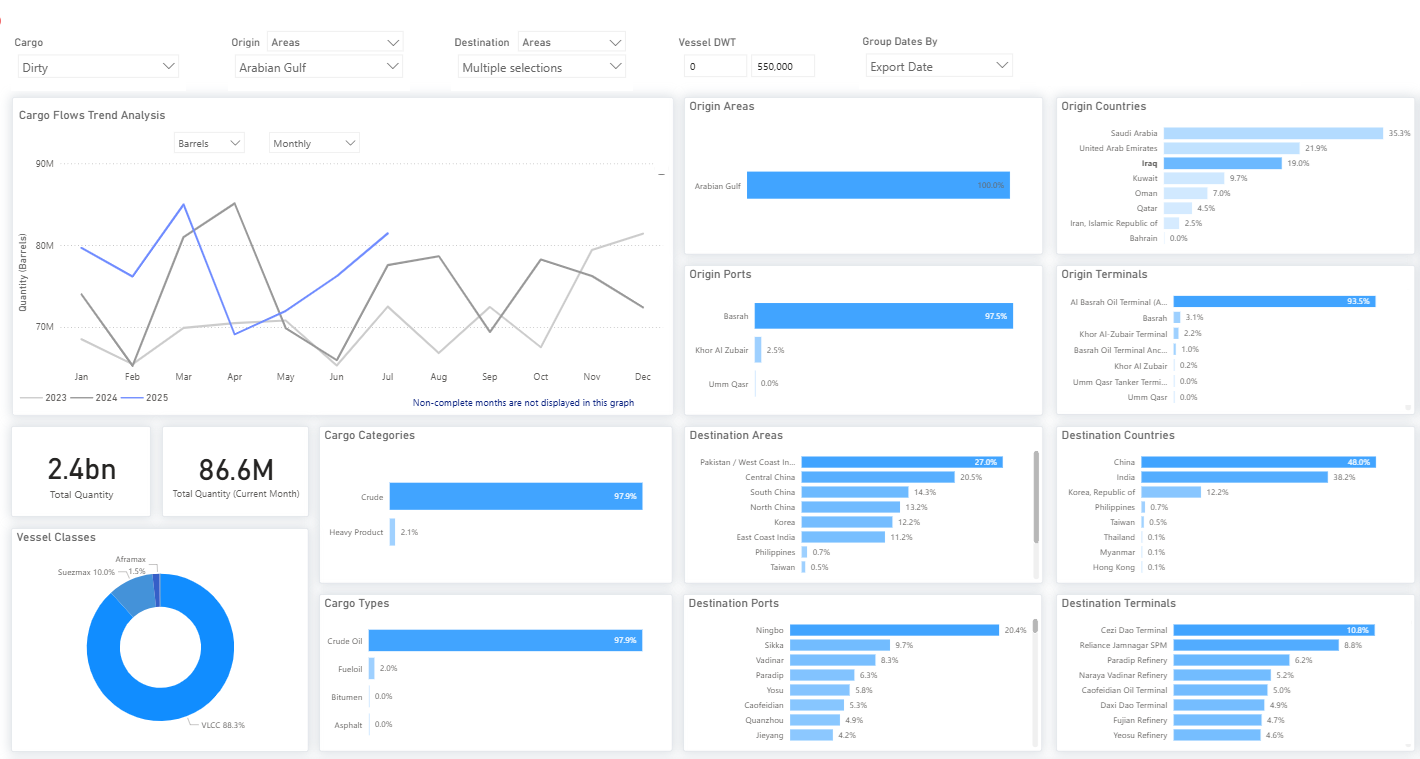

Within the Arabian Gulf, Iraq ranks as the third-largest crude supplier, holding a 19.0% share behind Saudi Arabia and the UAE. From Iraq’s perspective, China and India are its two most critical markets: China accounts for 48% of Iraqi dirty crude exports, while India follows with 38.4%, according to July 2025 tanker tracking data. The prominence of Indian demand reflects Iraq’s position as a stable supplier of medium sour grades, well-suited to Indian refinery configurations. Indian crude oil purchasing is primarily influenced by pricing and quality; however, Iraq stands to gain if there are changes in market sentiment or stricter policies regarding Russian oil exports.

