Subscribe for our latest news, straight to your inbox:

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Share this post

Spotlight of the Week| Chinese Crude Oil Flows

China Crude Oil Imports Fall 23% in First Half of 2026

May marks the low point of the period as vessel-tracking data shows a sharp Q2 decline, followed by signs of stabilization in July

Chinese seaborne crude oil imports fell approximately 23% year-on-year in the first half of 2026, according to Signal Ocean vessel-tracking data, declining from roughly 1.87 billion barrels in H1 2025 to an estimated 1.44 billion barrels in H1 2026.

Imports opened the year above 2025 levels in January and February before turning sharply lower from March onward. May 2026 marked the low point of the period, with tracked imports down approximately 47% year-on-year, the steepest single-month decline observed in the dataset this year. June volumes remained at similarly depressed levels.

Preliminary tracking for July 2026, combined with a modeled month-end estimate, indicates imports of approximately 177 million barrels, a modest increase of around 2% versus June, but still roughly 41% below the same month in 2025. The data suggests the sharp sequential declines seen from March through June have begun to stabilize, though volumes remain well below prior-year levels.

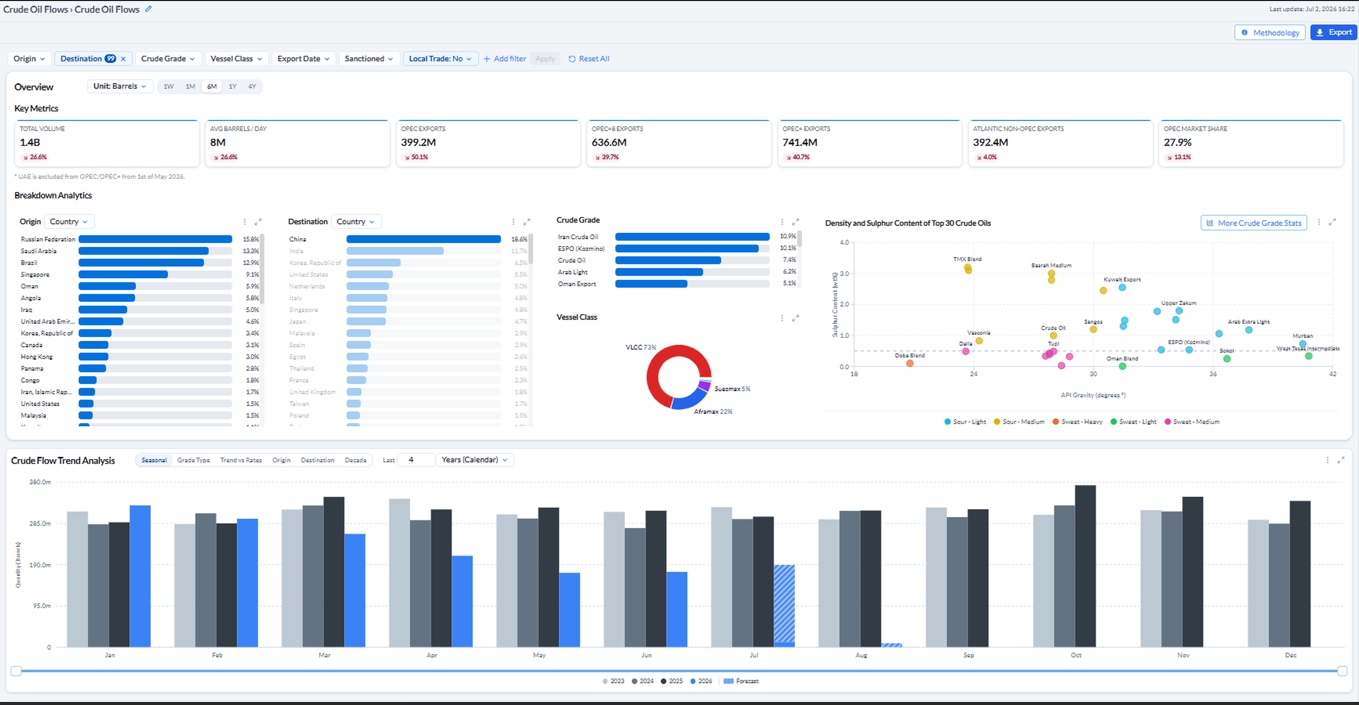

Signal Ocean Crude Oil Flows - China, 6-Month View

China crude imports, trailing 6-month view. Platform-reported tracked volume of 1.4B barrels, down 26.6% YoY on a rolling 6-month basis.

