Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

COMMODITY RADAR | Spotlight: IRON ORE

Disconnect between Chinese iron ore imports and steel production widens

Chinese iron ore imports continue to grow even as domestic steel output weakens, driving port inventories toward record highs. Until Simandou's accelerating ramp-up is offset by cuts elsewhere in the supply chain, the inventory overhang is set to deepen, complicating the demand outlook for traditional exporters

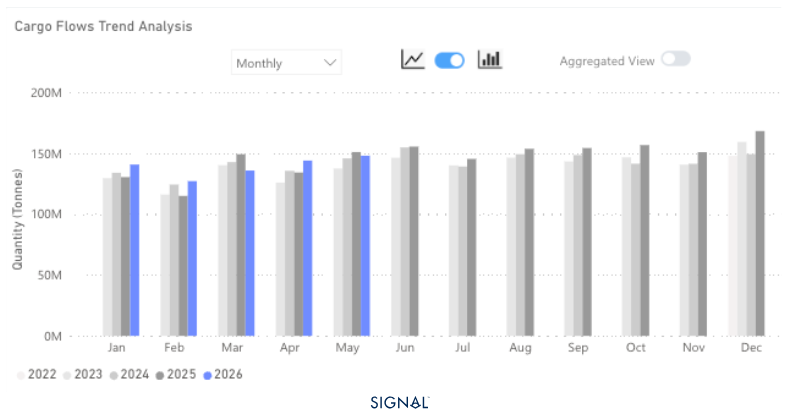

Global iron ore flows in May 2026 were down 2% y/y.

Flows to China increased by 3% y/y.

Flows destined to ports outside of China fell by 15% y/y.

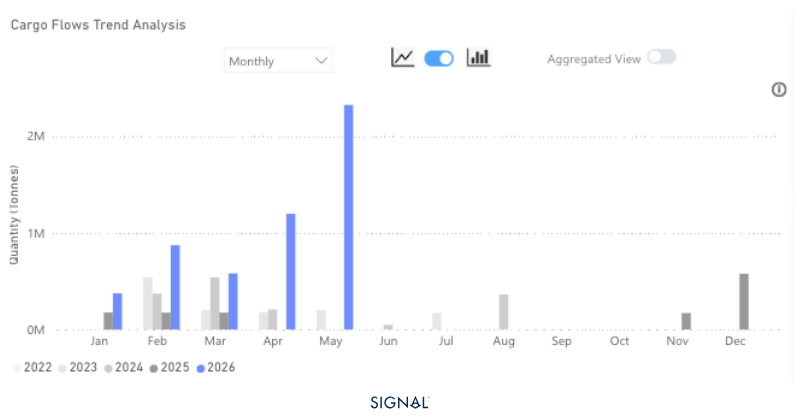

Iron ore flows from Guinea reached 2.1mt in May as Simandou continued to ramp up

Global iron ore flows reached 145mt in May 2026, down 2% on the same month last year. Flows to China continued to increase, by 3% this month, but growth was the lowest it has been since March, as the steel industry in China faces mounting headwinds.

Outside of China, demand for iron ore remains subdued as steel production is still under pressure. As a result, iron ore flows destined for ports outside of China fell by 15% y/y in May 2026.

Iron ore flows from Guinea reached over 2 million tons in May, a record and almost double the previous record from the previous month. Despite this, Guinea still only accounted for 2% of all global iron ore flows in May 2026. Australia and Brazil continued to dominate, exporting 86mt and 33mt respectively.

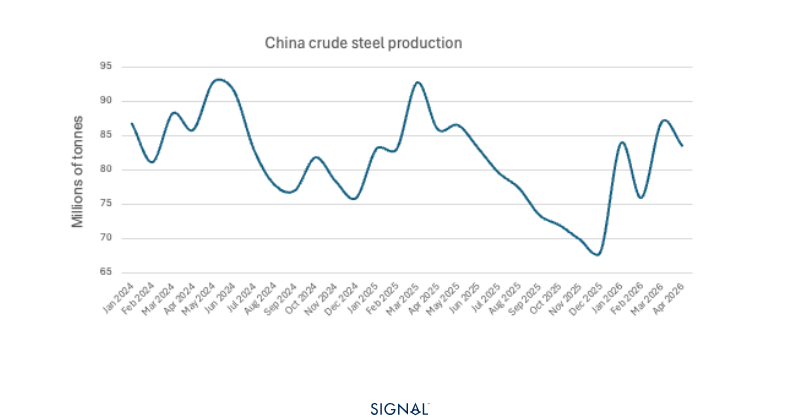

The NBS reports Chinese crude steel production tracking 4% below prior-year levels year-to-date, yet iron ore imports have moved in the opposite direction, up 3% over the same period. The result is a port inventory build that has taken Chinese stockpiles to 160mt as of the week ending May 22nd, within touching distance of the 165mt record set in March 2026 and some 22% above the July 2025 trough. The disconnect between import strength and steel output is the defining feature of this market, and it is now correcting: import growth is decelerating as portside rebalancing mechanics take hold.

The near-term demand trajectory for Australian exporters is unfavourable on two counts. Aggregate Chinese import demand is expected to ease from current levels as the inventory overhang is absorbed, reducing overall seaborne volumes. Simultaneously, the structural shift toward higher-grade feedstock, accelerated by Simandou's commercial ramp-up, reduces the relative attractiveness of Australian mid-grade fines at a time when Chinese mills are under margin pressure and incentivised to optimise blend economics.

For the capesize market, however, the Simandou narrative is a meaningful offset. Guinea-to-China adds approximately 25% in tonne-miles relative to an equivalent Australian voyage; at Simandou's projected plateau of 10mt per month, the incremental tonne-mile generation is substantial. Critically, this freight uplift occurs regardless of whether overall Chinese import volumes grow; it is a trade-route effect, not a volume effect. Even a gradual displacement of Australian tonnes, well ahead of full ramp, should provide durable underlying support for capesize rates through the balance of the year.

Source: China crude steel production from NBS https://data.stats.gov.cn/dg/website/page.html#/pc/national/en/monthData

Guinea to China to boost cape rates even if total volumes fall

The central market tension is a growing disconnect between Chinese import volumes and domestic steel output, which continues to decline. Port inventories remain near record highs, and import growth is now decelerating as the overhang corrects.

For the capesize market, Simandou's accelerating ramp-up provides a meaningful structural offset to softening overall volumes. Guinea-to-China generates materially more tonne-miles than an equivalent Australian voyage, making the freight uplift a trade-route effect rather than a volume one, and one that compounds as displacement of Australian tonnes gradually builds.

Luke has over 8-years of experience analysing and forecasting commodity markets, with particular expertise in stainless steel raw materials and the wider metals markets.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)