****

Iraq’s southern export infrastructure is highly centralised: 97.5% of its crude volumes depart via Basrah Port, and 94% originate from the Al Basrah Oil Terminal. Crude accounts for 97.9% of Iraq’s total dirty cargo exports, and Very Large Crude Carriers (VLCCs) handle 88.3% of all shipments. China’s Cezi Dao Terminal (10.8%) is currently the leading destination for Basrah-origin crude, followed closely by key Indian refineries at Reliance Jamnagar SPM (8.8%), Paradip (6.2%), and Vadinar (5.2%).

Iraq accelerates upstream expansion: July adds to medium-term export surge

Iraq has intensified its upstream development push in 2025, targeting a medium-term production capacity of 6 million barrels per day by 2028 to 2029. This effort is underpinned by accelerated well activity and field modernization, alongside new licensing deals with international and Chinese partners. According to official figures from the Iraqi Drilling Company, 113 oil wells were completed in the first half of 2025, including 27 newly drilled wells and 86 rehabilitated ones, across both southern and northern regions.

Field-level development remains concentrated in Iraq’s southern supergiant assets, with active expansion programs at West Qurna 1, Zubair, Rumaila, Majnoon, Faihaa, and Ratawi. Notably, West Qurna 1, operated by PetroChina, is projected to reach 750,000 barrels per day by year-end 2025, while Halliburton is leading a redevelopment of Nahr Bin Omar, targeting a ramp-up from 50,000 to 300,000 barrels per day. In parallel, Iraq has finalized a redevelopment plan for the Kirkuk oil cluster in collaboration with BP, aiming to recover northern field capacity.

These initiatives are designed to support long-term production growth, but actual output increases remain subject to project execution timelines, infrastructure bottlenecks, and associated gas capture and water injection capabilities. Iraq’s infrastructure modernization includes pumping system upgrades, energy supply enhancements, and capacity improvements at key terminals.

In the short term, however, Iraq’s crude export volumes are constrained by OPEC Plus quota discipline. Despite higher technical capacity, Iraq’s May and June 2025 exports averaged approximately 3.2 million barrels per day, down from earlier levels of 3.4 million barrels per day.

The latest OPEC Plus decision, made in July 2025, confirms a gradual unwind of voluntary cuts starting in October 2025, including Iraq’s share of the rollback. Iraq’s official production target will rise incrementally in the fourth quarter of 2025, offering room for modest export increases if project ramp-ups stay on schedule. However, the government has reaffirmed its commitment to avoid quota breaches as it navigates capacity expansion and market balance.

In early 2025, Iraq completed key infrastructure upgrades at the Al Basrah Oil Terminal (ABOT), its primary export hub, by installing new high-capacity pumping units and metering systems. These enhancements significantly improved operational efficiency, loading speeds, and flow control for VLCC shipments. As a result, ABOT’s effective export capacity now exceeds 3.3 million barrels per day, creating technical headroom for future output growth. Additional investments in terminal systems and pipeline integration are ongoing, positioning Iraq’s southern export infrastructure to support expanded volumes as OPEC Plus restrictions ease. Nonetheless, actual export flows remain aligned with quota compliance.

July flow data confirms a gradual export rebound

Iraq’s crude oil exports from the Arabian Gulf have shown a fluctuating trend over the past year. After a solid start in the early months, volumes eased through March and April before experiencing a sharper dip in May. June marked the lowest point so far, but flows began to rebound in July. This recovery suggests a potential shift in market dynamics, possibly supported by stronger demand from Asian buyers, particularly as refineries in China and India typically ramp up crude intake in the third quarter due to seasonal restarts and pre-winter stockpiling.

The rebound also coincided with a period of heightened regional volatility. In mid-July 2025, a series of drone attacks struck oilfields in Iraq’s semi-autonomous Kurdistan region, disrupting operations and raising geopolitical tensions across northern Iraq and neighboring areas. While the immediate supply impact was geographically contained, the unrest reinforced market sensitivity to northern instability and, by contrast, may have strengthened the strategic appeal of Iraq’s southern export infrastructure via the Arabian Gulf.