Key year-on-year moves: Jan +13.5% · May -46.8% · July -41.0% (est.)

Monthly Import Volumes - China (Year-on-Year)

Volumes in barrels. H1 Total covers January–June. July 2026 reflects partial-month tracking plus a modeled projection and is excluded from the H1 total. This update reflects observed and estimated import volumes only and does not constitute a forecast of future market conditions or an indicator of underlying demand drivers. Source: Signal Ocean.

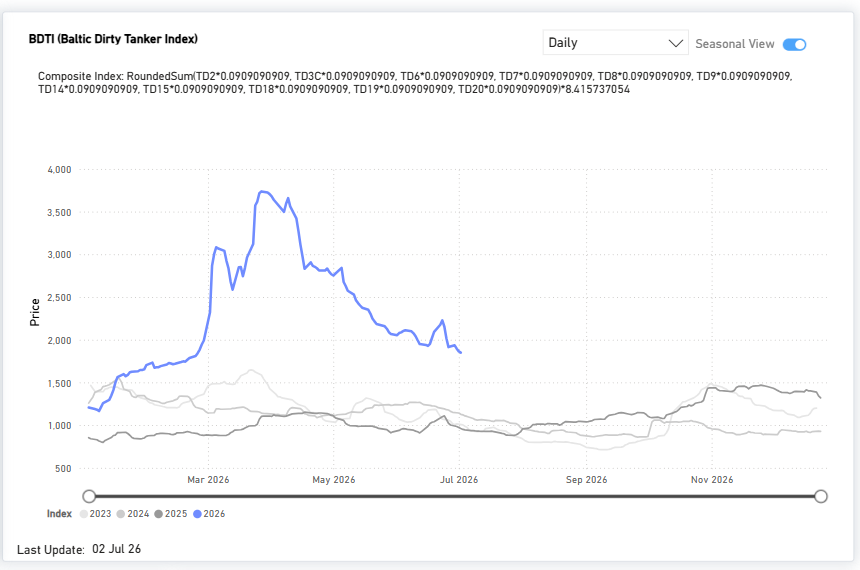

Freight Market Overview - Dirty

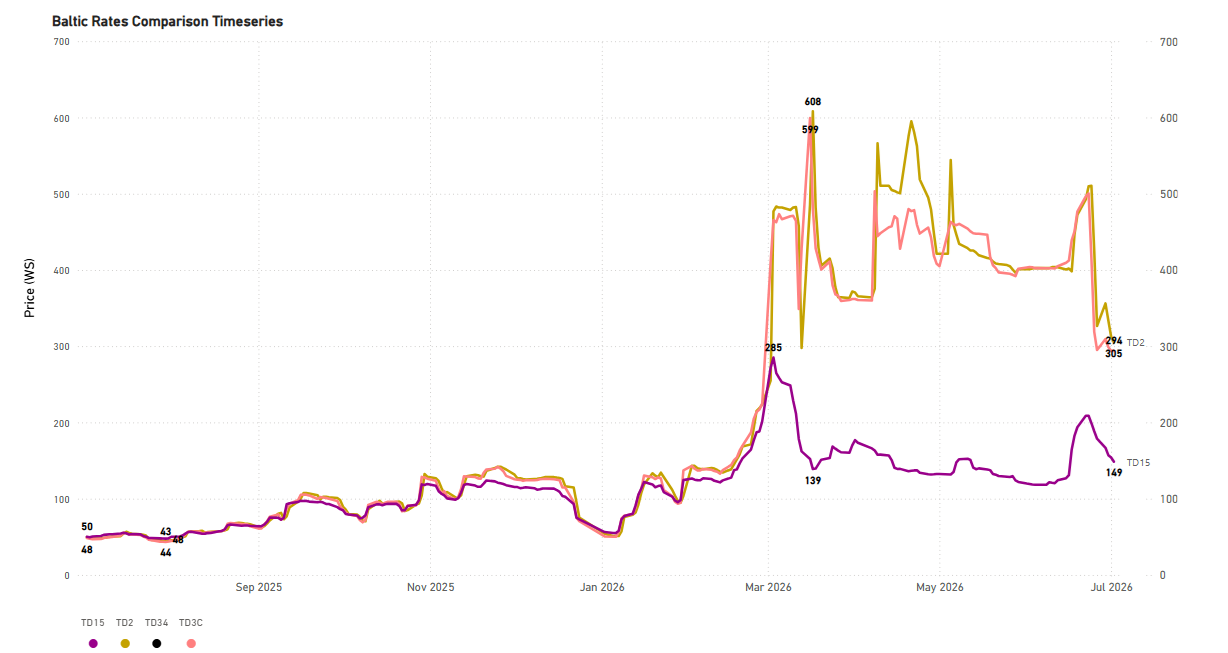

As of early July 2026, the Baltic Dirty Tanker Index had eased sharply to 1,850 points, down 49.2% year-to-date and roughly 50% from its peak, as tanker traffic through Hormuz began to normalize, though it remained approximately 92.5% above year-ago levels. Middle East Gulf-to-China rates (TD3C) had similarly retreated to 293.89 Worldscale points, down 27% monthly.

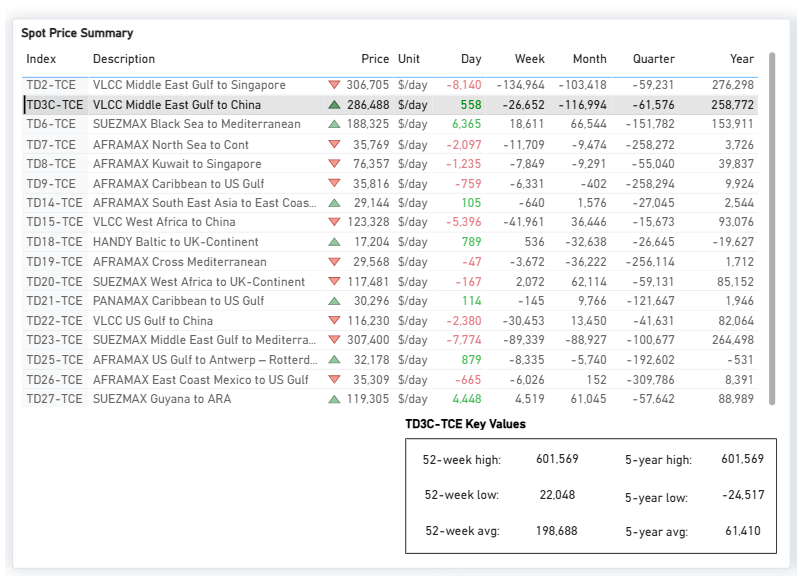

Time-Charter-Equivalent Earnings: The AG–China Route Correction

The correction was especially pronounced on time-charter-equivalent (TCE) earnings for the Middle East Gulf-to-China VLCC route (TD3C-TCE), the benchmark most directly tied to Chinese crude buying. As of July 2, 2026, daily earnings on the route stood at approximately $286,500 per day, still elevated at roughly 44% above the 52-week average, but down about $117,000 (‑29%) over the past month and more than 52% below the 52-week high of $601,569 recorded at the height of the crisis. On a year-on-year basis, earnings remained sharply higher (+$258,772), reflecting how depressed the pre-conflict starting point had been.

The retreat in freight earnings tracks the broader trajectory of US–Iran negotiations over the Strait of Hormuz. Following more than three months of conflict that severely disrupted a waterway through which around 20% of global oil trade normally passes, the United States and Iran reached an interim agreement in mid-June 2026 aimed at ending the conflict and reopening the strait, formalized through the Islamabad Memorandum signed on June 17, 2026. As transit conditions gradually improved, freight risk premiums eased, pulling TCE earnings back from their wartime extremes.

The latest round of indirect US–Iran talks in Doha on July 1 underscored that normalization remains incomplete. Mediators reported positive progress on issues linked to the memorandum, and both sides agreed to continue discussions. However, the technical negotiations concluded without resolving the main outstanding issues, with transit arrangements through the Strait of Hormuz remaining the principal point of disagreement. Shipping traffic has recovered only partially and remains well below pre-war levels, helping explain why TD3C earnings, despite retreating sharply from wartime highs, continue to trade well above pre-conflict norms.

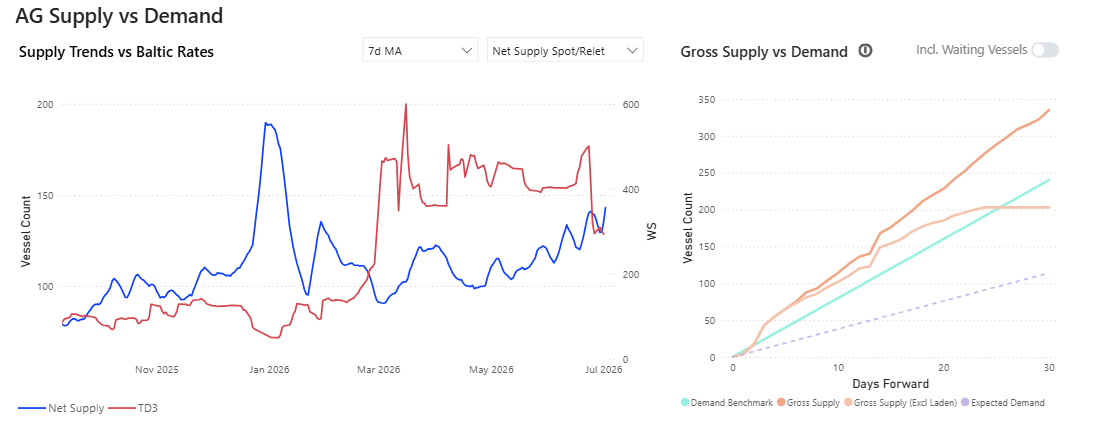

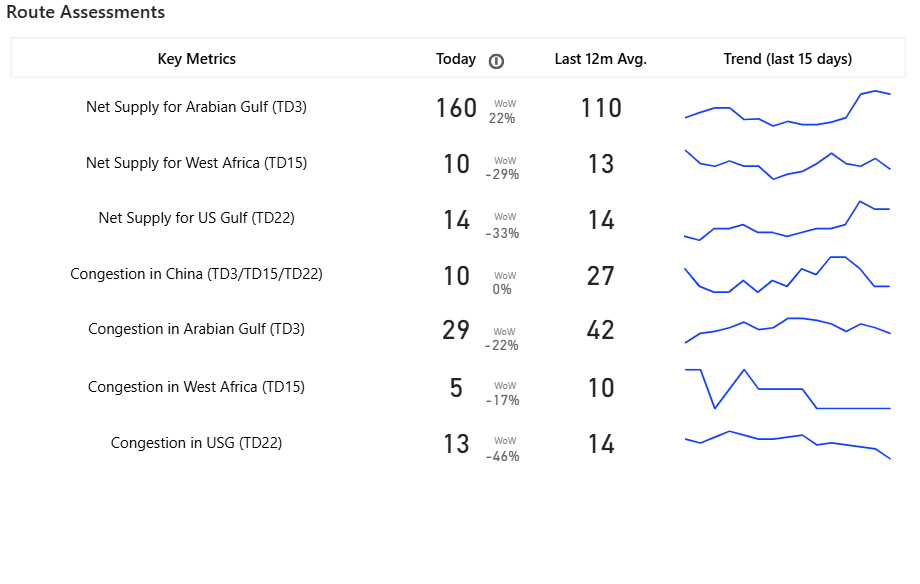

The latest indicators point to an upward trend in the net supply for the Arabian Gulf during the last 15 days, with the latest estimate at 160, up 22% W-o-W.