In July 2025, Iran lowered its official selling prices (OSPs) for key crude grades marketed to Asian refiners, marking a shift from the previous month’s levels. Iran Light crude was priced at $1.50 per barrel above the Oman/Dubai benchmark, down from $1.80 in June, indicating a clear reduction in premium. The Forozan blend also experienced a marginal price adjustment, slipping from a $0.10 premium in June to $0.05 above the benchmark in July. Iran Heavy crude saw its discount deepen slightly, moving from $0.15 below the Oman/Dubai average in June to $0.20 below in July.

These month-on-month adjustments in July reflect a relative softening in Iranian pricing across all grades. While the direct impact on market share is not publicly documented, such pricing behavior may reinforce Iran’s competitiveness among price-sensitive Asian refiners, especially at a time of heightened geopolitical uncertainty in neighboring crude-producing regions.

Looking ahead

Frequently Asked Questions

Why are U.S. tariffs affecting India's crude oil imports from Russia? The U.S. has imposed tariffs on Indian exports — reaching a potential 50% — explicitly citing India's continued purchases of Russian crude. The policy is part of a broader effort to pressure countries maintaining energy ties with Moscow, including proposed secondary sanctions targeting Russian oil buyers.

How much of Iraq's crude exports go to Asia? China and India together absorb over 86% of Iraqi dirty crude exports. China accounts for 48% and India for 38.4%, based on July 2025 tanker tracking data. Both markets are central to Iraq's export strategy.

What is Iraq's crude export capacity and how is it structured? Iraq's southern export infrastructure handles 97.5% of total crude volumes through Basrah Port, with 94% departing from the Al Basrah Oil Terminal (ABOT). VLCC vessels carry 88.3% of all shipments. ABOT's upgraded capacity now exceeds 3.3 million barrels per day.

When will Iraq increase production under the OPEC Plus framework? The July 2025 OPEC Plus decision confirmed a gradual rollback of voluntary cuts beginning October 2025. Iraq's official production target will rise incrementally in Q4 2025, with further increases tied to project execution timelines across its southern supergiant fields.

Which Iraqi oilfields are expanding production in 2025? Active expansion programs are underway at West Qurna 1, Zubair, Rumaila, Majnoon, Faihaa, and Ratawi. West Qurna 1, operated by PetroChina, is targeting 750,000 bpd by year-end 2025. Nahr Bin Omar is being redeveloped by Halliburton, with a target ramp-up from 50,000 to 300,000 bpd.

How is Signal Ocean tracking these crude flow shifts? Signal Ocean's tanker tracking platform provides real-time visibility into dirty cargo flows, vessel routing, port-level loadings, and cargo origin data — giving traders and analysts the data layer needed to monitor Iraq, Russia, and Asian crude dynamics as they evolve.

With Russian crude flows under pressure, Iraq is leveraging its robust export infrastructure and refinery-compatible medium-sour grades to win market share in Asia. Chinese independent firms, such as Geo‑Jade, United Energy Group, Zhongman, and Anton, are making deep inroads in Iraq’s upstream sector, aiming to double their output to 500,000 bpd by 2030. These upstream efforts are being complemented by integrated investments like Geo‑Jade’s South Basra project, which includes a new refinery and petrochemical complex. While Chinese refiners are solidifying their long-term crude supply footprint in Iraq, Indian refiners are navigating short-term disruptions. U.S. sanctions and tariff threats have forced Indian state refiners to pause spot purchases of Russian crude, prompting them to turn to alternative suppliers. Indian Oil Corporation (IOC) recently ordered a mix of substitutes: one VLCC of WTI crude from Mercuria, three Suezmaxes of WTI from Phillips 66, Equinor, and Vitol, one VLCC of Das blend from Trafigura, and one Suezmax of Western Canadian Select (WCS) from Vitol. Despite this diversified response, Iraqi grades remain a favored long-term replacement, given their compatibility with Indian refining systems and existing logistics.

Track Iraq crude flows with Signal Ocean

Signal Ocean's platform delivers real-time tanker tracking, cargo flow analytics, and market intelligence across the Arabian Gulf and beyond. Request a demo from Signal Ocean to see how the platform supports crude flow monitoring, voyage analysis, and supply chain visibility. Visit the Signal Ocean Newsroom for the latest market updates, or read the previous Special Focus on Supramax and Panamax coal cargo flow trends from Indonesia.

Ready to get started and outrun your competition?

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)