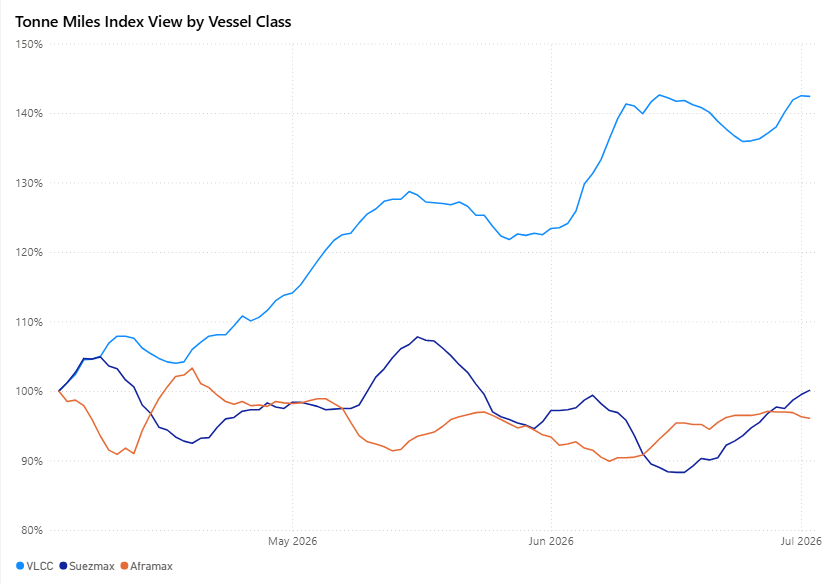

VLCC tonne-mile demand extended its outperformance, rising 6.1 ppts WoW to 142.4% and remaining above historical norms. Suezmaxes recorded a further improvement of 4.6 ppts WoW to 100.1%, returning above the 100% parity threshold. By contrast, Aframax tonne-mile demand softened only marginally, declining 0.6 ppts WoW to 96.1%, indicating almost stable underlying demand.

Metrics Description: Index View (Base 100) by total Tonne Miles over the selected period. This facilitates relative performance comparisons between segments of different sizes (e.g., comparing the growth rate of VLCC vs Suezmax)

Maria holds a M.Sc. in Shipping, Trade and Finance from the Bayes Business School at the City University in London and a B.Sc. in Shipping Economics from the University of Piraeus.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

No items found.

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

Creating a sustainable world requires us to embark on a journey towards a zero emission future, where every step is a commitment to preserve our planet for future generations.

Albert Greenway

Environmental Scientist, Sustainability Expert

Increased Use of Renewable Energy:

Shipping companies are embracing renewable energy sources to power onboard systems and reduce emissions during port operations. Solar panels and wind turbines are being installed on vessels to generate clean energy, reducing reliance on auxiliary engines, and cutting down emissions. Shore power facilities in ports allow ships to connect to the electrical grid, eliminating the need for onboard generators while docked.

Collaboration and Industry Partnerships:

Recognizing that addressing emissions requires collective action, shipping companies, governments, and organizations have formed partnerships and collaborations. These initiatives focus on research and development, sharing best practices, and promoting knowledge transfer. Joint projects aim to develop and deploy innovative technologies, improve infrastructure, and create a supportive regulatory framework to accelerate the industry's transition towards a greener future. The Zero Emission Shipping - Mission Innovation.

To pave the way for a greener future in shipping, the availability of alternative fuels plays a vital role in their widespread adoption. However, this availability is influenced by factors such as port infrastructure, local regulations, and government policies. As the demand for cleaner fuels in shipping rises and environmental regulations become more stringent, efforts are underway to improve the accessibility of these fuels through infrastructure development, collaborations, and investments in production facilities.

Liquefied Natural Gas (LNG) infrastructure has seen significant growth in recent years, resulting in more LNG bunkering facilities and LNG-powered vessels. Nonetheless, the availability of LNG as a marine fuel can still vary depending on the region. To ensure consistent availability worldwide, there is a need for further development of LNG supply chains and infrastructure. For biofuels, their availability hinges on production capacity and the availability of feedstock. Although biofuels are being produced and utilized in various sectors, their availability as a marine fuel remains limited. Scaling up biofuel production and establishing robust supply chains are imperative to ensure wider availability within the shipping industry.Hydrogen, as a fuel for maritime applications, is still in the early stages of infrastructure development. While some hydrogen vessels have been tested or introduced in the first quarter of last year, the infrastructure required for hydrogen production and distribution needs further advancement.

Ammonia, as a marine fuel, currently faces limitations in availability. The production, storage, and handling infrastructure for ammonia need further development to support its widespread use in the shipping industry.Methanol, on the other hand, is already a commercially available fuel and has been used as a blend with conventional fuels in some ships. However, its availability as a standalone marine fuel can still be limited in certain regions. Bureau Veritas in October 2022 published a White Paper for the Alternative Fuels Outlook. This white paper provides a comprehensive overview of alternative fuels for the shipping industry, taking into account key factors such as technological maturity, availability, safety, emissions, and regulations.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)